- The paper presents a CGAN framework with LSTM-based generators for synthesizing minute-level crypto time series.

- It validates synthetic data using statistical measures like Pearson, Spearman correlations, MAE, and RMSE across volatility regimes.

- The approach supports anomaly detection, algorithmic trading, and privacy-preserving data sharing in cryptocurrency markets.

Synthetic Data Generation in Cryptocurrency Markets Using CGANs

Introduction

The paper "Synthetic data in cryptocurrencies using generative models" (2604.16182) presents a comprehensive framework for generating minute-level synthetic cryptocurrency time series using Conditional Generative Adversarial Networks (CGAN) with LSTM-based generators. The main motivation is to address privacy limitations and data scarcity inherent in financial datasets by enabling the generation of statistically consistent, privacy-preserving, and high-fidelity synthetic series for major cryptocurrencies—Bitcoin (BTC), Ethereum (ETH), and XRP. The methodology leverages the temporal expressivity of LSTM for sequential price dynamics, validated by both statistical metrics and visual correspondence, and is specifically tailored for market scenarios characterized by exogenous shocks and structural regime shifts.

Methodological Framework

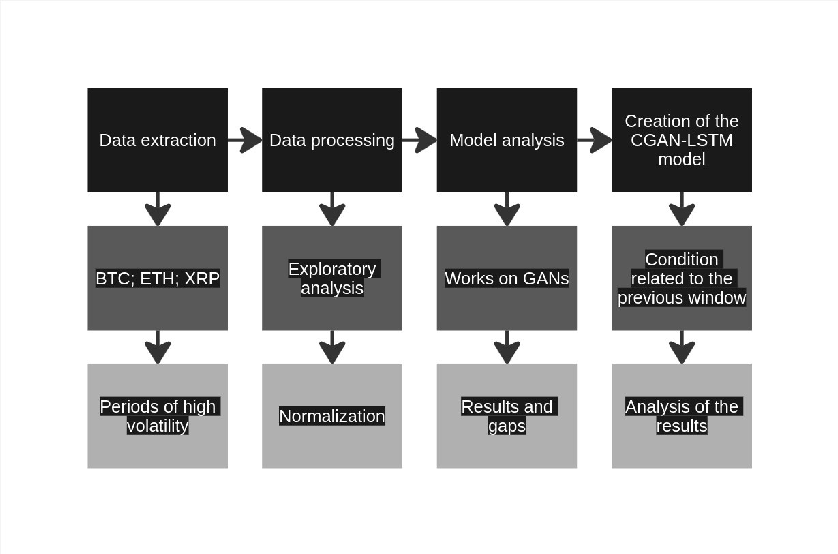

The methodology integrates deep generative models and time-series preprocessing tailored for high-frequency cryptocurrency data. The experimental design is illustrated in (Figure 1).

Figure 1: The end-to-end process, from raw data extraction to synthetic series validation via CGAN architecture.

