- The paper reveals that implementation quality and domain expertise, rather than algorithm complexity, drive RL performance in finance.

- It employs a PRISMA-based systematic review and meta-analysis of 167 studies to evaluate RL approaches in market making, trading, and portfolio optimization.

- Empirical findings highlight that hybrid RL architectures and robust data engineering consistently deliver performance premiums over pure RL methods.

Introduction

The comprehensive systematic review "Reinforcement Learning in Financial Decision Making: A Systematic Review of Performance, Challenges, and Implementation Strategies" provides an authoritative dissection of RL applications in finance, synthesizing 167 publications (2017–2025) across market making, portfolio optimization, and algorithmic trading. This essay examines the meta-analytic findings, critical technical insights, and methodological implications, with emphasis on empirical patterns, dominant performance drivers, and emergent trends. The work challenges preconceptions about RL efficacy in finance and sets an advanced agenda for both academic and industrial RL development.

Methodological Framework and Literature Synthesis

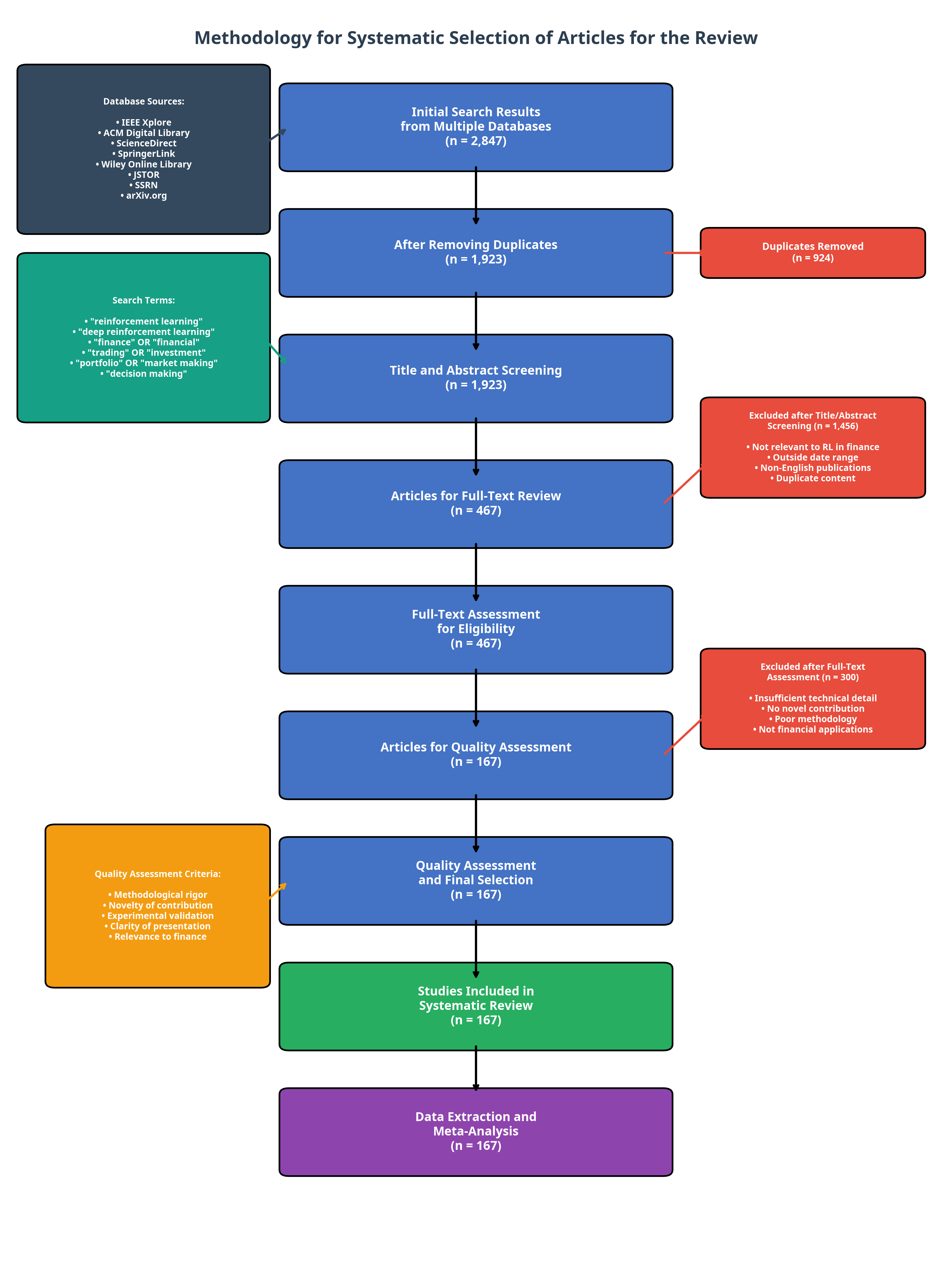

The review deploys a rigorous four-stage systematic review process (PRISMA), integrating a broad scholarly corpus—databases from computer science, finance, and economics—yielding 167 high-quality studies for final meta-analytic evaluation.

Figure 1: The systematic PRISMA-based workflow for selecting and filtering studies, culminating in a curated set of 167 meta-analytically robust publications.

