- The paper presents a framework integrating dispatch optimization and CVaR metrics to assess and mitigate long-term tail risks in renewable power systems.

- It employs a multi-timescale Copula model to generate scenarios that capture extreme, rare events missed by traditional methods.

- Experimental results on a modified IEEE-39 bus system validate that adaptive storage policies can effectively reduce emergency supply costs under abnormal conditions.

Dispatch-Embedded Long-Term Tail Risk Quantification and Mitigation in Renewable Power Systems

Introduction

The increasing penetration of renewable energy (RE) has heightened the need for methodologies that robustly assess and mitigate long-term tail risks in power systems. The pronounced seasonality and extreme variability of RE, such as the stark seasonal swings of PV and wind output in European scenarios, can induce persistent shortfall events that are inadequately captured by short-term or simplistic long-term models. Traditional scenario-based approaches often downplay the probabilistic impact of multiscale RE dependence and overlook how realistic dispatch strategies interact with these uncertainties. The paper "Dispatch-Embedded Long-Term Tail Risk Assessment and Mitigation via CVaR for Renewable Power Systems" (2604.00926) directly confronts these gaps. The authors present a comprehensive framework that systematically embeds dispatch optimization within a scenario-based tail risk assessment methodology underpinned by Conditional Value-at-Risk (CVaR), and develops a feedback-controlled dispatch adaptation to mitigate emergent risk under high-impact, low-probability events.

System Model and Dispatch Framework

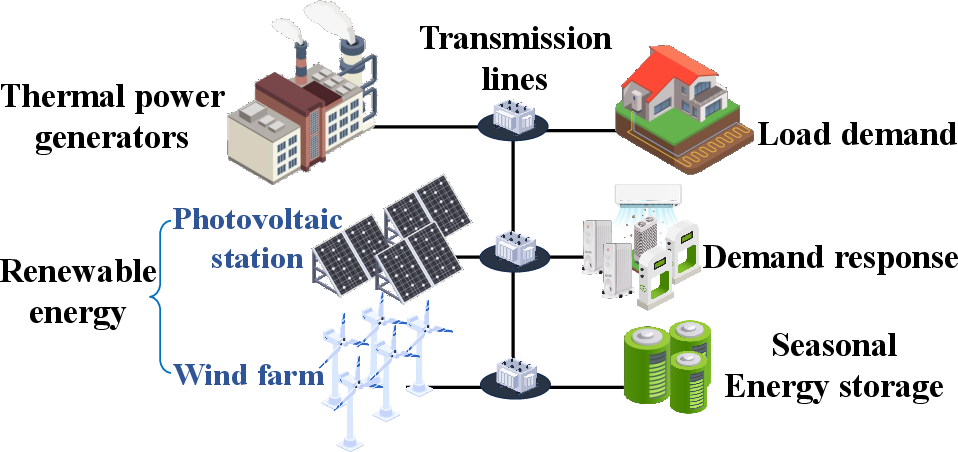

The paper delineates a renewable-dominant power system incorporating thermal power generators (TPGs), storage (SES), demand response (DR), and an explicit temporal structure that supports both short- and long-term decision-making. The system is operated under a set of detailed technical constraints: start-up/shut-down logic, resource capacities, ramp constraints for TPGs, charge/discharge and SoC tracking for SES, and explicit power flow and load balance constraints. The objective is a cost-weighted dispatch portfolio that includes start-up, de-commitment, energy, storage degradation, DR cost, and most critically, high-penalty emergency supply for unsatisfied load.

Figure 1: Schematic of the renewable-rich power system with explicit modeling of TPGs, SES, DR, LD, and power flows.

Multi-Timescale Copula Scenario Generation

A key foundation of the risk assessment methodology is its approach to long-term scenario modeling. Rather than relying on historical clustering or Monte Carlo samples—which fail to sufficiently populate tails or capture multivariate, persistent extremes—the framework applies a multi-timescale Copula-based stratagem. The process aggregates historical generation and demand data at a coarse timescale (e.g., weekly or daily), models their dependencies (including joint extreme correlations) via Copulas, and then reconstructs fine-resolution scenario traces via conditional sequence generation and rescaling.

Figure 2: Architecture of the evolution-based risk assessment model, integrating Copula-based scenario generation with rolling-horizon dispatch.

This approach yields representative scenario sets that:

- Reproduce both inter-annual/seasonal nonstationarity and short-term variability,

- Accurately reflect the coupled, plausible but unobserved rare events,

- Provide a sufficient basis for severe tail risk quantification.