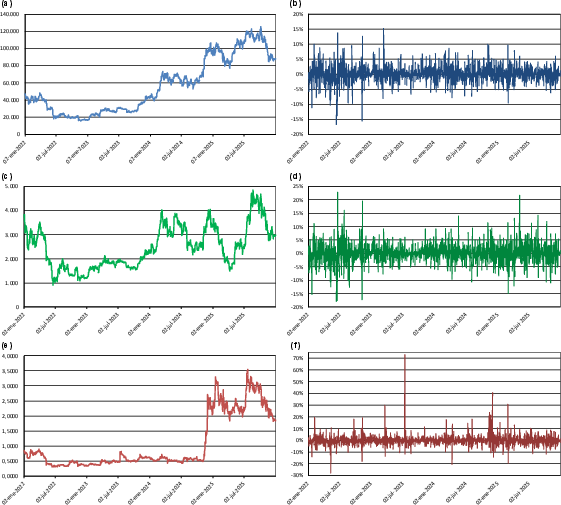

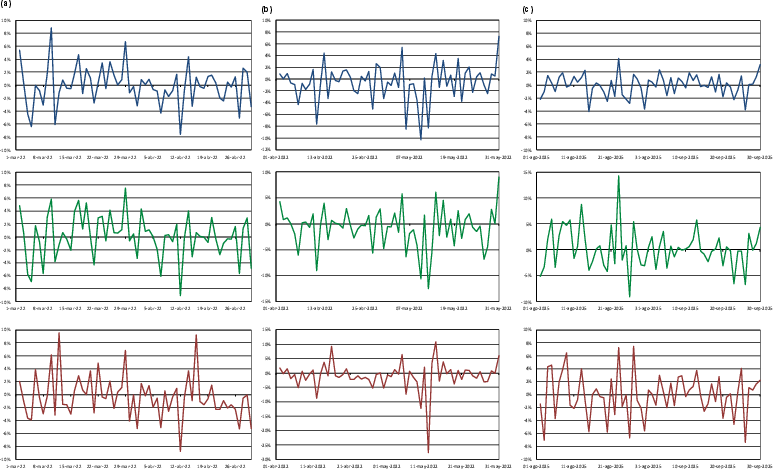

The cryptocurrency dataset spans January 2022–October 2025, with focused analysis on three volatility regimes: the March–April 2022 period (post-Russia-Ukraine conflict onset), April–May 2022 (macro-financial stress), and September 2025 (geopolitical and policy disruption), as visualized in (Figure 2) and (Figure 3).

Figure 2: Macro-level price evolution for BTC, ETH, and XRP highlighting major volatility epochs.

Figure 3: Intra-period volatility segmentation reflecting the distinct risk/return landscapes of different macro regimes.

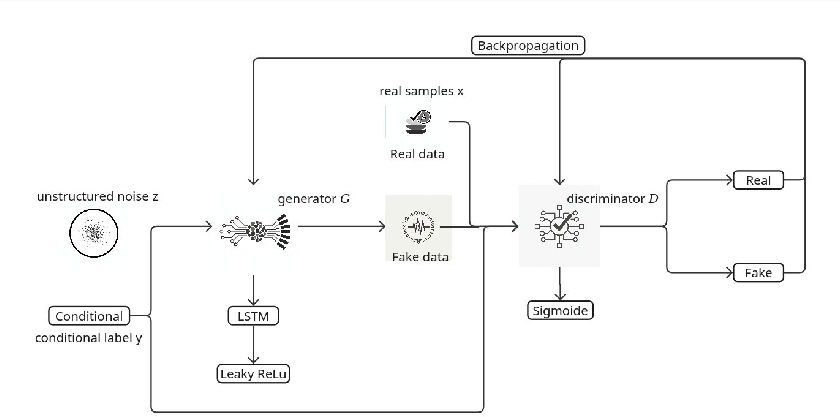

Central to the approach is a CGAN architecture (Figure 4):

- The generator employs an LSTM Cell, receiving the closing price at t−1 as a condition and producing a candidate value for t.

- The discriminator is a multilayer perceptron classifying pairs (Pricet−1,Pricet) as either real or synthetic.

This architecture enables the generator to learn complex temporal dependencies while the discriminator enforces statistical fidelity in local price trajectories.

Figure 4: Detailed schematic of the hybrid LSTM-MLP CGAN architecture for conditional time series synthesis.

Normalization is performed via StandardScaler, ensuring each asset’s data is centered and scaled, thereby providing a robust regime for gradient-based adversarial optimization. Generation and discrimination employ BCEWithLogitsLoss for numerical stability, with Adam optimizer (η=2⋅10−4, β1=0.5, β2=0.999) and a look-back window of 60.

Experimental Results

Quantitative Metrics

Synthesis quality is assessed through Pearson and Spearman correlations between real and generated test sets, and by MAE and RMSE computed for each asset-period pair. For example, BTC and ETH series routinely exhibit Pearson and Spearman correlations at or above 0.999 across all three periods.

Strong alignment is further observed in direct sample-wise comparison. For the most volatile period (April–May 2022), BTC synthetic data achieves MAE of 46.71 and RMSE of 58.49, and ETH shows much lower error (MAE: 2.50, RMSE: 3.54), with extremely high Pearson/Spearman coefficients. XRP error is similarly low (MAE: 0.00065, RMSE: 0.00095).

