SPX-VIX Risk Computations Via Perturbed Optimal Transport

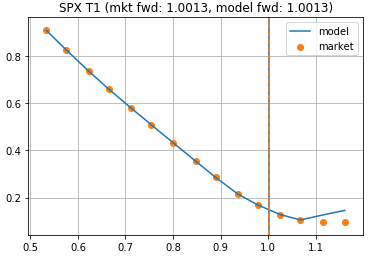

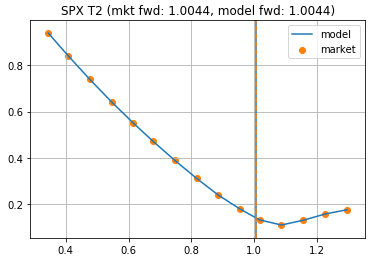

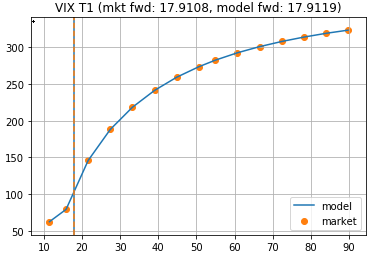

Abstract: We propose a model independent framework for generating SPX and VIX risk scenarios based on a joint optimal transport calibration of their market smiles. Starting from the entropic martingale optimal transport formulation of Guyon, we introduce a perturbation methodology that computes sensitivities of the calibrated coupling using a Fisher information linearization. This allows risk to be generated without performing a full recalibration after market shocks. We further introduce a dimension reduction method based on perturbed optimal transport that produces fast and stable risk estimates while preserving the structural properties of the calibrated model. The approach is combined with Skew Stickiness Ratio(SSR) dynamics to translate SPX shocks into perturbations of forward variance and VIX distributions. Numerical experiments show that the proposed method produces accurate risk estimates relative to full recalibration while being computationally much faster. A backtesting study also demonstrates improved hedging performance compared with stochastic local volatility models.

Paper Prompts

Sign up for free to create and run prompts on this paper using GPT-5.

Top Community Prompts

Explain it Like I'm 14

What is this paper about?

This paper is about pricing and managing risk for two linked markets:

- SPX options (bets on where the S&P 500 stock index might be in the future), and

- VIX options (bets on the future level of volatility, which is like how “bumpy” the market might be).

Because VIX is built from SPX’s future variability, these two markets should move together in a consistent way. The authors present a new, fast, and model‑free way to both match current market prices and compute how those prices change when the market moves (the “risk” or “Greeks”)—without having to rebuild the whole model every time.

What questions do the authors ask?

In simple terms:

- How can we match SPX and VIX option prices at the same time without assuming a complicated model for volatility?

- Once matched, how can we quickly estimate how VIX prices and risks change when SPX changes (and vice versa), without recalculating everything from scratch?

- Can we add realistic “rules of thumb” that traders observe—like how the shape of the VIX options curve shifts when the VIX level moves—into this model‑free setup?

How did they study it?

Think of this as a transport problem:

- Imagine you have piles of sand (the “probability” of different future outcomes of SPX and VIX), and you want to rearrange them so they match what the market’s option prices imply—while moving as little sand as possible and keeping things smooth. This is called optimal transport with an “entropy” twist (it prefers smoother, more spread‑out answers).

- The transport solution gives a “Gibbs distribution,” which is just a smart way to assign weights to scenarios so that current option prices are exactly matched.

The paper adds two key ideas:

- Linear Response (LR): fast risk from local geometry

- The final distribution belongs to an “exponential family,” a fancy way of saying that it’s controlled by a set of knobs (numbers) that ensure the match with market prices.

- The Fisher information matrix tells you how stiff these knobs are—like how a spring pushes back when you nudge it.

- If the market moves a tiny bit (like a small change in SPX implied volatility), the LR method uses the Fisher matrix to predict how all prices and risks change—without recalibrating. It’s like using the slope at a point to estimate a small move.

- Dimensional Reduction (DR): solving a smaller problem

- The full setup tracks three things together: SPX at an earlier time (S1), VIX (V), and SPX at a later time (S2).

- Under a “conditional invariance” rule (meaning one part doesn’t change when conditioned on others), they can keep the part linking S2 to (S1, V) fixed and just refit the smaller (S1, V) problem when markets move.

- This makes the calculations much faster but still financially consistent (no arbitrage).

Adding realistic smile dynamics (SSR)

- Traders observe that when the VIX future level moves, the VIX option smile (its slope/shape) shifts in a somewhat predictable way. This is called the Skew Stickiness Ratio (SSR): a number that measures how much the smile moves with the level.

- The authors embed a linearized version of SSR into the transport framework as simple linear rules. That way, when SPX changes and pushes the VIX level, the VIX smile also reacts in a trader‑realistic manner—without needing a heavy stochastic volatility model.