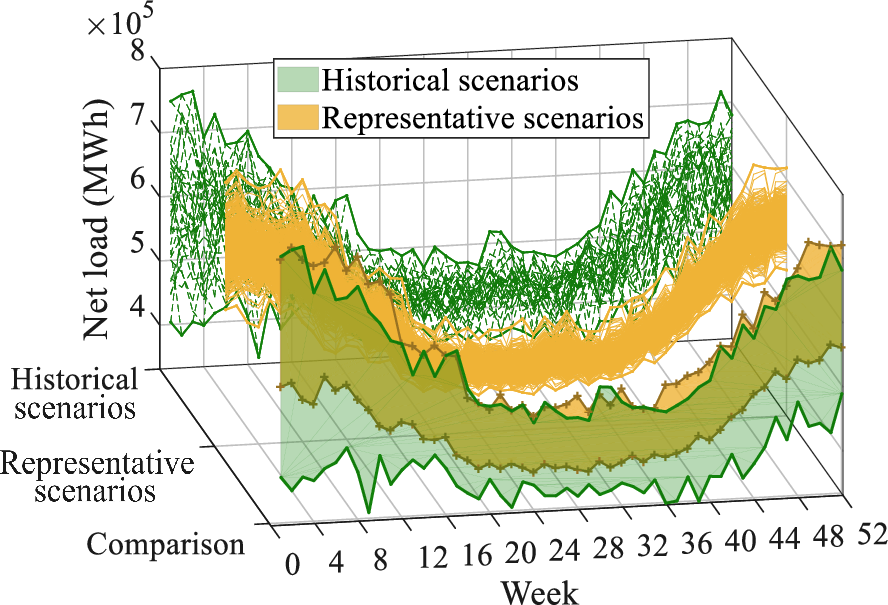

The model demonstrates that generated representative net load scenarios possess characteristics and extremes not present in historical traces, indicating improved sampling of risk-relevant conditions.

Figure 3: Comparative analysis of net load profiles reveals the representative scenario set embeds more diverse and extreme events than the historical sample.

CVaR-Based Tail Risk Assessment Embedding Realistic Dispatch

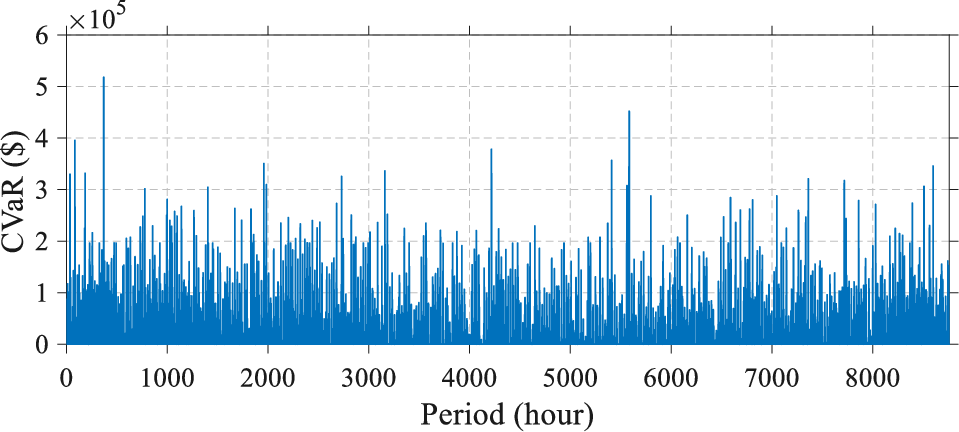

The core of the risk quantification strategy is an evolution-based, dispatch-embedded simulation framework. For each generated scenario, a rolling-horizon dispatch model resolves the operational allocation of TPGs, SES, and DR subject to all constraints, simultaneously enforcing long-term storage SoC tracking. Emergency supply instances incur a substantial cost, serving as the operational proxy for tail risk events.

After evolving all scenarios through this dispatch, the sequence of emergency energy costs is empirically collated. The CVaR at confidence level α is then computed period-wise, providing a coherent, scenario-driven risk metric that is sensitive to both event probability and magnitude. By comparing the period-specific CVaR to pre-set risk thresholds, the framework identifies specific times at which dispatch policy adaptation is required to constrain tail risk.