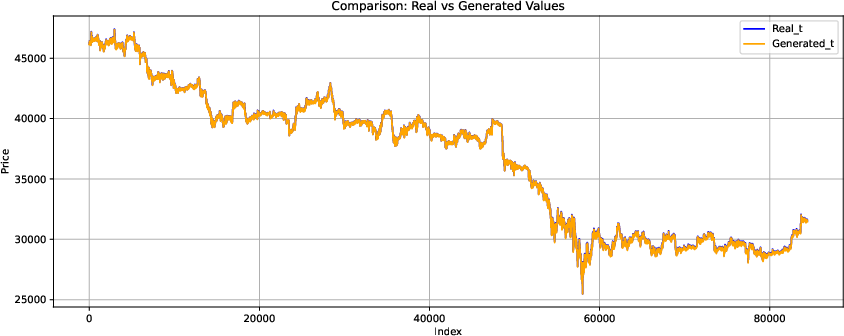

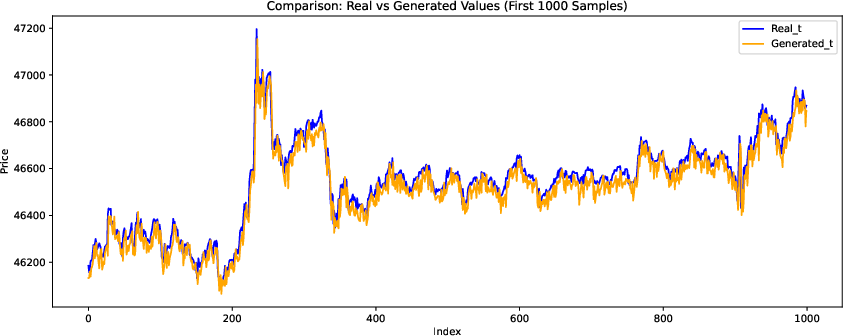

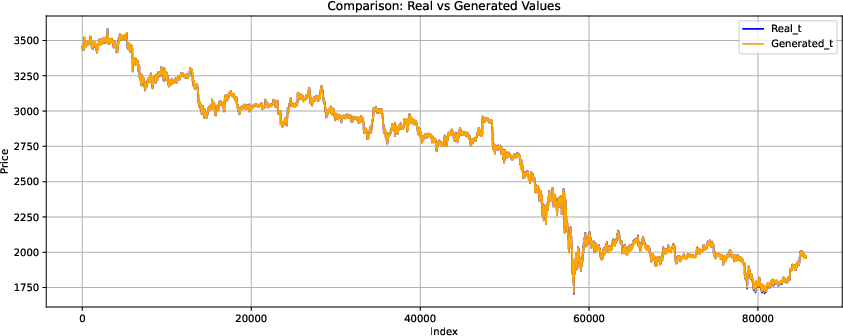

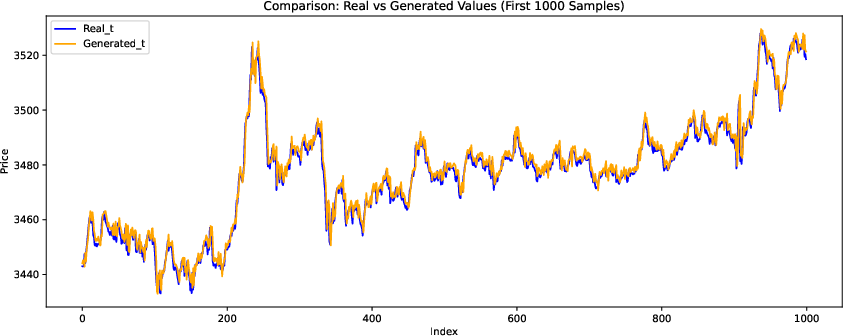

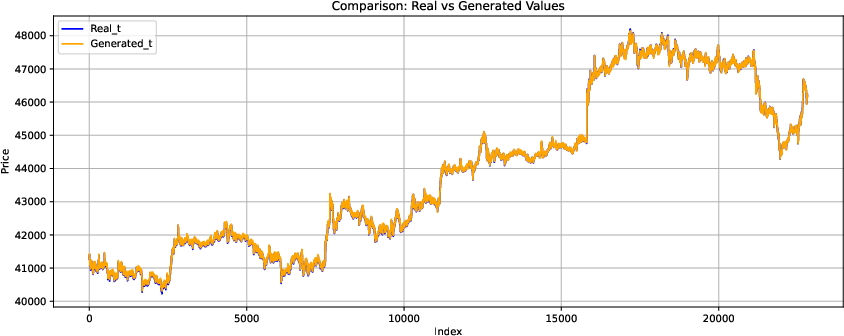

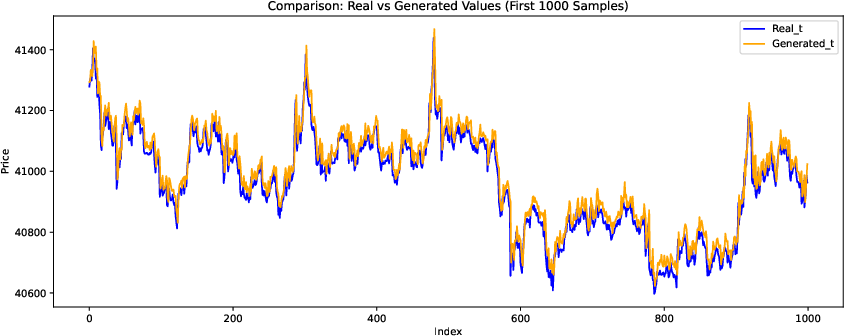

Representative results for BTC and ETH over the observed regimes are visualized in (Figure 5, Figure 6, Figure 7, Figure 8):

Figure 5: BTC closing price—original vs. CGAN-generated series in the first high-volatility period.

Figure 6: ETH closing price—original vs. CGAN-generated series, first period.

Figure 7: BTC price dynamics—capturing crash and recovery patterns during the second period.

