- The paper introduces a weight-centric abstraction that unifies research, backtesting, and live execution to minimize deployment gaps.

- It employs a modular design integrating data processing, strategy construction, and risk management, validated across historical and paper trading scenarios.

- Empirical results demonstrate improved risk-adjusted returns and reduced drawdowns, highlighting the system's operational resilience.

FinRL-X: An AI-Native Modular Infrastructure for Quantitative Trading

Introduction

"FinRL-X: An AI-Native Modular Infrastructure for Quantitative Trading" (2603.21330) introduces a system architecture that addresses major deployment gaps characteristic of both academic and production quantitative trading pipelines. The framework emphasizes deployment consistency through a weight-centric abstraction, modular composability, and a unified interface from offline research to live execution. Compared to prior frameworks—which are typically either modeling-centric or engineering-centric—FinRL-X is designed as a comprehensive, open-source infrastructure explicitly engineered for reproducibility, integration, and operational resilience.

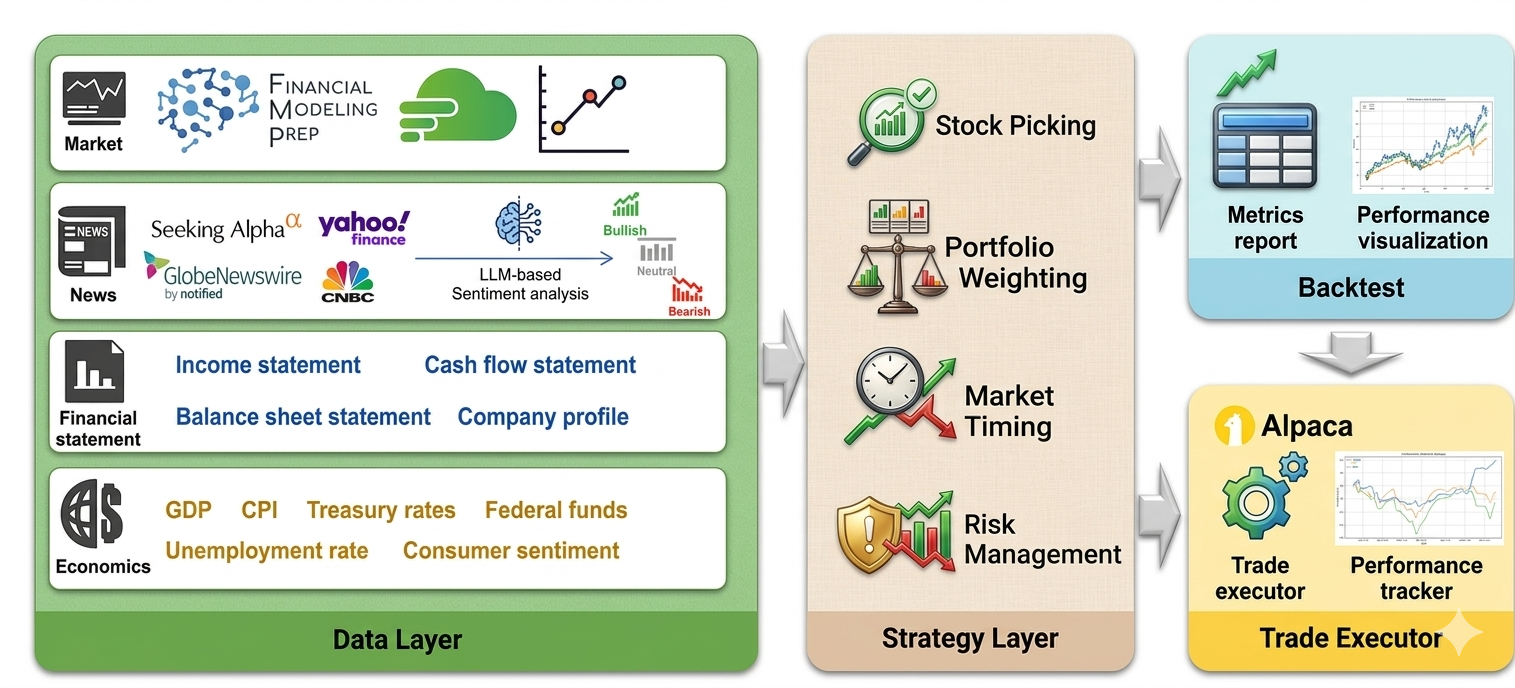

Figure 1: A layered, end-to-end trading architecture that unifies data processing, strategy construction, backtesting, and broker-integrated execution within a consistent pipeline.

