- The paper introduces a robust TOT framework that reduces predictive risk by integrating latent variables and providing theoretical guarantees.

- The paper details exact identifiability conditions using only four adjacent observations, ensuring reliable recovery of hidden dynamics.

- The paper offers a model-agnostic blueprint validated on synthetic and real-world datasets, enhancing forecasting accuracy over traditional methods.

Online Time Series Forecasting with Theoretical Guarantees

This essay provides an expert summary of the research paper "Online Time Series Forecasting with Theoretical Guarantees" (2510.18281). The paper introduces a robust framework designed to address the challenges of online time series forecasting amidst nonstationary environments caused by latent variable distribution shifts.

Introduction to the Framework

The paper proposes the Theoretical framework for Online Time-series forecasting (TOT), which incorporates theoretical guarantees to improve forecasting accuracy in the presence of temporal distribution shifts driven by latent variables. The framework is designed to enhance traditional forecasting models by integrating latent variables that influence the observed data.

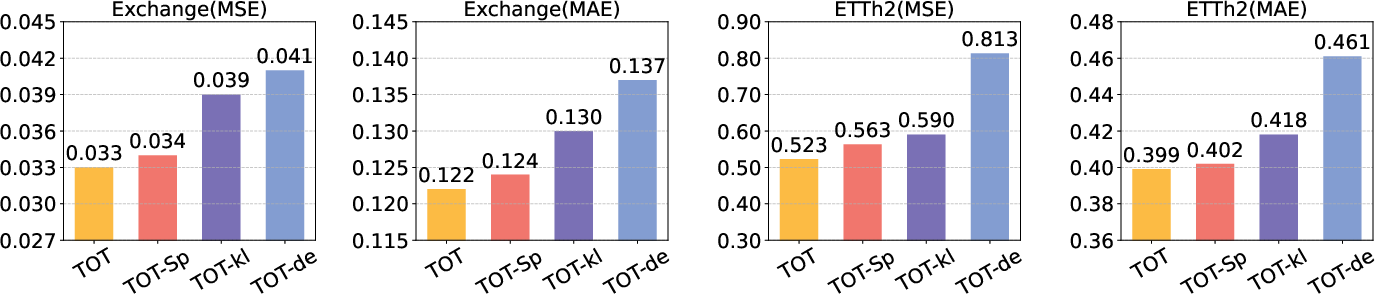

Figure 1: Ablation study on the Exchange and ETTh2 datasets.

Theoretical Contributions

Predictive-Risk Analysis

The core contribution is the theoretical demonstration that integrating latent variables into forecasting models reduces the predictive risk. Specifically, the approach provides a risk-bound guarantee, proving that conditioning on latent variables yields a systematic reduction in forecasting errors. The reduction is persistently effective under estimation noise and improves with greater identifiability precision of the latent variables.

Identifiability of Latent Variables

Another critical aspect is the identifiability of both latent variables and their causal dynamics using only four adjacent observations. The paper provides a formal derivation of these conditions, ensuring that the introduced latent variables are uniquely recoverable, which is vital for maintaining the consistency and reliability of the forecast.

Block-wise and Component-wise Identification

The authors establish a block-wise identifiability framework to manage the joint distribution of latent and observed variables, which is crucial for consistent performance in practice. Extended to component-wise identification, the framework facilitates a more granular understanding and control of individual latent variables, paving the way for more tailored interventions in time series forecasting.

Practical Implementation

Model-Agnostic Blueprint

The research introduces a modular, plug-and-play model-agnostic blueprint for incorporating latent variables into various backbone models. This architecture employs a temporal decoder coupled with two independent noise estimators to accurately model observed and latent variable dynamics. This configuration is highly adaptable and can be integrated with existing neural architectures like LSTMs and Transformers.

Experiments and Results

The paper showcases extensive empirical validation on synthetic and real-world datasets to support the theoretical claims. The framework is implemented on baseline models to demonstrate significant improvements in accuracy over traditional methods, thereby highlighting its practical utility in diverse applications.

Conclusion

The introduction of the TOT framework marks a significant advancement in online time series forecasting by addressing the pervasive issue of distribution shifts through theoretical underpinnings and practical solutions. By securing latent variable identifiability, the framework ensures robust, accurate forecasting, which is crucial for applications demanding real-time data adaptability.

The paper concludes with future directions, hinting at potential extensions to related tasks, such as causal discovery in time series data and nonstationary video understanding. The limitations indicate an opportunity for further research in handling continuous or multi-rate sampling time series data, suggesting it as a meaningful direction for future exploration.