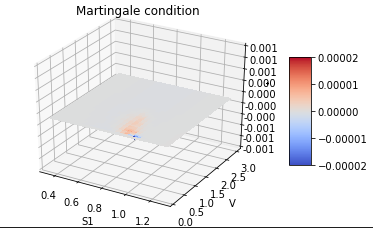

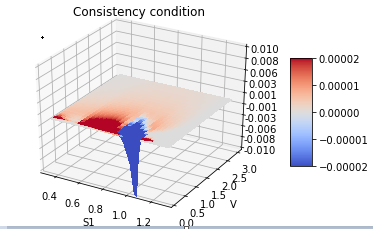

Financial consistency rules

- They enforce “martingality”: under risk‑neutral pricing, expected future SPX equals today’s SPX (no free lunch).

- They enforce “variance consistency”: VIX is tied to the SPX distribution’s future variability, so both must agree.

- These are treated as linear constraints so the math stays stable and fast.

What did they find, and why is it important?

Main results:

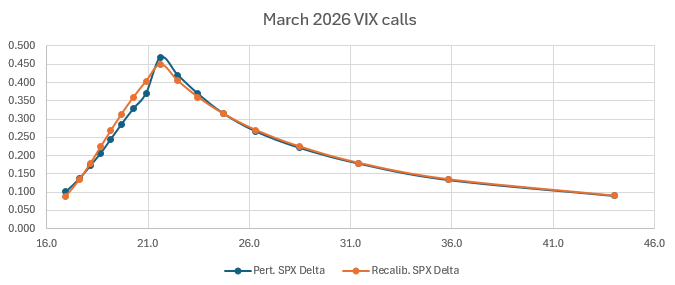

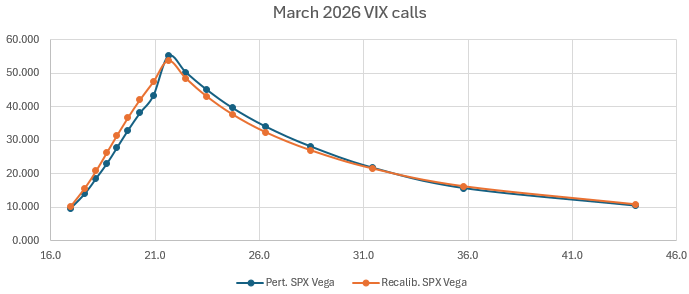

- Linear Response (LR) works: The LR method’s risk sensitivities (like how a VIX call changes when SPX volatility moves) closely match what you’d get by fully recalibrating—but at a fraction of the cost.

- Dimensional Reduction (DR) is fast and accurate: With the conditional invariance trick, they can cut the problem size and still produce reliable cross‑asset risks.

- SSR dynamics can be built in: The framework naturally incorporates VIX smile reactions (via SSR) as linear rules, matching how traders see the market move day‑to‑day.