Academic frameworks for systematic trading frequently underrepresent the practical challenges involved in the transition from research to live deployment. Existing open-source systems (e.g., Backtrader, Zipline, Qlib, TradingAgents, TensorTrade) are limited to isolated pipeline stages—backtesting, ML research, or broker integration—without formalizing consistency between research evaluation and operational execution. This produces significant behavioral drift due to simplified historical simulation assumptions (e.g., latency-free fills, naive cost models) and operational failures in live environments (e.g., broker API variance, infrastructure risk, recovery logic), as formalized in the paper.

LLM-based tools such as BloombergGPT and FinGPT have advanced financial text modeling but remain decoupled from system integration and broker-realistic deployment. The lack of a unified protocol induces overfitting to research-specific assumptions and hinders the reproducibility and robustness of ML-based strategies.

FinRL-X System Architecture

FinRL-X adopts a distinctly modular, layered architecture that decomposes the end-to-end trading process into data, strategy, backtesting, and execution layers. The core system innovation is the "weight-centric" interface, in which all strategy logic outputs a target portfolio weight vector at each decision time. This enforces interface stability: every module downstream—backtester, broker executor, risk manager—operates only on abstract weights, avoiding brittle coupling to signal formats or order-generation idioms.

The strategy layer is further decomposed into contract-preserving modules: stock selection, portfolio allocation, timing adjustment, and portfolio risk overlay, all composed as transformations of data into executable weights. Model-based and rule-based approaches (such as DRL allocation, mean-variance optimization, and LLM-based news sentiment) are interchangeable, preserving output semantics and validation logic.

Deployment Consistency: Backtesting, Paper, and Live Gaps

The framework formalizes two deployment gaps: (1) the backtest-to-paper gap, where simulated environments are systematically optimistic due to unrealistic execution and cost assumptions, and (2) the paper-to-live gap, where even broker-integrated simulations omit crucial operational risks, fill uncertainty, and infrastructure idiosyncrasies. Unlike prior systems, FinRL-X actively designs for these gaps: it aligns simulation logic, order generation, and state management with the live broker environment, logs reconciled realized and target portfolios, and applies persistent infrastructure for failure recovery and post-trade accounting.

By maintaining the unified weight interface across all stages, the architecture ensures that the exact same logical portfolio, risk, and timing modules are validated in both research and deployment. This reduces behavioral divergence and empirically improves the fidelity of research results under live constraints.

Empirical Evaluation and Ablation Results

The paper provides comprehensive experimental validation using U.S. equities and ETFs, standardizing SPY and QQQ as benchmark indices. The evaluation spans historical backtests (January 2018–October 2025), broker-integrated paper trading (October 2025–March 2026), and controlled ablation studies.

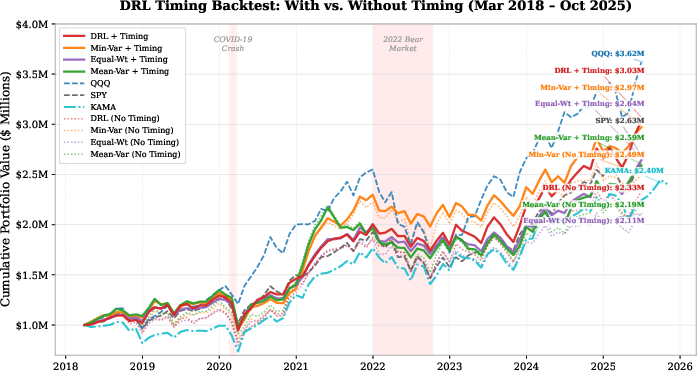

Timing modules are shown to systematically improve risk-adjusted returns across classic and DRL-based allocations by modulating portfolio exposure (Sharpe uplift from 0.55 to 0.89 under DRL; maximum drawdown reduction), whereas base allocations (equal, mean-variance, minimum-variance, DRL) serve as controls. The ablation confirms that timing and risk overlays can be incorporated modularly without pipeline changes.

Figure 2: Ablation study showing that incorporation of a timing adjustment module improves cumulative return and drawdown profile for DRL-based allocation, compared to base DRL and SPY benchmark.

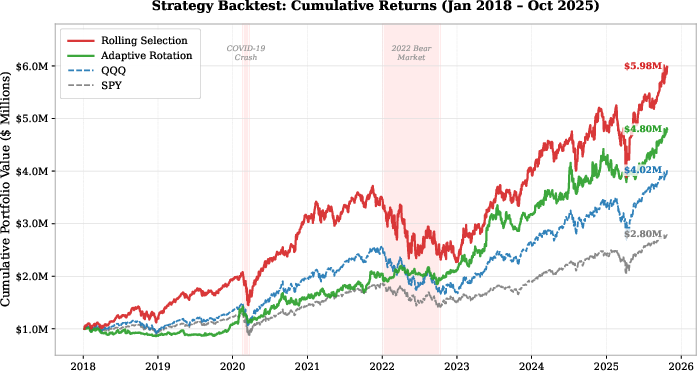

Portfolio trajectory visualizations and out-of-sample metrics establish effectiveness and reproducibility across paradigms.

