- The paper presents a unified framework for Generalized Autoregressive Binary (GAB) models that captures both linear and nonlinear dependencies in binary time series.

- It establishes conditions for strict stationarity, uniqueness, and geometric ergodicity via Lipschitz contraction, extending the results to network interactions.

- It rigorously derives Poisson autoregression from aggregate binary events under rare-event scaling, validated by empirical analysis with S&P 100 tail events.

Generalized Autoregressive Multivariate Models for Binary and Count Data

The paper develops a unified framework for Generalized Autoregressive Binary (GAB) processes, where each dimension of a multivariate binary time series evolves as a Bernoulli random variable with a time-varying success probability. The probability dynamics incorporate both linear and nonlinear dependencies on past observed outcomes and latent probabilities, enabling flexible autoregressive feedback akin to GARCH models, but tailored to binary data. This recursive structure is extended to incorporate cross-sectional interactions and networks, accommodating a wide range of dependence structures in large panels.

Key to the theoretical development, the authors establish the existence of strictly stationary solutions for all parameter values by exploiting the bounded support of the binary variables and continuity of the evolution function. They further prove uniqueness and geometric ergodicity via a coupling argument under a Lipschitz contraction condition—criteria that generalize standard GARCH stationarity conditions without requiring transformations mapping probabilities to R.

Examples illustrate model flexibility, from classical linear GAB(s,q) forms, which parallel standard GAS models, to nonlinear and interaction-driven structures, including exchangeable, interactive, and network-based GAB models. This generality facilitates the modeling of various economic, financial, and sociometric phenomena where interdependence and rare event clustering are salient. The stochastic properties of the process—including unconditional moments and stationarity boundaries—are expressed in closed form for several cases.

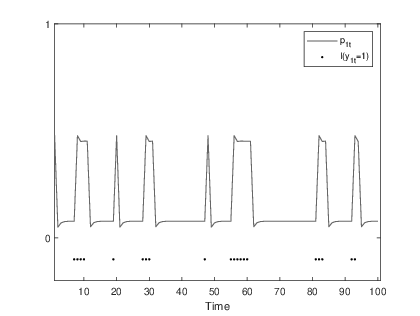

Figure 1: Nonlinear GAB(1,1) probability trajectories, highlighting nonlinear feedback mechanisms in binary series.

Aggregation Theory: Micro-foundations for Poisson Autoregression

A central theoretical contribution is the rigorous derivation of Poisson autoregression (INGARCH) as the aggregate limit of multivariate GAB processes under rare-events scaling. As the number of series N grows and individual success probabilities vanish (order $1/N$), the sum of binary outcomes converges in finite-dimensional distributions to a Poisson process with autoregressive intensity. The limit recursion for the Poisson intensity embodies both linear and nonlinear effects, depending on the specification of micro-level probability dynamics, and allows for the survival of complex feedback from aggregate counts.

The aggregation theory is robust to network structures: provided the network is doubly stochastic and sufficiently dense, heterogeneous interaction weights become asymptotically irrelevant, and the aggregate dynamics are fully captured by mean coefficients. The explicit mapping between micro parameters and Poisson autoregressive parameters provides a micro-foundation for widely used count models and clarifies parameter identification in panels with substantial cross-sectional dimension.

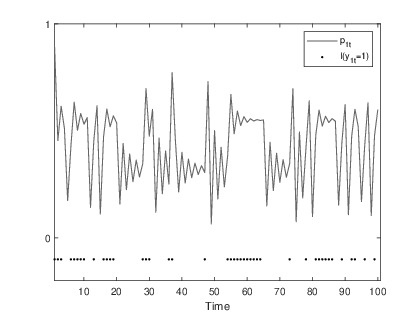

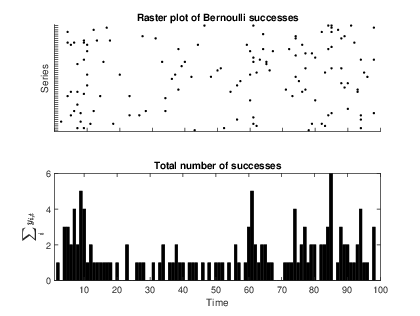

Figure 2: Illustration of aggregation—individual and aggregate binary successes under interactive GAB driving Poisson-like aggregate dynamics for N=50.

Estimation Procedures and Asymptotic Properties

The authors detail maximum likelihood estimation (MLE) for the GAB model, establishing consistency and asymptotic normality of the estimators in the moderate-probability regime where probabilities are bounded away from $0$ and $1$. Practical issues regarding initialization and identification are addressed, showing that contraction properties ensure negligible effects from unobserved initial probabilities.

In the rare-event regime where aggregate counts are well-approximated by a Poisson process, they demonstrate that the Poisson likelihood applied to aggregate data serves as a natural estimator. Importantly, the paper shows how, in homogeneous settings, the Poisson parameters can be mapped back to interpretable micro-level binary dynamics, preserving interpretability and identification.

Covariate Extension and Generalizations

The GAB framework is extended to handle exogenous covariates, with guidelines for how individual and aggregate covariate effects are scaled under rare-events limits. Both fixed- and growing-dimension covariate panels are treated, including decompositions into common and idiosyncratic components. The same contraction and stationarity results apply, as conditioning on shared covariates preserves the requisite properties for ergodicity.