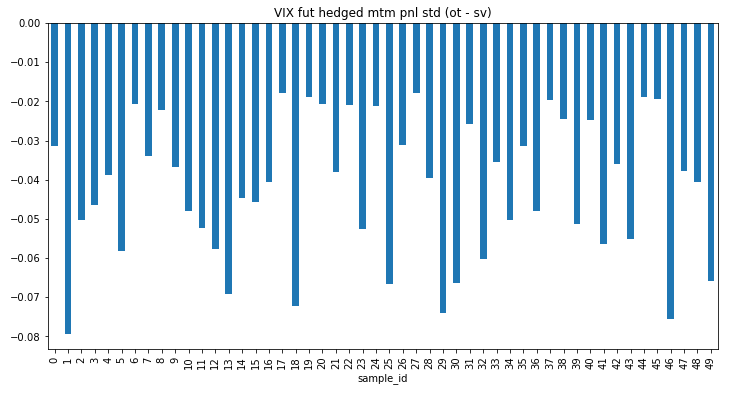

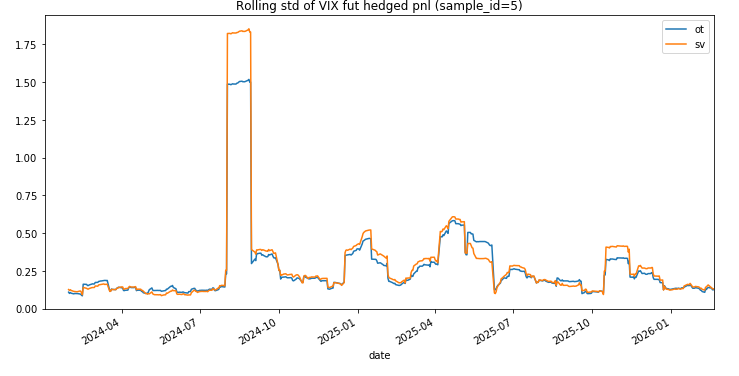

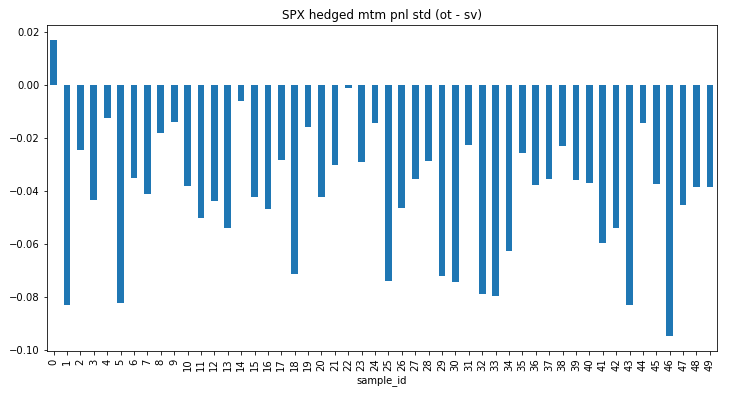

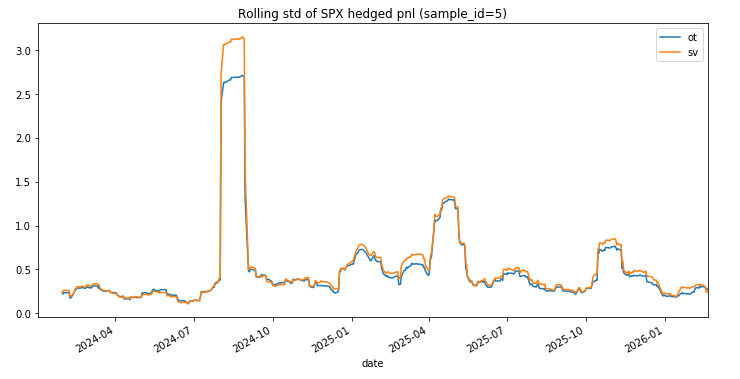

- Better hedging in tests: When they ran hedging backtests on random VIX option portfolios, the hedges built using their transport‑based risks produced lower hedged P&L volatility (especially in turbulent markets) than a benchmark stochastic volatility model.

Why it matters:

- Exact “statics”: You get a perfect joint fit to SPX and VIX option prices.

- Fast “dynamics”: You can get risk quickly without rerunning a heavy calibration.

- Realistic reactions: By adding SSR, the VIX smile moves the way practitioners expect when the VIX level changes.

What’s the potential impact?

- For traders and risk managers: Faster, more reliable cross‑asset Greeks (how VIX reacts to SPX moves) means better hedges and fewer surprises—especially when markets are jumpy.

- For quants: A unified, model‑free framework that handles both calibration and risk. No need to pick a specific volatility model or tune lots of parameters to fit two markets at once.

- For future research: This shows how geometry (via Fisher information) and optimal transport can power quick sensitivity analysis in other multi‑asset problems—potentially improving both speed and robustness in modern derivatives risk systems.

In short, the paper turns a powerful calibration tool (optimal transport) into a complete, practical engine for both matching SPX–VIX prices and generating fast, realistic risk—by smartly using the local geometry of the calibrated solution and by building in observed VIX smile behavior.

Knowledge Gaps

Knowledge gaps, limitations, and open questions

The paper introduces a Perturbed Optimal Transport (POT) framework for SPX–VIX risk, but several aspects remain uncertain or unexplored. The following list identifies concrete gaps and questions to guide future research:

- Lack of dynamic consistency beyond two dates: the framework is static/calibrational (on ). How to extend POT to multi-step or continuous-time settings so that path-dependent payoffs and dynamic hedging assumptions are internally consistent?

- Limited treatment of multi-maturity VIX term structure: the current formulation focuses on a single VIX window (e.g., ). How to impose variance-consistency constraints across multiple maturities and jointly calibrate/propagate risk for the full VIX term structure and cross-maturity smiles?

- Unclear mapping of SSR constraints into the transport measure: SSR is posed as a smile-dynamics rule in implied vol space, but the paper does not fully specify how to encode SSR as linear constraints on (the coupling). What are the exact linear functionals in that enforce SSR-consistent price changes for VIX options?

- Exogeneity and stability of SSR: SSR is introduced as an empirical, exogenous parameter. How to estimate SSR robustly across regimes, maturities, and moneyness, assess its stationarity, and propagate estimation uncertainty into risk?

- Heterogeneity of SSR with strike and maturity: the paper uses a single (local) linear SSR. Empirically SSR may vary with moneyness, term, and regime. How to generalize SSR constraints to be strike- and maturity-dependent while preserving convexity and tractability?

- Validation of linear SSR under large moves: the error bound is theoretical; there is no empirical study of how far the linearization holds under realistic stress moves. What thresholds should trigger second-order corrections or fallback to recalibration?

- Second-order risk usage: a second-order expansion is derived but not operationalized. How to compute efficiently in practice, quantify error bars for Greeks, and decide when second-order terms materially improve hedge quality?

- Conditional kernel invariance (DR) assumptions: the dimensional reduction relies on invariance of the conditional . What are sufficient conditions for this to hold in practice, and how large are errors when the assumption is violated?

- Error quantification for DR: no bounds are provided for price/Greek errors induced by DR. Can we derive computable a posteriori error controls to decide when DR is safe to use?