Controlled Evolution-Based Risk Mitigation

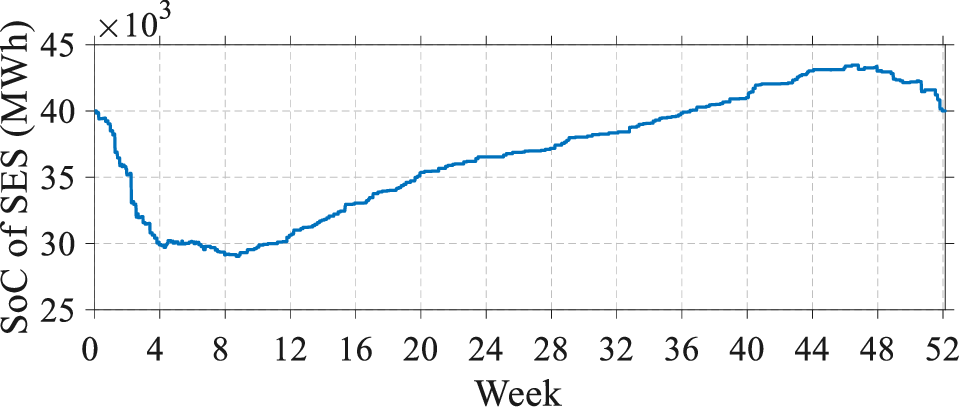

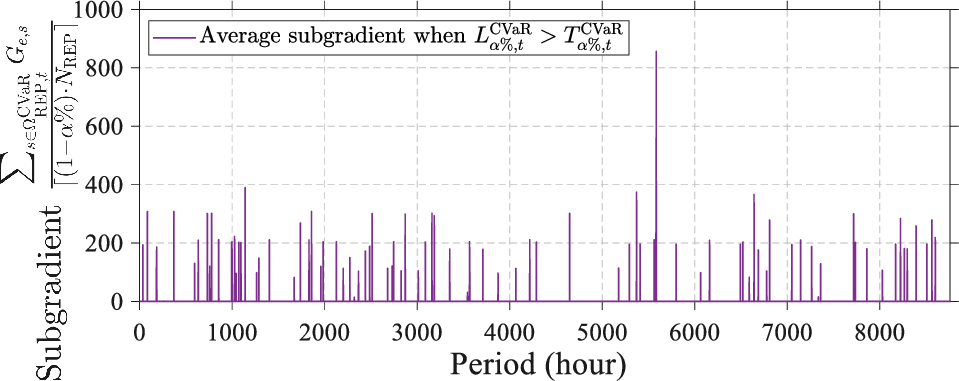

The mitigation strategy is formulated as an iterative feedback loop. When the computed CVaR exceeds its threshold in any period, the algorithm computes the subgradient of emergency cost with respect to the reference SoC level for SES. This gradient provides a direction to adapt the storage policy such that risk is explicitly suppressed. Scenarios driving the CVaR (“tail” scenarios) inform the direction and magnitude of policy correction, allowing targeted discharge actions precisely during periods of highest systemic vulnerability.

The method ensures any update moves the policy toward reducing CVaR, exploiting the linearized sensitivity captured in the subgradient for practical, computationally tractable real-time adaptation.

Figure 4: Evolution of SES SoC setpoints, corresponding CVaR trajectory, and subgradient-driven policy updates illustrate feedback-controlled tail risk mitigation.

Experimental Results and Implications

The experimental demonstrations are conducted on a modified IEEE-39 bus system with significant wind and PV penetration, and realistic 30-year German renewable and load traces serve as the data source. Generation of 200 representative yearly scenarios reveals the enhanced ability of the Copula model to span plausible extreme events. The dispatch evolution model identifies time windows where tail risk, as measured by emergency supply CVaR, exceeds the operational threshold, and quantifies the SoC adaptation required.

Quantitatively, the framework:

- Achieves scenario-driven identification of long-term vulnerability windows,

- Provides operational feedback (SES setpoint adaptation) that, when executed, directly reduces the realized system risk profile,

- Accurately simulates coupled, persistent extreme conditions that would be missed by historic-only or single-timescale methods.

The study establishes that embedding realistic operational policies within risk assessment is essential for accurate risk quantification and robust tail event preparedness. The Copula-enhanced scenario set eliminates the optimism bias of naive scenario generation, while the evolution-based mitigation approach ensures response capability is dynamically targeted toward maximal systemic benefit.

Theoretical and Practical Implications

On the theoretical level, the integration of a multiscale Copula model and evolution-based risk assessment provides a formal, computationally tractable mechanism to propagate high-dimensional uncertainty into actionable, dispatch-driven risk metrics. By utilizing subgradient-based policy adaptation, the approach bridges scenario-based simulation and gradient-driven optimization, opening pathways for future reinforcement learning or distributed feedback control schemes.

Practically, the methodology is directly applicable to large-scale system planning and operations where reliability and regulatory compliance hinge upon quantifiable assurance against rare but destructive events. The framework can be adapted to anticipate the increasing share of renewables, increased sector coupling (e.g., hydrogen, EVs), and higher network complexity. Future work can focus on accelerating scenario generation, leveraging forecast information, and integrating dynamic risk thresholds responsive to system state and external drivers.

Conclusion

The paper presents a rigorous framework for dispatch-embedded long-term tail risk assessment and mitigation in renewable-rich power systems, addressing the limitations of prior approaches by embedding realistic operational strategies and leveraging advanced scenario generation techniques. The integration of CVaR as a risk-metric, multi-timescale Copula modeling, and feedback-controlled dispatch adaptation provides an effective tool for operational and planning contexts. The approach sets a direction for future research focused on the confluence of robust statistics, multi-horizon optimization, and real-time risk management for resilient energy systems.