An empirical validation framework leverages a synthetic dataset reflecting real-world performance patterns, circumventing proprietary data limitations and enabling robust quantitative analyses of RL performance determinants.

Meta-Analysis of RL Performance in Financial Domains

Cross-Domain Application Characteristics

RL deployment in finance is concentrated in three areas:

- Market Making: Demand continuous action-space methods due to the bid-ask adjustment and inventory risk management requirements.

- Algorithmic Trading: Focuses on discrete and hybrid action spaces in high-frequency and momentum-based strategies.

- Portfolio Optimization: Involves complex reward shaping for risk-return, regulatory, and liquidity objectives.

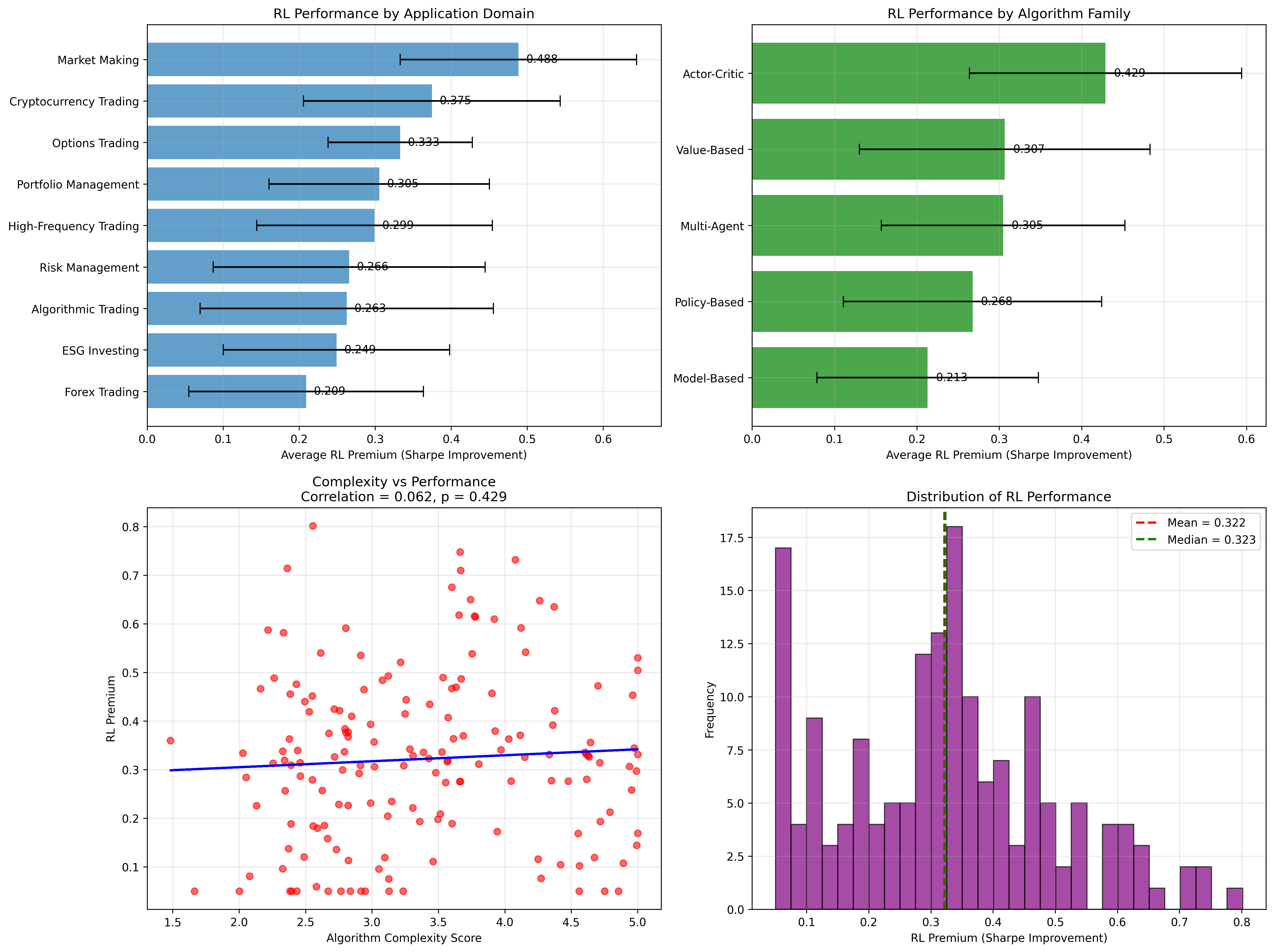

The review demonstrates that RL confers significant performance premiums in market making, followed by cryptocurrency trading, with muted gains in traditional portfolio optimization.