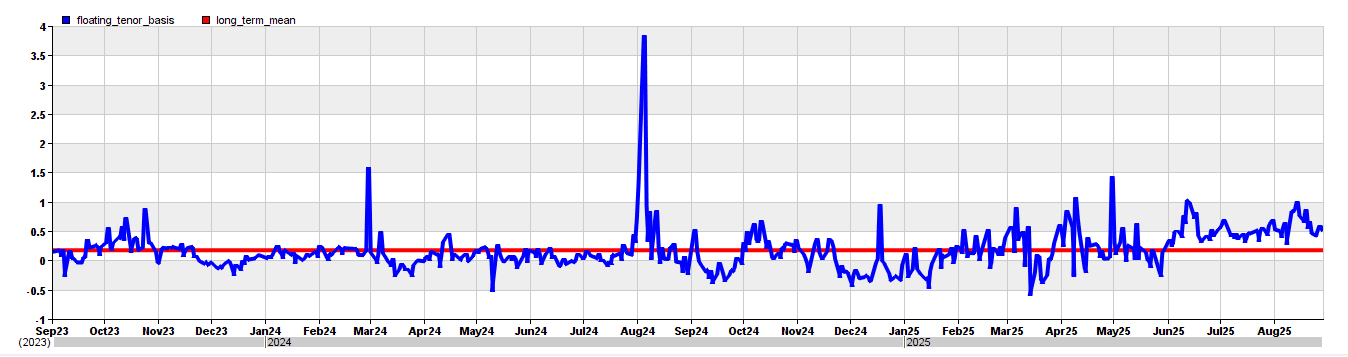

- Robustness to marginal inconsistency and basis: markets are often inconsistent (SPX forward variance vs. traded VIX futures). The paper acknowledges a basis but does not specify how it is imposed (hard vs. penalized constraints) or how basis uncertainty affects risk.

- Sensitivity to the prior measure : the entropic projection depends on the choice of prior, yet there is no guidance on prior selection (e.g., independence prior vs. model-based) or on how risks depend on that choice.

- Grid design and discretization error: risk and calibration quality depend on grid resolution and support truncation. How to select grids adaptively, assess discretization error in Greeks, and ensure stability at the tails?

- Fisher matrix conditioning and inversion: the Fisher information matrix can be large and ill-conditioned. What regularization, preconditioning, or low-rank approximations are needed, and how do they bias risk?

- Numerical scalability and performance: the paper claims efficiency but provides no complexity analysis for LR/DR vs. recalibration (memory, time, scaling with grid sizes). What are practical limits and optimization strategies (e.g., sparsity, parallelization)?

- Handling noisy and inconsistent option quotes: how to incorporate bid–ask, outliers, and microstructure noise in constraints? Are soft constraints or robust divergences preferable to hard linear constraints for stability?

- Arbitrage across surfaces beyond enforced constraints: while martingality and a log-contract identity are imposed, the framework does not address other no-arbitrage conditions (e.g., calendar/butterfly arbitrage across SPX and VIX surfaces and across maturities). How to incorporate broader consistency conditions?

- Interest rates, dividends, and carry: the exposition “ignores discounting for simplicity,” but practical deployment must handle non-zero rates/dividends and term structures. How do these affect constraints and risk propagation?

- Joint shock handling and causality: the method focuses on propagating SPX shocks to VIX via forward variance and SSR. How to handle VIX-led shocks (e.g., volatility events) and compute sensitivities to VIX-only perturbations coherently within POT?

- Inclusion of additional instruments: extension to variance swaps, VVIX, SPX variance futures, and options on multiple VIX futures is not discussed. How to augment constraints for a broader joint calibration and risk propagation?

- Out-of-sample and regime robustness: empirical validation and backtests are mentioned but not detailed (data, periods, cost assumptions, performance metrics). How robust are LR/DR Greeks to regime shifts (e.g., crisis periods) and to SSR changes?

- Hedging implementation details: there is no discussion of transaction costs, liquidity, and rebalancing frequency in backtests. How do POT-based hedges perform after trading frictions and slippage?

- Stress testing and nonlinearity: the linear response is local. How to design systematic stress tests (large spot/vol moves) and decide when to switch from LR/DR to full entropic recalibration?

- Choice of divergence: only KL (entropic) regularization is considered. Would alternative divergences (e.g., quadratic, χ², Wasserstein with entropy) yield more robust risks or better conditioning?

- Real-world vs risk-neutral dynamics: hedging performance depends on real-world dynamics, yet POT is calibrated under the risk-neutral measure. How to bridge measures (e.g., via filtering or Bayesian updates) for more realistic P&L distributions?

- Incomplete sections and formal details: the paper hints at “Compatibility With The Optimal Transport Linear Response System” for SSR but the exposition is incomplete. A precise derivation is needed to verify linearity, feasibility, and numerical implementation.

- Generalization to path-dependent and exotic payoffs: the framework prices/risk-manages payoffs measurable on ; extension to path-dependent exotics (barriers, cliquets) and multi-date risk remains an open problem.