Figure 3: Comparison of cumulative portfolio trajectories for representative strategy classes relative to benchmarks under a standardized execution protocol.

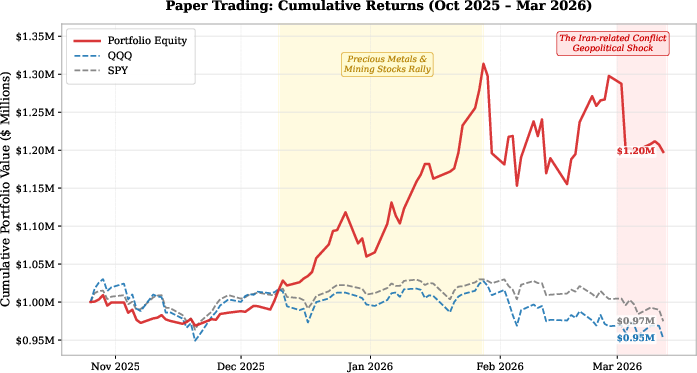

In live-paper trading emulation on Alpaca, an ensemble strategy (Rolling Selection plus Adaptive Rotation) yields a +19.76% total return (annualized 62.16%), Sharpe ratio of 1.96, and low drawdown, with consistently low order rejection and target-realized tracking error. The result demonstrates faithful execution and post-trade validation in a broker-live context, not just simulation.

Figure 4: Deployment-consistent execution and realized returns for the ensemble strategy relative to benchmarks during the Alpaca paper-trading window.

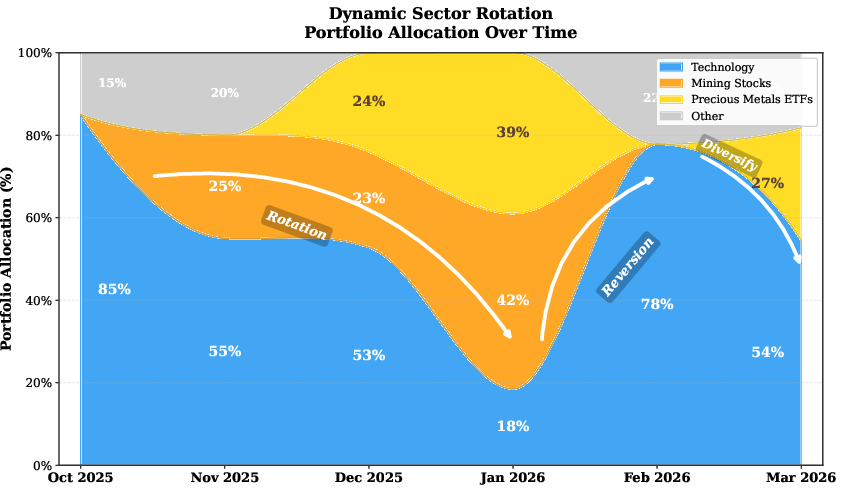

The allocation trajectory figure illustrates seamless modular delivery of dynamic regime-aware position sizes across asset groups, again highlighting pipeline consistency without architecture modification.

Figure 5: Portfolio allocation adjustments made by the weight-based framework during paper trading, demonstrating adaptable and modular allocation outputs.

A stress event involving a leveraged ETF highlights the criticality of real-world execution-aware risk overlays, motivating future enhancements in volatility scaling and instrument-specific constraint modules.

Implications and Future Directions

FinRL-X's design pushes systematic trading infrastructure toward an AI-native, research-to-deployment-consistent paradigm. By eliminating discrepancies imposed by interface drift and inconsistent module semantics, the framework establishes a reproducible foundation for scalable ML-based trading systems. This addresses both practical needs—seamless migration of strategy research to broker environments, operational resilience, robust monitoring—and enables more credible empirical research in financial ML.

From a theoretical viewpoint, forcing a single canonical portfolio weight abstraction eliminates many confounding factors (e.g., signal translation, order logic) that contaminate classical backtesting studies. The architecture can be extended to accommodate more complex asset classes (options, futures, credit), multi-agent or adversarial simulation, and advanced execution-aware RL strategies.

Potential next steps include integration of multi-asset support, limit order book simulation, real-time distributed streaming, and LLM-based agents driving adaptive strategy logic under the same unified protocol.

Conclusion

FinRL-X establishes a robust, modular, and deployment-consistent foundation for quantitative trading, unifying the research, backtesting, and live execution workflows through a principled weight-centric interface. It enables reproducible and operationally resilient AI-driven trading pipelines, validated empirically across simulated and broker-integrated environments. The compositional flexibility and focus on deployment realism make FinRL-X a benchmark system for research and practice in systematic asset management.