Figure 8: ETH series in the second regime, synthetic data closely following real market swings.

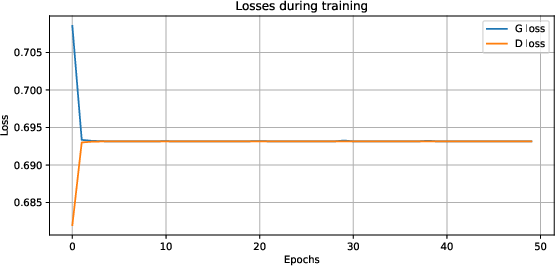

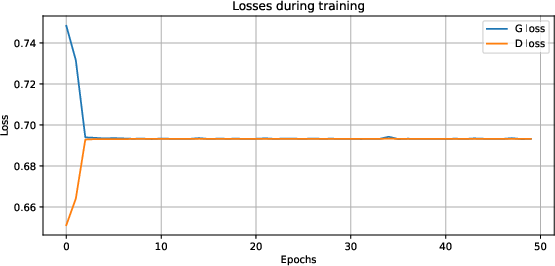

Training Dynamics

Training convergence and adversarial learning dynamics are confirmed through generator/discriminator loss plots, consistently demonstrating non-divergence and smooth opponent adaptation in all three regime-specific sessions (see Figure 9 for BTC as an example):

Figure 9: Generator and discriminator loss trajectories for BTC, confirming stable minimax training.