- Calibration uniqueness under additional constraints: existence/uniqueness is proven for marginal constraints with positive prior, but not for the full set including martingale/variance and SSR constraints. What are the feasibility conditions and uniqueness guarantees in the augmented problem?

- Data latency and real-time deployment: the practicalities of running LR/DR in real time with streaming updates (quotes, surfaces) are not addressed. What update cadence and system design are needed for stable intraday risk?

Practical Applications

Immediate Applications

Below are actionable applications that can be deployed with today’s data and standard quantitative infrastructure, derived directly from the paper’s Linear Response (LR), Dimensional Reduction (DR), and SSR-constraint innovations.

- Finance (sell-side/trading): Intraday cross-greeks for SPX–VIX portfolios

- What: Replace “bump-and-recalibrate” with LR-based sensitivities using the Fisher information of the calibrated entropic MOT. Generate cross-greeks (e.g., VIX option sensitivity to SPX slice shifts) from a single linear solve rather than many recalibrations.

- How/Workflow:

- Calibrate the entropic MOT (Sinkhorn iterations) to SPX and VIX surfaces.

- Build the Fisher information matrix from the gauge-fixed dual potentials; pre-factorize it.

- Compute influence functions for portfolio payoffs; map marginal shocks to P&L via a matrix-vector product.

- Tools/Products:

- “POT Risk Engine” microservice for Greeks.

- Fisher-information dashboard for risk explainability (influence-function reports).

- Assumptions/Dependencies:

- High-quality, arbitrage-filtered SPX and VIX option surfaces; strictly positive priors.

- Small-perturbation regime for LR accuracy; invertible Fisher matrix after gauge fixing.

- Feasibility of constraints (martingale and variance consistency).

- Finance (sell-side/trading): Faster quote-to-hedge cycle for VIX options market making

- What: Deploy DR under conditional kernel invariance to reduce (S1, V, S2) to (S1, V), enabling near real-time repricing and hedging of VIX options as SPX moves.

- How/Workflow:

- Assume conditional invariance of S2|S1,V; re-solve a lower-dimensional entropic projection on (S1, V) after small market moves.

- Update hedges via precomputed mapping from SPX shocks to VIX smiles (SSR-embedded).

- Tools/Products:

- “DR Hedge Updater” for intraday hedging.

- Assumptions/Dependencies:

- Conditional kernel invariance holds locally; LR/DR accuracy in small moves.

- Robust SSR estimates for VIX term structure.

- Finance (sell-side/buy-side): Stress testing and scenario propagation across SPX→VIX

- What: Use LR sensitivities to propagate SPX shocks (e.g., parallel vol bumps, skew shifts) through forward variance to VIX futures and options in a model-independent manner.

- How/Workflow:

- Express regulatory or internal stress scenarios as marginal shocks.

- Apply LR influence functions to estimate VIX futures and option P&L quickly.

- Tools/Products:

- “OT Scenario Propagator” for cross-asset stress testing.

- Assumptions/Dependencies:

- Calibration admits martingality and variance-consistency; SSR constraints embedded for VIX smile dynamics.

- Finance (sell-side/buy-side): Hedging improvement for VIX portfolios

- What: Implement POT-based hedging strategies; paper’s backtests show reduced hedged P&L variance vs a benchmark stochastic volatility model, particularly in volatile regimes.

- How/Workflow:

- Use DR-generated SPX sensitivities to hedge VIX options dynamically.

- Monitor hedged P&L and adjust SSR parameters with rolling estimation.

- Tools/Products:

- “POT Hedging Strategy” module integrated with execution.

- Assumptions/Dependencies:

- Stable SSR estimation process; regular re-calibration cadence.

- Liquidity to implement SPX hedges and manage basis risk.

- Finance (risk/quant dev): Risk explainability and governance

- What: Influence-function reports quantify contribution of each marginal (e.g., SPX slice, VIX smile node) to portfolio risk—useful for model risk management and audit trails.

- How/Workflow:

- Store influence vectors at each calibration.

- Provide traceable mapping from specific market inputs to portfolio sensitivities.

- Tools/Products:

- “Influence Explorer” for model risk committees.

- Assumptions/Dependencies:

- Reliable storage pipeline for calibrated potentials and Fisher matrices.

- Controls for gauge fixing and numerical stability.

- Finance (infrastructure): Computational cost reduction

- What: Replace repeated full MOT recalibrations with one-time calibration + repeated linear solves; DR further cuts dimensionality.

- How/Workflow:

- Nightly full calibration; intraday LR/DR-based risk updates.

- Batch- and streaming-mode sensitivity updates.

- Tools/Products:

- GPU/CPU hybrid services for Sinkhorn and sparse linear algebra.

- Assumptions/Dependencies:

- Stable grids for (S1, V, S2); efficient linear algebra stack; monitoring for null-space handling.

- Academia: Reproducible research and teaching in model-free joint calibration

- What: Use POT as a lab platform for joint SPX–VIX calibration and sensitivity propagation demonstrating entropic projections and information geometry.