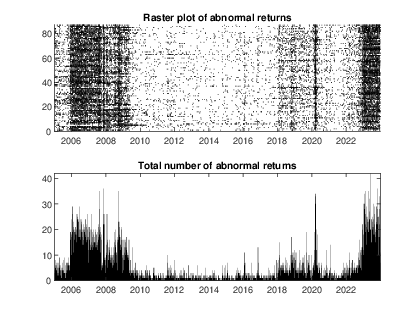

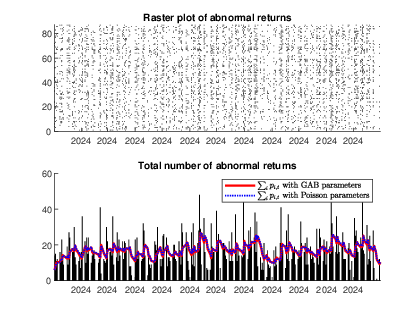

Empirical Analysis: S&P 100 Tail Event Clustering

The empirical application models daily returns of 87 S&P 100 constituents (2005–2025), focusing on days with idiosyncratic returns falling in the bottom 5% (tail events). The authors fit the interactive GAB model with panel-specific and cross-sectional interaction effects to the binary outcome of tail event occurrence, and contrast estimates with those from the aggregate Poisson approach. The findings demonstrate:

- Micro and macro (Poisson) parameter estimates closely align, supporting the theoretical aggregation mapping.

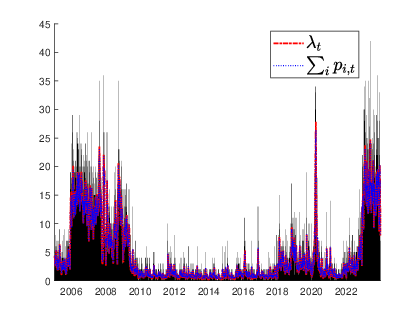

- The filtered Poisson intensity tracks the sum of individual series probabilities with high fidelity in-sample, validating the Poisson limit.

- Out-of-sample, the granular GAB model (with heterogeneous parameters) achieves superior forecasting accuracy relative to the Poisson and naive benchmarks, affirming the value of modeling cross-sectional heterogeneity, even when aggregation gives similar mean intensities.

Figure 3: Raster of S&P 100 tail events: clustering in crisis periods motivates interactive specification.

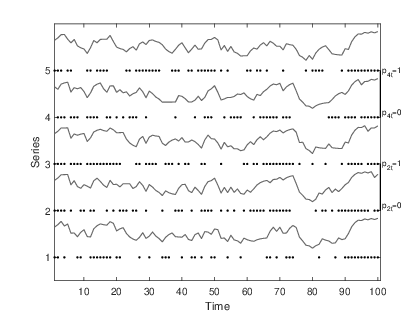

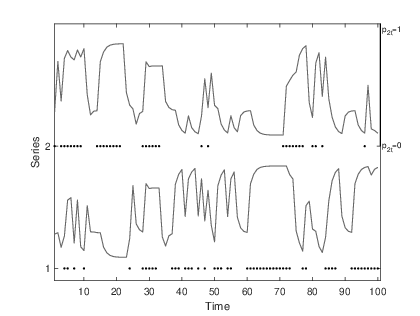

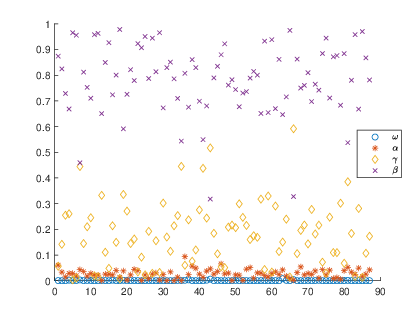

Figure 4: Estimated interactive GAB coefficients for 87 stocks, showing the distribution and magnitude of idiosyncratic and cross-sectional feedback.

Figure 5: In-sample fit—aggregate Poisson intensity tracks sum of GAB probabilities, showcasing model alignment.

Implications and Future Research

The results have several implications:

- Provides micro-foundations for integer-valued GARCH/Poisson autoregression, justifying their use in count data aggregation from rare binary events with endogenous feedback and network effects.

- The stationarity and ergodicity results establish theoretical guarantees for inference in nonlinear, networked binary panels—critical for reliable applications in finance (systemic risk, portfolio default), economics (dynamic binary choice), and social sciences (network diffusion).

- The explicit mapping between micro and aggregate parameters, and the quantification of information loss in aggregation, inform optimal estimation strategies and the design of composite likelihood approaches.

- Empirical superiority of the full GAB likelihood suggests that, even under aggregation, preserving heterogeneity can yield tangible forecasting improvements.

Potential extensions include the joint large-N, large-T asymptotic theory for estimator properties, development of composite likelihoods leveraging both micro and macro likelihoods, and applications to large-scale binary panels in administrative, financial, and sociometric data.

Conclusion

The paper articulates a broad and rigorous framework for multivariate binary autoregressive modeling, uniting micro-level GARCH-inspired feedback, cross-sectional and network interactions, and rare-events aggregation into a tractable and estimable theory. The link to Poisson autoregressive models not only provides a foundation for established count time series methodologies but also guides best practices in the empirical modeling of rare binary events in large heterogeneous panels.