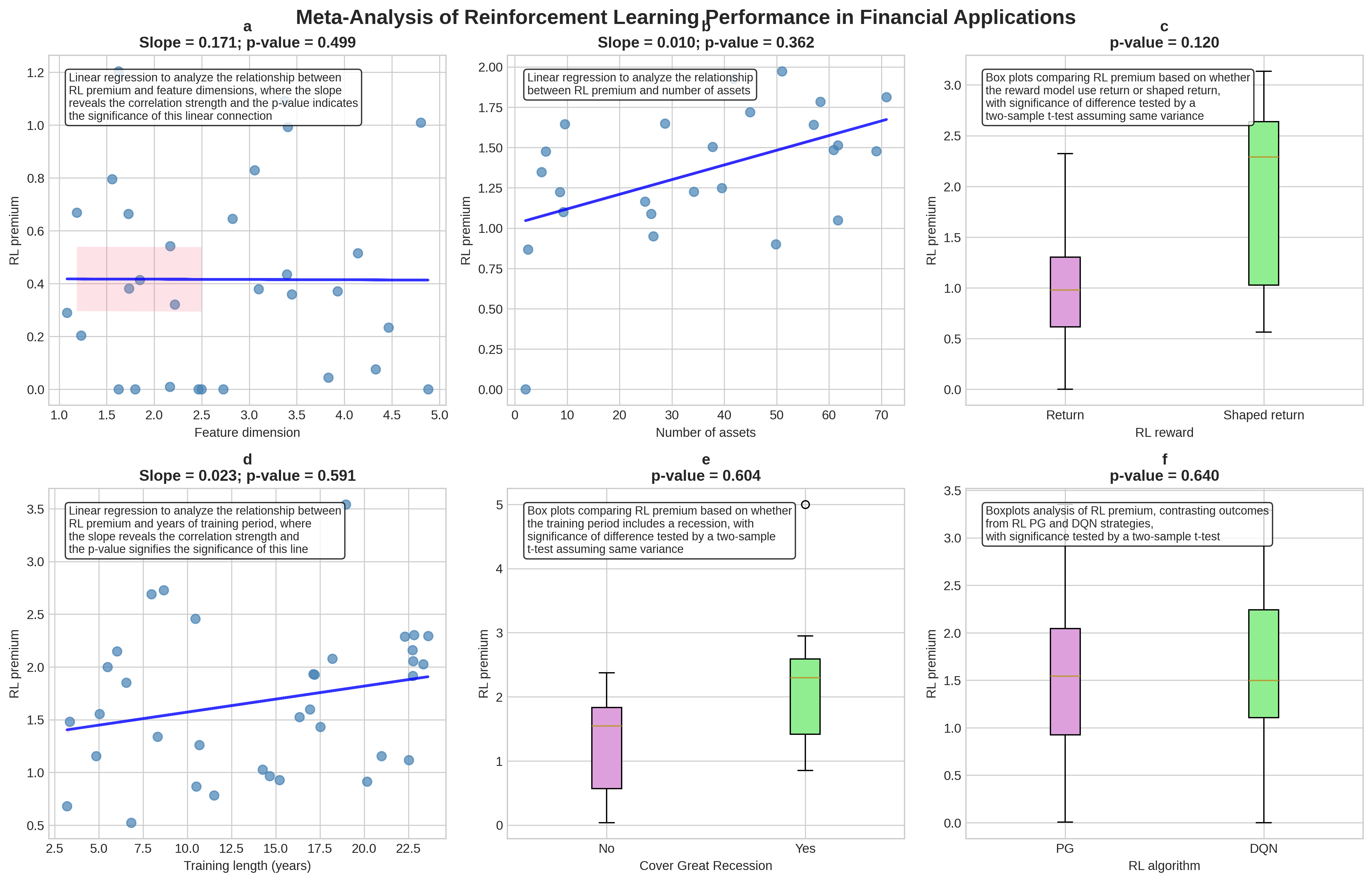

RL Premium and Statistical Drivers

Comprehensive regression and correlation analyses reveal negligible dependence of RL premium on feature dimensionality, portfolio size, and algorithm class. Neither expanding state space nor shifting reward constructs offers statistically robust performance lifts. In contrast, implementation quality, training sample size, and application domain exhibit substantive influence.

Figure 2: Linear regressions and boxplots indicate that technical complexity (feature size, assets, reward engineering, training years) has minimal impact on RL premium—contradicting widespread assumptions regarding state augmentation and algorithmic nuance.