- How/Workflow:

- Build course labs that implement Sinkhorn, gauge fixing, Fisher matrix computation, and LR risk for simple portfolios.

- Tools/Products:

- Open-source notebooks (e.g., using Python OT libraries, autograd for Hessians).

- Assumptions/Dependencies:

- Access to historical option surfaces; careful discretization and regularization.

- Policy/Regulation: Transparent cross-asset risk capture for supervisory exercises

- What: Provide regulators or internal validation teams with model-independent, constraint-consistent cross-greeks for SPX–VIX risk transmission without parametric dynamics.

- How/Workflow:

- Submit LR-based sensitivity maps under specified standardized shocks.

- Demonstrate diagnostic checks for martingality and variance consistency.

- Tools/Products:

- “Constraint Diagnostics” reports (martingality and variance-consistency plots).

- Assumptions/Dependencies:

- Agreement on SSR estimation and acceptable bases between forward variance and VIX futures.

- Acceptance of small-perturbation linearization in supervisory contexts.

- Daily life/retail platforms: More stable VIX options pricing and tighter spreads

- What: Broker-dealers and retail platforms can use faster cross-greeks to maintain tighter quotes and reduce latency-induced mispricings on VIX options when SPX moves.

- How/Workflow:

- Integrate LR/DR sensitivities to update quotes and hedges automatically as SPX ticks.

- Tools/Products:

- Low-latency pricing service augmented with POT.

- Assumptions/Dependencies:

- Sufficient system performance; simplified grids suitable for retail-scale instruments.

Long-Term Applications

These require further research, scaling, or validation beyond the paper’s current scope, but are natural extensions of its findings and methods.

- Finance (multi-asset): Extending POT to other joint markets

- Use cases:

- Equity index vs. single-name vol coupling (index–component variance consistency).

- Rates: consistent joint calibration of swaption surfaces and realized variance proxies.

- Commodities/energy: options vs. forward variance indexes, if/when tradable.

- Tools/Products:

- Cross-market “OT Joint Calibrator” with LR risk modules.

- Assumptions/Dependencies:

- Existence of analogous variance-consistency constraints; sufficient liquidity in both legs.

- Design of appropriate financial constraints akin to SPX–VIX martingale/variance consistency.

- Finance (modeling): Nonlinear and higher-order risk propagation

- What: Deploy second-order (and higher) expansions using the third derivatives of the log-partition function for improved accuracy under larger shocks.

- Tools/Products:

- “Second-Order POT Risk” library for stress scenarios.

- Assumptions/Dependencies:

- Robust estimation of higher cumulants; numerical stability and runtime control.

- Finance (learning): Online SSR estimation and adaptive constraints

- What: Continuously learn SSR term structures from tick or end-of-day data; adapt SSR constraints in the entropic projection in real time.

- Tools/Products:

- “SSR Estimator” with Bayesian or regularized regression; feedback to calibration.

- Assumptions/Dependencies:

- Stationarity windows and regime detection; safeguards against overfitting/noise.

- Finance (execution): Real-time feedback loop between quoting, hedging, and calibration

- What: Integrate LR/DR risk with auto-hedgers and quoting engines so that calibration, risk, and hedge decisions co-evolve under a latency budget.

- Tools/Products:

- Event-driven “POT Orchestrator” coordinating calibration states and hedge orders.

- Assumptions/Dependencies:

- Low-latency data pipelines; robust exception handling when constraints become infeasible.

- Policy/Regulation: Standardized, model-independent cross-asset risk benchmarks

- What: Supervisory frameworks that specify entropic projection-based benchmarks for cross-asset sensitivities, distinct from any parametric model.

- Tools/Products:

- Regulatory technical standards for constraint diagnostics and influence-function disclosures.

- Assumptions/Dependencies:

- Industry consensus on discretization standards, SSR estimation protocols, and acceptable bases.

- Academia/Methods: Information geometry for robust model risk and sensitivity analysis

- What: Use Fisher geometry of entropic projections to diagnose model misspecification, quantify sensitivity directions with largest curvature, and guide grid design.

- Tools/Products:

- “Geometric Risk Analyzer” for curvature and influence heatmaps.

- Assumptions/Dependencies:

- Theoretical development of curvature-based bounds and their empirical validation.

- Software/ML: Constrained OT perturbation methods for other domains

- What: Apply POT-style LR to OT problems with domain-specific linear constraints (e.g., supply-chain flows, fair allocation), where sensitivities to marginal changes are needed.

- Tools/Products:

- Generic “Perturbed OT” libraries with plug-in constraints and LR solvers.

- Assumptions/Dependencies:

- Clear domain constraints and availability of a positive prior; acceptance of entropic regularization bias.

- Finance (XVA/Enterprise Risk): Integration into valuation adjustments and firm-wide stress testing

- What: Use LR-based cross-greeks to feed XVA engines and enterprise-wide scenario propagation, capturing impact of SPX vol shocks on VIX-linked exposures.

