- The paper’s main contribution is introducing the b-value to quantify the bias threshold at which combined estimators lose statistical significance.

- It develops a framework using precision-weighted, pretest, and soft-thresholding estimators to construct confidence intervals that adjust for unknown bias.

- The methodology enables robust sensitivity analysis and efficient empirical applications, such as reconciling OLS and IV estimates in returns to schooling.

Combining Unbiased and Biased Estimators: Theoretical Foundation and Inference Robustness via the b-Value

Introduction and Motivation

The central statistical problem addressed is the combination of unbiased but less precise estimators with biased but more precise ones, especially for improved inference in applied research where biases are unknown and potentially non-negligible. Classical point estimation under such circumstances is well-studied, but robustly valid and interpretable statistical inference has seen substantially less attention due to challenges in characterizing the resulting distributions when the magnitude of the bias is unknown.

This paper introduces an inferential framework that systematizes sensitivity to possible bias using a family of confidence intervals indexed by an upper bound on the relative bias. The pivotal construct is the b-value, representing the critical threshold of (relative) bias at which the combined estimator ceases to yield a statistically significant inference. This concept unifies ideas from classical sensitivity analysis with recent advances in estimator combination and robust inference.

Problem Setup and Inference Framework

The canonical setup involves two estimators for a scalar parameter τ: an unbiased estimator, τ^0∼N(τ,σ02), and a biased estimator, τ^1∼N(τ+Δ,σ12), with Δ and both variances σ02,σ12 generally unknown. Certain works further generalize this to correlated estimators, vector-valued parameters, and integration of multiple biased estimators. The analysis primarily exploits the joint (possibly asymptotic) normality of the estimators under Le Cam or local asymptotic normality frameworks—rendering the following developments broadly applicable.

The core inferential object is a sequence of confidence intervals for τ, parameterized by an assumed upper bound b on the maximum relative bias, i.e., ∣Δ∣/σ0≤b. For a given estimator τ^ (e.g., via a combination rule), a confidence interval can be constructed that ensures

∣Δ∣/σ0≤binfPΔ(∣τ^−τ∣≤c(b))≥1−ζ.

The width of the interval and its center can be specialized according to the combination rule (precision weighting, pretest, soft-thresholding). Notably, monotonicity is imposed: increasing b yields wider intervals, encapsulating greater uncertainty as larger biases are considered.

The b-value (b∗) is formally defined as the smallest b for which the confidence interval includes the null value (for hypothesis testing), i.e., 0∈[τ^−c(b∗),τ^+c(b∗)]. Thus, b∗ quantifies the inferential robustness of conclusions to potential bias magnitude.

Canonical Estimators and Their Inferential Properties

Three estimator types are systematically analyzed:

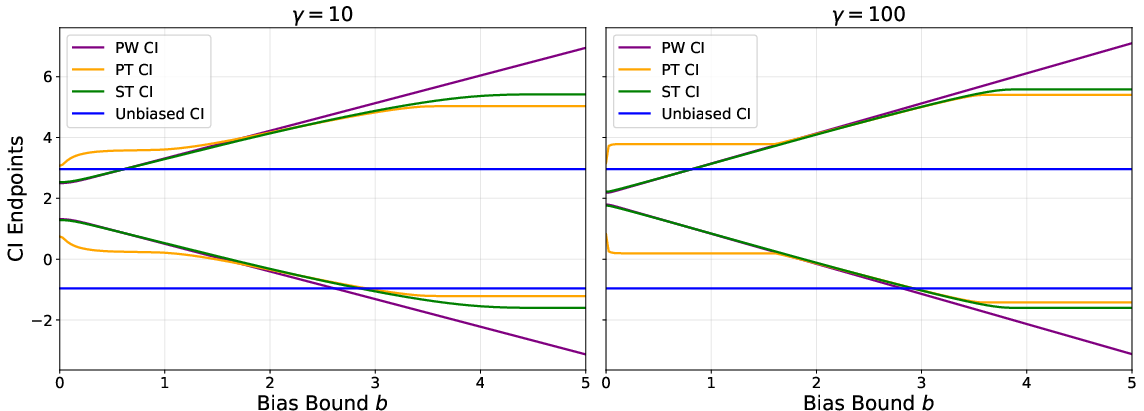

1. Precision-Weighted Estimator (PW): This convexly combines the two estimators based on their variances; while minimax optimal if Δ=0, its risk can diverge rapidly with increasing ∣Δ∣. The derived confidence interval is minimal when b=0 but expands rapidly as b grows.

2. Pretest Estimator (PT): This estimator employs a preliminary test of equality between estimators (or equivalently, of bias). If evidence against bias is weak, a weighted estimator is used; otherwise, the unbiased estimator prevails. The confidence interval here is constructed using a non-trivial mixture distribution reflecting a combination of these two regimes.

3. Soft-Thresholding Estimator (ST): By replacing the discontinuous hard threshold of PT with a continuous transition, the ST estimator ensures regular risk behavior across the spectrum of possible biases. Both point risk and coverage probability exhibit a monotonic dependency on ∣Δ∣, ensuring statistical control and computational tractability for constructing coverage intervals.