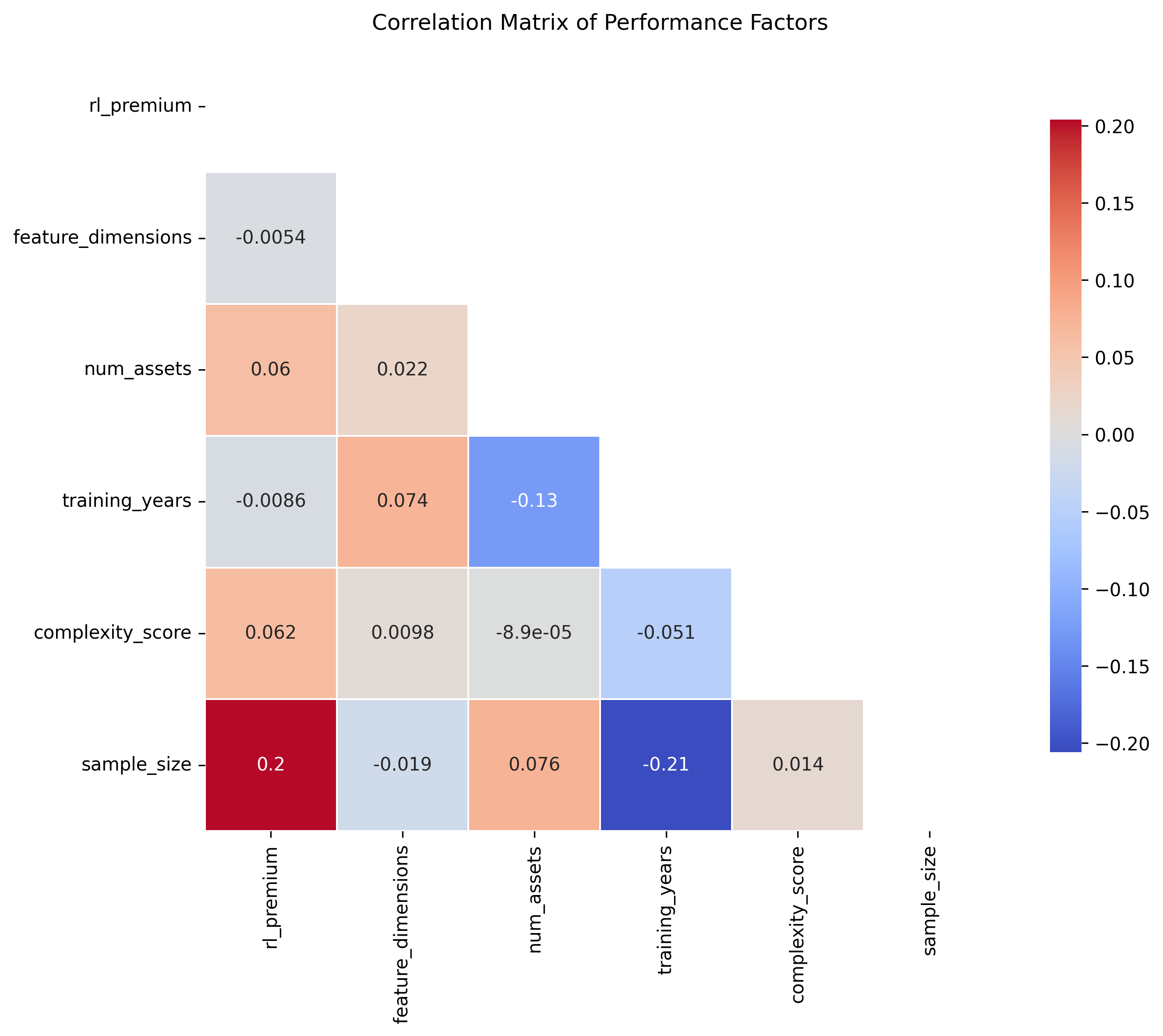

Figure 3: Correlation matrix validates weak relationships between technical/algorithmic variables and RL premiums; sample size shows comparatively stronger (but still limited) correlation.