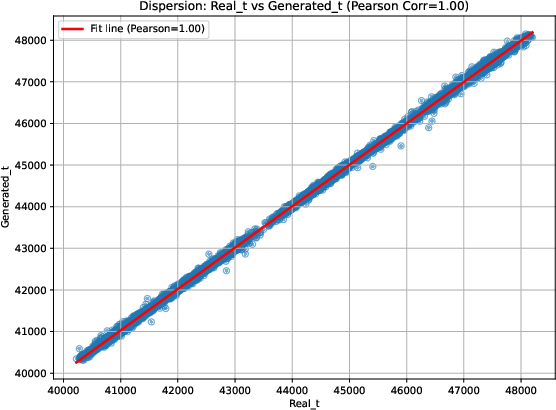

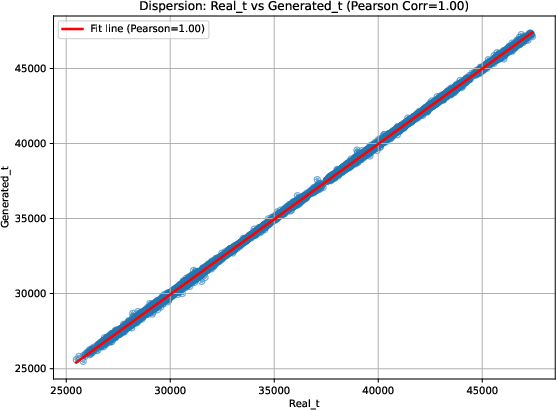

Statistical Fidelity

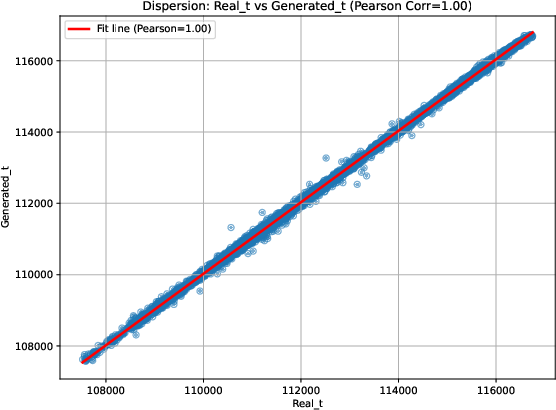

Scatter plots comparing real and synthetic values (e.g., Figure 10 for BTC; similar for ETH and XRP) show almost perfect alignment along the identity line. Visualizations show both the preservation of long-range market structure and short-term fluctuation.

Figure 10: BTC: Dispersion plot, synthetic vs real—tight clustering on the identity line, indicating high-fidelity generation.

Asset- and Regime-Specific Analysis

The model demonstrates asset-dependent effectiveness:

- BTC: Synthetic series exhibit robust fidelity to both micro-structure and macro-trends, superior to other assets, facilitated by BTC’s market efficiency and lower relative noise.

- ETH: Slight underestimation of volatility spikes, as CGAN tends to smooth heavy-tailed shocks—a known limitation in adversarial approaches for regimes with persistent abrupt innovations.

- XRP: Accurate in local structure but somewhat more sensitive to noise, reflecting its greater exposure to regulatory and speculative events not fully encoded by endogenous price history.

This asset differentiation is consistent with prior findings on neural forecasting difficulty for less liquid, highly nonstationary series [Wiese et al. 2020, Zhang et al. 2021].

Theoretical and Practical Implications

From a theoretical perspective, the results reaffirm the practical suitability of hybrid adversarial-recurrent architectures for complex, nonstationary financial time series. By conditioning on lagged values, these models are effective at emulating autocorrelation and regime transitions in crypto-assets.

Practically, such synthetic data can support:

- Robust anomaly and risk event detection—synthetic augmentations enable balanced training under privacy constraints

- Algorithmic trading and stress testing—generation of plausible alternative market paths for Monte Carlo evaluation

- Data sharing between institutions—circumventing privacy and regulatory hurdles via faithful synthetic alternatives

- Benchmarking of anomaly detection or fraud systems—providing labeled data sans disclosure of proprietary flows

An important methodological finding is the role of normalization (StandardScaler) and carefully chosen window size for temporal conditioning in stabilizing adversarial training for high-frequency financial data.

Future Directions

Potential avenues include integrating exogenous event annotation for more robust shock generation, experimenting with alternative losses (e.g., Wasserstein) to address volatility underestimation, and asset-specific conditioning to further reduce residual error. Expansion to quantum GANs, transfer learning for low-liquidity assets, and joint training on both spot and derivative markets would generalize applicability.

Conclusion

The work provides strong evidence that CGANs with LSTM generators can generate synthetic cryptocurrency price series that are statistically and dynamically consistent with real market data, especially for mature, liquid assets like BTC. The extremely high correlation between synthetic and real data across volatile regimes underscores the feasibility of deep generative models for privacy-preserving financial simulation. Continued advances in conditional generation are expected to further support anomaly detection, backtesting, and risk management in digital asset markets.

Reference: "Synthetic data in cryptocurrencies using generative models" (2604.16182)