- Tools/Products:

- Interfaces connecting POT risk outputs to XVA/simulation layers.

- Assumptions/Dependencies:

- Data normalization across desks; alignment on grid/currency/discounting conventions omitted in the paper’s simplified exposition.

- Finance/Infrastructure: HPC-scale POT with dynamic grids and microstructure-aware filters

- What: Scale to large, adaptive grids and integrate microstructure filters (bid-ask, sparse strikes/tenors) while maintaining stability of Fisher inversions.

- Tools/Products:

- Distributed linear algebra for Hessian factorization; adaptive meshing.

- Assumptions/Dependencies:

- Careful regularization to stabilize inversions; robust gauge handling; monitoring of feasibility as constraints evolve.

- Education/Public literacy: Practitioner courses and toolkits for model-free cross-asset risk

- What: Develop continuing education modules and sandbox environments for traders/risk managers to learn model-free calibration and risk propagation.

- Tools/Products:

- Interactive labs demonstrating LR/DR/SSR effects on cross-greeks and hedging P&L.

- Assumptions/Dependencies:

- Curated historical datasets; simplified but faithful implementations for teaching.

Cross-cutting assumptions and dependencies (affecting most applications)

- Data quality: Clean, arbitrage-consistent SPX/VIX surfaces and VIX futures; treatment of known SPX–VIX basis.

- Feasibility: Existence of a coupling satisfying marginals and linear financial constraints; prior strictly positive on support.

- Numerical stability: Proper gauge fixing; well-conditioned Fisher matrix; robust Sinkhorn convergence.

- Validity domain: LR/DR accuracy holds primarily for small to moderate shocks; larger moves may need second-order expansions or partial recalibration.

- SSR dynamics: Empirical SSR estimates are stable across regimes or adaptively updated; SSR reflects local smile dynamics without introducing inconsistencies.

Glossary

- Bergomi model: A stochastic volatility framework where the forward variance curve drives volatility dynamics. "Traditional approaches to the joint SPXâVIX modeling problem rely on parametric stochastic volatility models such as the Heston model, stochastic volatility with jumps, Bergomi model, or rough volatility frameworks"

- Black's formula: A pricing formula for options on futures under lognormal assumptions, often used for VIX options. "In practice the latter is frequently handled using Black's formula applied directly to VIX futures"

- Black–Scholes: The classic option pricing model assuming lognormal asset dynamics and constant volatility. "Black-Scholes prices are smooth in ."

- Breeden–Litzenberger inversion: A method to recover the risk‑neutral density from the second derivative of call prices with respect to strike. "Using Breeden-Litzenberger inversion, the marginal density changes:"

- cumulant generating function: The logarithm of the moment generating function; for exponential families, it equals the log-partition function. "This function is the cumulant generating function of the exponential family defined by the Gibbs coupling."

- Dimensional Reduction (DR): A technique that reduces a higher-dimensional transport problem to a lower-dimensional one under conditional invariance, lowering computational cost. "Using SPX sensitivities generated by the dimension-reduced optimal transport method(DR), we construct dynamic hedges"

- dual potentials: The Lagrange multipliers in the dual of the entropic transport problem that parameterize the Gibbs coupling additively over coordinates. "The dual potentials are not uniquely determined."

- entropy regularization: Adding an entropy penalty to the transport objective to obtain smoother, computationally tractable solutions. "Entropy-regularized transport problems have become widely used in machine learning and computational optimal transport due to their favorable numerical properties"

- entropic martingale optimal transport: An entropy-regularized optimal transport approach constrained by martingality, used for joint SPX–VIX calibration. "While entropic martingale optimal transport provides an exact joint calibration of SPX and VIX smiles"

- entropic optimal transport: Optimal transport with an added entropy term, solvable efficiently via iterative scaling. "In this framework the calibrated coupling between equity levels and forward variance is obtained by solving a discrete entropic optimal transport problem using Sinkhorn iterations"

- entropic projection: The problem of finding the distribution closest in relative entropy to a prior, subject to linear constraints (e.g., marginals). "We consider the entropic projection problem:"

- exponential family: A class of probability distributions whose densities are proportional to the exponential of a linear combination of sufficient statistics. "Because the optimal coupling belongs to an exponential family, its response to marginal shocks can be characterized by the Fisher information matrix of the calibrated Gibbs distribution."

- Fisher information matrix: The Hessian of the log-partition function measuring local curvature of the statistical manifold; governs linear response sensitivities. "Because the optimal coupling belongs to an exponential family, its response to marginal shocks can be characterized by the Fisher information matrix of the calibrated Gibbs distribution."

- forward variance: The expected future variance over a horizon under the risk‑neutral measure. "VIX options are derivative contracts written on VIX, the square root of forward variance."