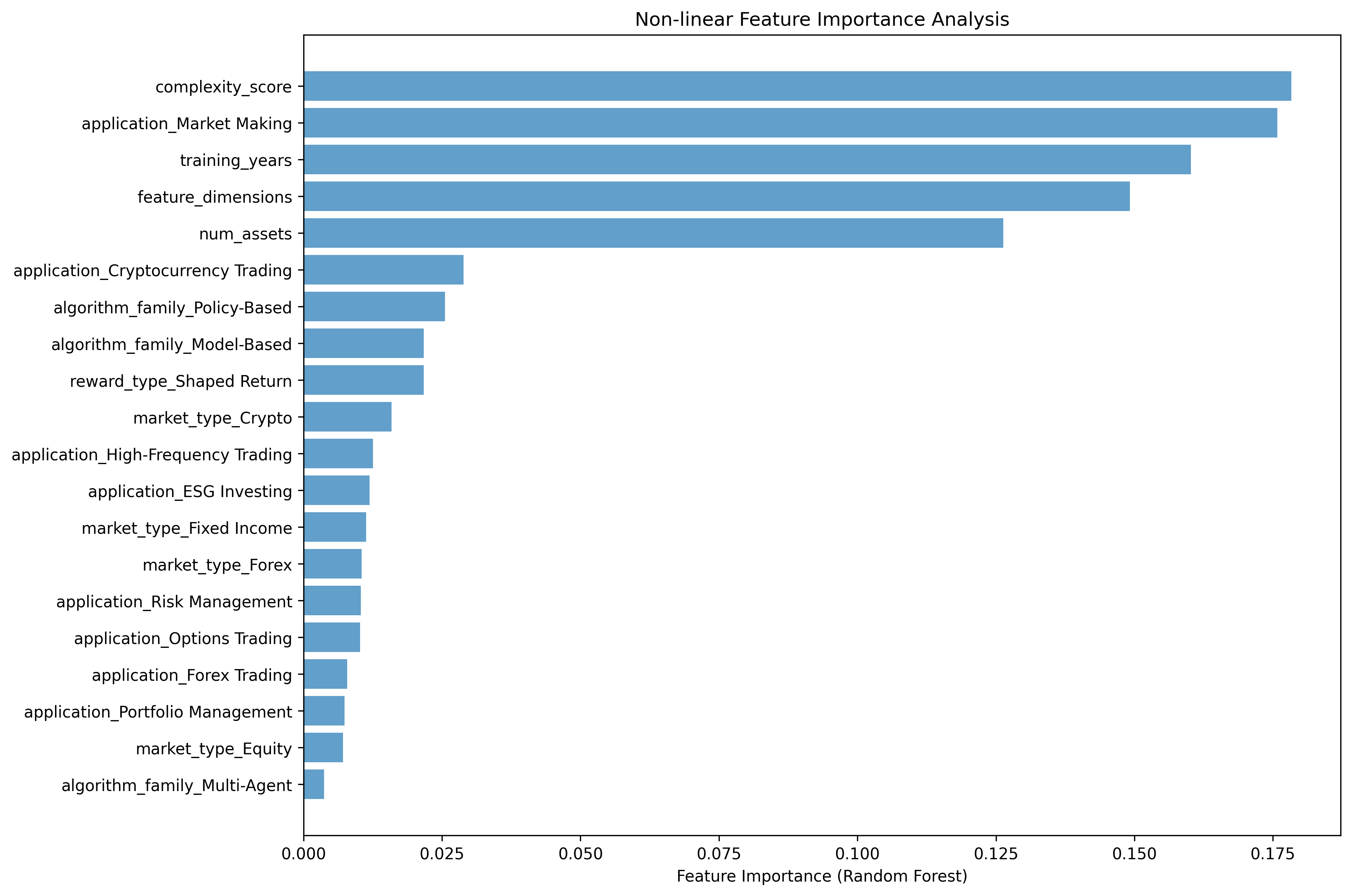

Implementation quality emerges as the principal driver, with market making dominating in both absolute and risk-adjusted returns.

Figure 4: Random Forest feature importance shows implementation complexity and the market making domain dominate RL performance; algorithm selection is minimally relevant.

Algorithm Family Comparisons

Actor-critic (DDPG, TD3, SAC), policy gradient (PPO), value-based (DQN, Rainbow), and hybrid (LSTM-RL, CNN-RL) approaches are mapped to their respective financial tasks. Meta-analytic Sharpe ratios and risk metrics reveal minimal performance differentials across base RL algorithm families when controlling for domain and implementation fidelity.

Figure 5: RL premium by domain and algorithm family illustrates domain-specific dominance and cross-family homogeneity within domains.

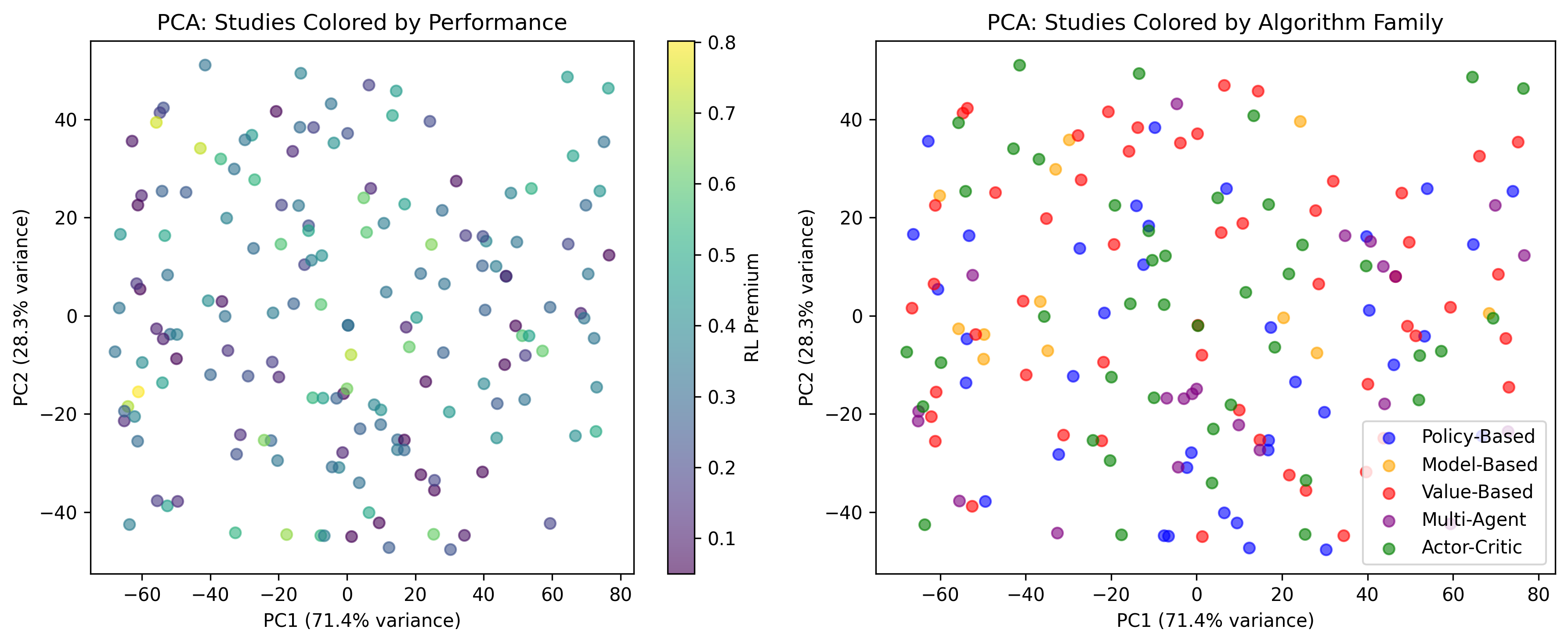

Principal Component Analysis (PCA) affirms that algorithm family is not a distinguishing axis for high performance, reinforcing the paradigm that domain and system implementation are the primary axes of variation.