Efficiency and Robustness: Among these, the ST estimator is shown to combine the inferential efficiency of PW in the low-bias regime with the robustness of PT's fallback behavior in the presence of significant bias. Furthermore, the monotonic functional dependence of coverage on ∣Δ∣ for ST expedites optimal interval construction for prescribed coverage levels.

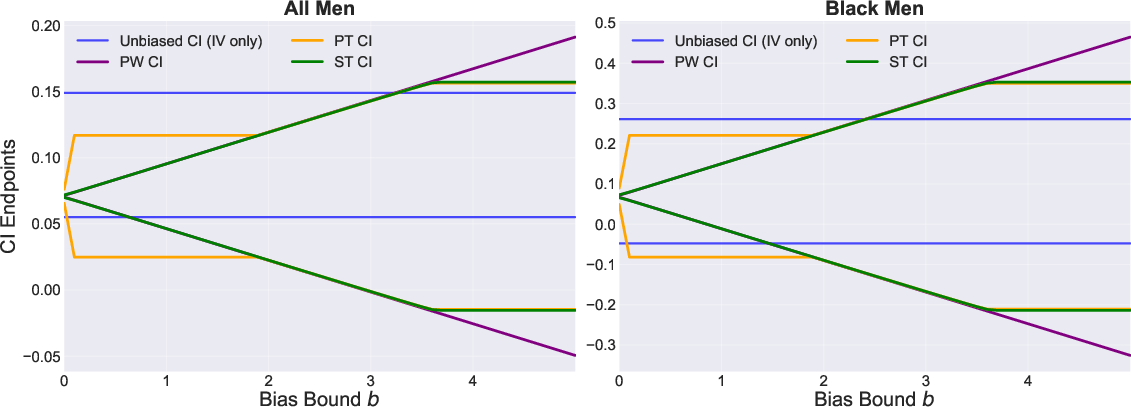

Figure 1: Confidence intervals as a function of maximum relative bias ∣Δ/σ0∣≤b for precision-weighted, pretest, soft-thresholding, and unbiased estimators.

The b-Value and Sensitivity Analysis

The critical methodological innovation is the operationalization of b-value as a robustness threshold. For hypothesis testing (e.g., H0:τ=0), one examines how the sequence of intervals intersects the null. The b-value is explicitly computable for all three estimator types; for ST, its unique monotonicity ensures optimal computational efficiency.

This paradigm generalizes and extends classical sensitivity analysis (e.g., Rosenbaum's design sensitivity, the E-value in causal inference) in a model-based setting, integrating both analytical tractability and clear interpretability of robustness to unmeasured confounding or other sources of bias.

Numerical Implementation: Root-finding methods (e.g., bisection) efficiently yield the b-value for each estimator. For the ST estimator, since coverage is minimized at the maximal allowed ∣Δ∣, a one-dimensional search suffices.

Generalizations: Multivariate and Multiple Estimators

The framework admits direct extension:

- Multivariate Parameters: For vector-valued τ, the bias constraint becomes an axis-aligned hyperrectangle in bias space. The coverage criterion is extended to ellipsoidal regions, with the b-value becoming a (d−1)-dimensional surface in bias space. The maximization for worst-case bias is achieved at hyperrectangle vertices.

- Multiple Biased Estimators: Combining more than two estimators, each with its own bias and variance, is treated via componentwise thresholding and appropriate generalizations of the previous interval constructions.

Application: Empirical Demonstration

An empirical illustration combines OLS and IV estimators of returns to schooling [angrist1991does]. The OLS estimator is highly precise but potentially biased due to endogeneity, whereas IV is unbiased but with large variance. Application of the robust confidence interval framework:

Implications and Future Directions

This paper's formalization of estimator robustness systematically enriches both methodological and substantive research where estimator bias is plausible but unidentifiable. Analysts gain both inferential efficiency and explicit quantification of sensitivity via the b-value, aligning with ongoing trends towards transparent, assumption-graded analysis.

Key future avenues include:

- Deciding optimal bias-scaling matrices in the multivariate case.

- Developing adaptive combination rules exploiting external information on plausible bias.

- Extending the framework to high-dimensional settings and non-Gaussian noise models.

Overall, this framework will play a foundational role in credible, efficient, and transparent statistical practice in the presence of estimator bias.

Conclusion

By introducing the b-value and associated sensitivity-parameterized confidence interval sequences, the paper offers a theoretically grounded and practically implementable methodology for combining unbiased and biased estimators in inference tasks. The explicit characterization of robustness to bias, especially via the soft-thresholding estimator, advances both the theory and implementation of combining heterogeneous evidence sources. This work broadens the inferential toolkit for robust data integration, causal inference, and evidence synthesis, and sets the stage for further development in bias-aware methodology.

References

- "Introducing the b-value: combining unbiased and biased estimators from a sensitivity analysis perspective" (2602.16310)

- Angrist, J. D., & Krueger, A. B. (1991). Does Compulsory School Attendance Affect Schooling and Earnings? [angrist1991does]

- Additional referents as cited in the original article.