- forward variance identity: A relation linking SPX option prices to the VIX future via integrals over option payoffs. "In equity volatility markets the SPX and VIX option surfaces are linked through the forward variance identity"

- Gâteaux derivative: The directional derivative of a functional; here, the first‑order change in expectations under marginal perturbations. "Risk Representation: Gateaux Derivative Of Expectations"

- gauge fixing: Imposing normalization conditions on dual potentials to remove non-uniqueness due to additive constants. "To obtain a unique representation of the dual variables we fix the gauge"

- gauge invariance: The property that adding certain constants to dual potentials leaves the Gibbs coupling unchanged. "Gauge invariance."

- Gibbs distribution: A probability distribution of the exponential family form with a log-partition normalization, arising from entropic projection. "The resulting Gibbs distribution exactly reproduces the observed SPX and VIX option prices while remaining free of parametric volatility assumptions."

- Heston model: A stochastic volatility model where variance follows a mean-reverting square‑root (CIR) process. "Traditional approaches to the joint SPXâVIX modeling problem rely on parametric stochastic volatility models such as the Heston model"

- implicit function theorem: A result guaranteeing differentiability of solution mappings under suitable conditions; used to show smooth dependence of dual potentials on perturbations. "Using the implicit function theorem applied to the dual formulation, we show that the calibrated Gibbs coupling depends smoothly on admissible market perturbations."

- information geometry: The differential‑geometric study of statistical manifolds equipped with the Fisher metric. "The perturbation theory derived above admits a natural interpretation in terms of information geometry."

- influence function: A vector that maps marginal perturbations to first‑order changes in a functional (price) via inner products. "The vector is the influence function of the payoff "

- KKT conditions: The Karush–Kuhn–Tucker optimality conditions characterizing solutions to constrained optimization problems. "differentiate the dual KKT condition"

- Linear Response (LR): A first‑order system describing how calibrated couplings and prices react to small perturbations through the Fisher information. "the local geometry of the calibrated coupling via a Linear Response (LR) system"

- log-contract: A derivative with payoff proportional to the negative logarithm of the asset return, whose fair strike equals expected variance under certain conditions. "The VIX index must represent the fair strike of a log-contract on :"

- log-partition function: The logarithm of the normalization constant of an exponential family; its gradient and Hessian yield moments and Fisher information. "For dual potentials define the log-partition function"

- martingale: A stochastic process whose conditional expectation equals its current value, reflecting no‑arbitrage in discounted asset prices. "Under the risk-neutral measure, the discounted asset price must be a martingale."

- Martingale Optimal Transport (MOT): Optimal transport with the additional constraint that the coupling yields a martingale; used for model‑free pricing. "who formulated the joint SPXâVIX calibration problem as a martingale optimal transport (MOT) problem."

- martingality condition: The enforcement that the conditional expectation of future spot equals current spot under the calibrated measure. "Martingality condition"

- Open Mapping Theorem: A functional analysis theorem ensuring linear surjections map open sets to open sets; used to show feasibility under small perturbations. "By the Open Mapping Theorem, for a sufficiently small neighborhood of , contains a neighborhood of ."

- Perturbed Optimal Transport (POT): The paper’s framework that leverages entropic OT and perturbation theory to generate risks without full recalibration. "we term Perturbed Optimal Transport(POT)"

- primal–dual equivalence: The equality of optimal values between a convex optimization problem and its dual, ensuring strong duality. "PrimalâDual Equivalence"

- probability simplex: The set of all nonnegative vectors that sum to one, representing discrete probability distributions. "where denotes the probability simplex."

- relative entropy: Also known as Kullback–Leibler divergence; a measure of discrepancy between two probability distributions. "where relative entropy is"

- Riemannian metric: An inner product on the tangent space of a manifold; the Fisher information induces such a metric on statistical models. "therefore corresponds to a natural Riemannian metric induced by the Fisher information."

- rough volatility: A class of models where volatility paths are rough (e.g., driven by fractional Brownian motion), capturing short‑term irregularity. "rough volatility frameworks"

- Sinkhorn iterations: An iterative matrix scaling algorithm used to solve entropy‑regularized transport problems efficiently. "solved efficiently using Sinkhorn iterations."

- Skew Stickiness Ratio (SSR): A dimensionless parameter quantifying how the implied volatility smile shifts with respect to changes in the forward. "Skew Stickiness Ratio (SSR) dynamics for the VIX volatility surface"

- SPX: The S&P 500 index (or its options); SPX options provide the equity smile used in joint calibration with VIX. "SPX options encode the distribution of future equity prices"

- stochastic local volatility: Models combining local volatility (state‑dependent) with stochastic factors to capture smile dynamics. "parametric stochastic volatility and stochastic local volatility models"

- stochastic volatility: Models where volatility itself follows a random process, often used to match implied volatility smiles. "stochastic volatility frameworks such as the Heston model"

- variance consistency: The constraint that ties the VIX level to the expected log‑contract payoff, ensuring forward‑variance coherence. "Variance Consistency: The VIX index must represent the fair strike of a log-contract on :"

- VIX: The volatility index equal to the square root of risk‑neutral expected variance; underlies VIX futures and options. "VIX options are derivative contracts written on VIX, the square root of forward variance."

Collections

Sign up for free to add this paper to one or more collections.