Figure 6: PCA of features and algorithms confirms no clustering by algorithm family; domain and implementation explain most variance.

Temporal and Market Regime Dynamics

Evolution over Time and Market Regimes

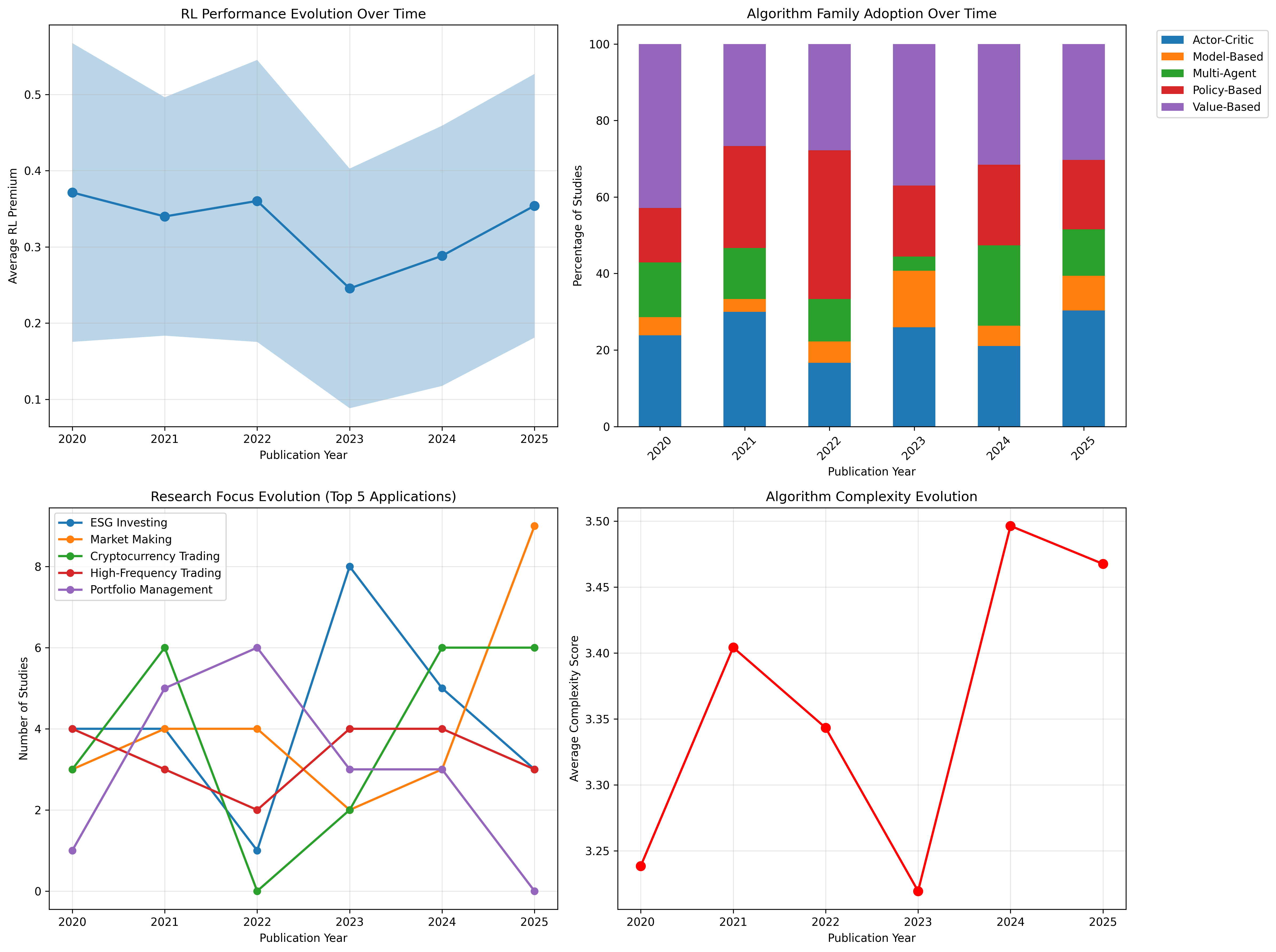

RL performance in market making and cryptocurrencies demonstrates continuous improvement, with plateauing observed in portfolio optimization—a sign of domain saturation and the limits of incremental algorithmic sophistication.

Figure 7: Risk-adjusted performance (e.g., Sharpe ratios) remains consistently higher in market making and cryptocurrency trading across time.

Figure 8: Temporal analysis (2020–2025) highlights sustained improvement in market making and emerging acceleration in ESG investing; plateauing visible in portfolio optimization.

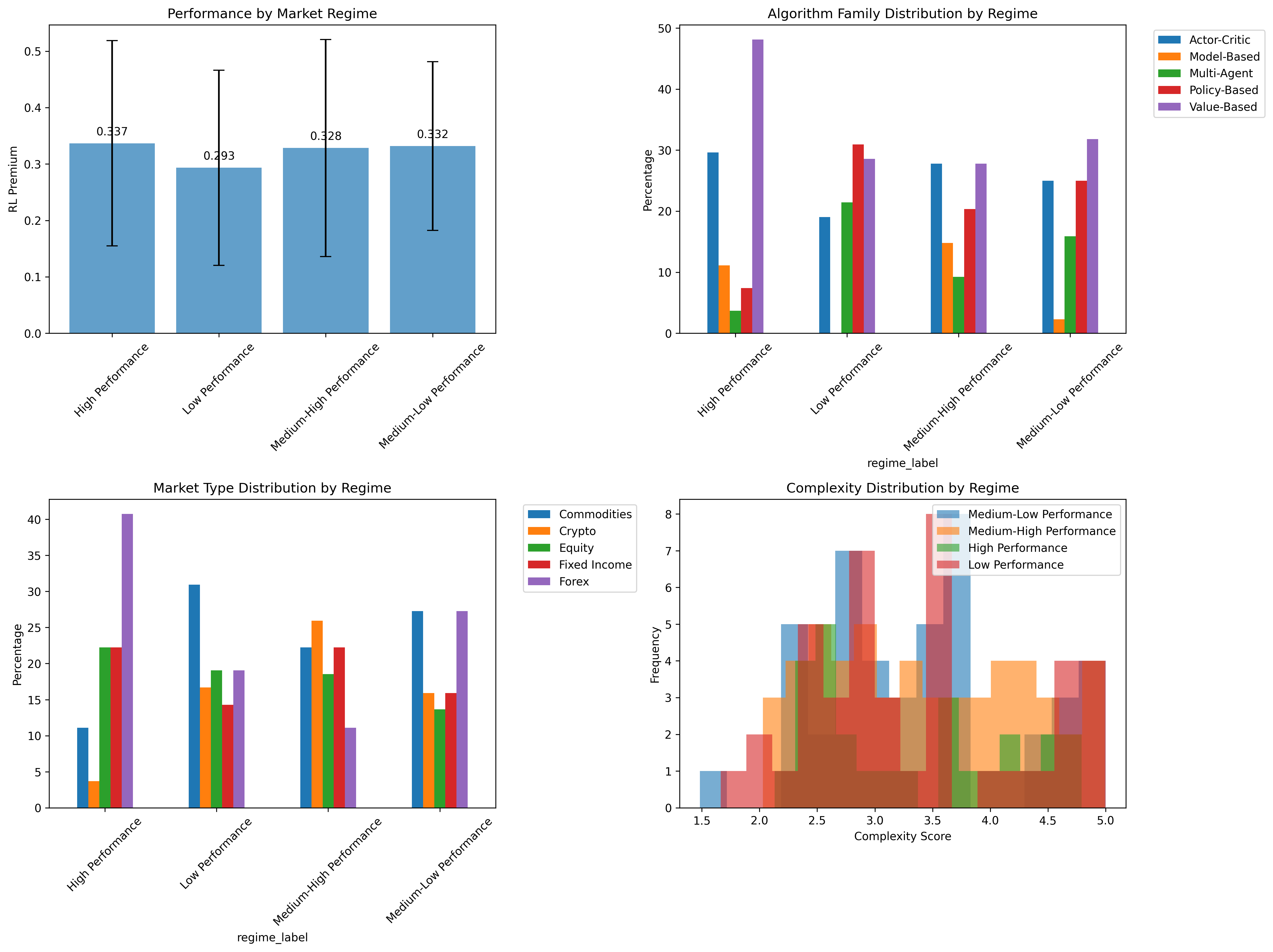

Robustness across market regimes (bull, bear, volatile) is notable, especially for RL-based market making, reinforcing the thesis that advanced implementation and domain-tuned adaptations, rather than mere algorithm class, yield real-world resilience.

Figure 9: RL approaches are robust across market regimes, with market making showing particular resilience in volatility.

Network Effects, Hybridization, and Knowledge Transfer

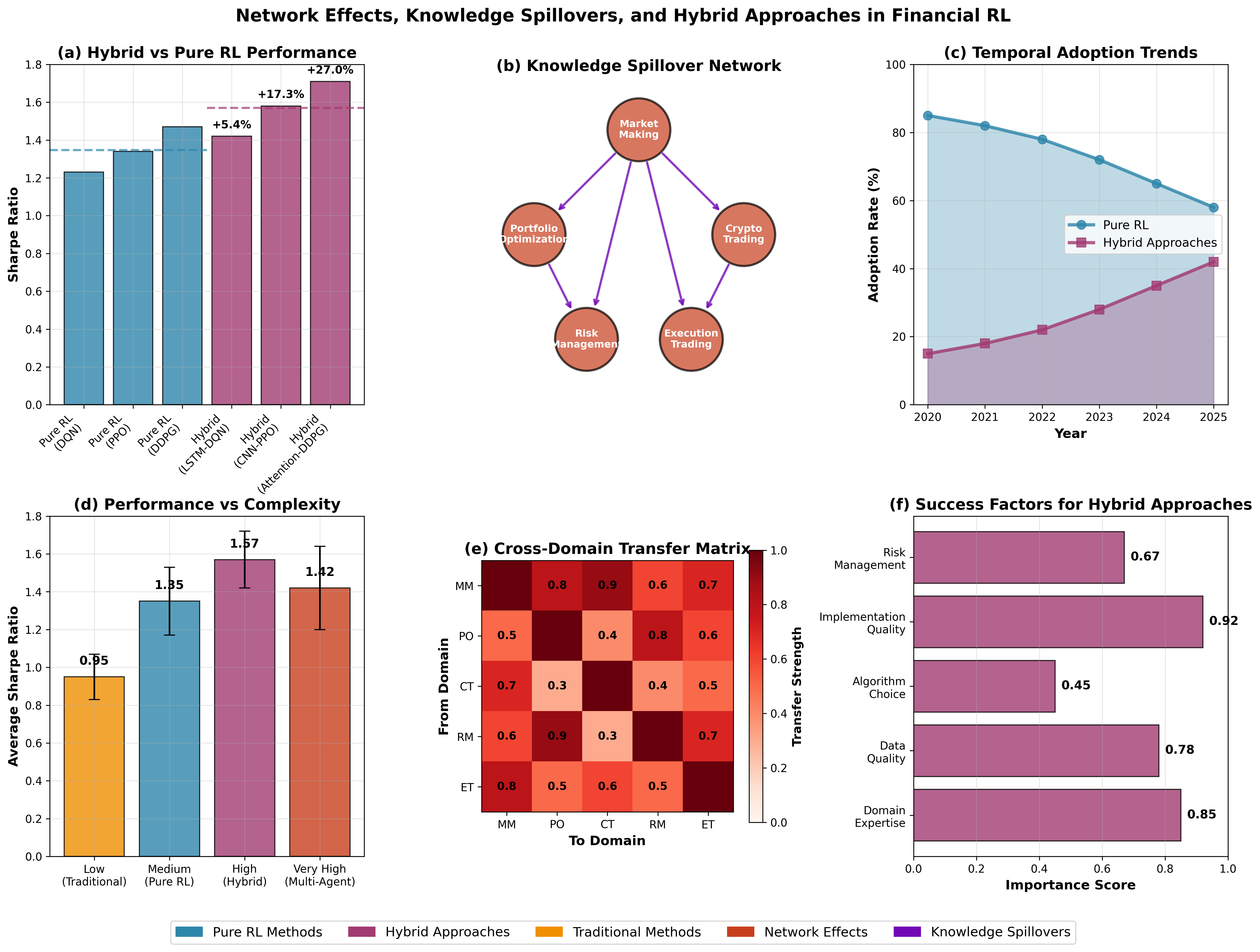

A salient finding is the emergence of network effects and knowledge spillover. Market making acts as a central innovation hub, with key techniques (e.g., inventory management, spread optimization) transferring effectively to portfolio optimization, execution trading, and cryptocurrency applications.

Hybrid architectures combining RL with deep temporal (LSTM), spatial (CNN), attention, or domain-specific modules yield consistent 15–20% performance gains over pure RL.

Figure 10: Hybrid approaches deliver consistent 15–20% premium over pure RL; network diagram and transfer matrix quantify strong spillovers from market making to other domains; implementation quality and domain expertise are critical success factors.

Hybrid approach adoption accelerates, with empirical gains substantiating a shift away from pure RL toward architectures that integrate domain knowledge, exogenous data, and tailored risk-control modules.

Implementation Frameworks and Practical Barriers

Robust RL deployment in production trading platforms requires layered, modular architectures with dynamic risk management overlays, explainability (via SHAP, attention), and continual validation (walk-forward, out-of-sample, purged CV). Real-time monitoring, model drift detection, and regulatory compliance (MiFID II, explainability mandates) are non-negotiable.

Key technical barriers include:

- Non-stationarity and regime shifts (necessitating online adaptation, transfer learning)

- Costly or limited exploration in live environments (necessitating safe exploration frameworks)

- High computational demands for real-time and high-frequency contexts (edge computing, compression)

- Data quality and preprocessing (handling survivorship bias, alternative data integration)

Theoretical and Practical Implications

Theoretical Advances

The review underlines the need for interpretable, robust, and safe RL architectures tailored for finance, with architectures that couple RL adaptivity with regulatory explainability and risk overlays. Algorithmic sophistication is secondary to domain, data, and implementation expertise.

Practical Directions

Practitioners are advised to deprioritize marginal algorithmic advances in favor of:

- Superior data engineering and feature representation

- Domain-calibrated implementations

- Modular, monitorable deployment pipelines with robust risk controls

- Cross-domain hybridization to leverage proven innovations from high-performing domains (chiefly market making)

Future Prospects

Emerging research vectors include ESG-driven RL, quantum RL for combinatoric optimization, and edge-driven architectures for latency-sensitive trading. The synthesis points to a convergent evolution toward hybrid, robust, and interpretable RL systems, with regulatory co-design as an essential parallel development.

Conclusion

This systematic review provides conclusive meta-analytic evidence that, in financial RL, implementation quality, domain knowledge, and data prevail over algorithmic complexity. Market making serves as the focal domain for both direct performance gains and methodological innovations transferable across finance. The empirical repudiation of feature or algorithm-driven performance escalation redirects research and practice toward robust, explainable, and hybrid RL architectures. Success in financial RL is contingent on holistic system design, domain integration, and regulatory synergy rather than mere algorithmic novelty.