- The paper shows that upper censorship consistently outperforms full disclosure in maximizing collusive profits across different discount factor regimes.

- Simulation results reveal a non-monotonic profit reversal between no disclosure and full disclosure, contradicting traditional equilibrium predictions.

- The study integrates Q-learning algorithm dynamics with information design theory, highlighting the need for simulation-based evaluations in AI-mediated markets.

Context and Motivation

The growing adoption of AI-powered pricing algorithms in regulated industries has amplified concerns about algorithmic collusion and the potential for supracompetitive outcomes even without explicit communication between firms. Amid these concerns, this paper analyzes how third-party information disclosure—specifically, the design of signals observed by Q-learning pricing algorithms—affects pricing dynamics and collusive outcomes under stochastic demand. The study is motivated by real-world instances where intermediaries such as RealPage provide market signals to algorithmic pricing agents, influencing strategic interaction and market outcomes.

Theoretical Framework and Disclosure Rules

The model features two symmetric Q-learning agents repeatedly setting prices in a Bertrand competition with stochastic binary demand (θL, θH). Agents do not observe demand shocks directly, but a third party observes and discloses information according to a fixed rule:

- No Disclosure: No information about the demand state is sent.

- Full Disclosure: The true demand state is revealed.

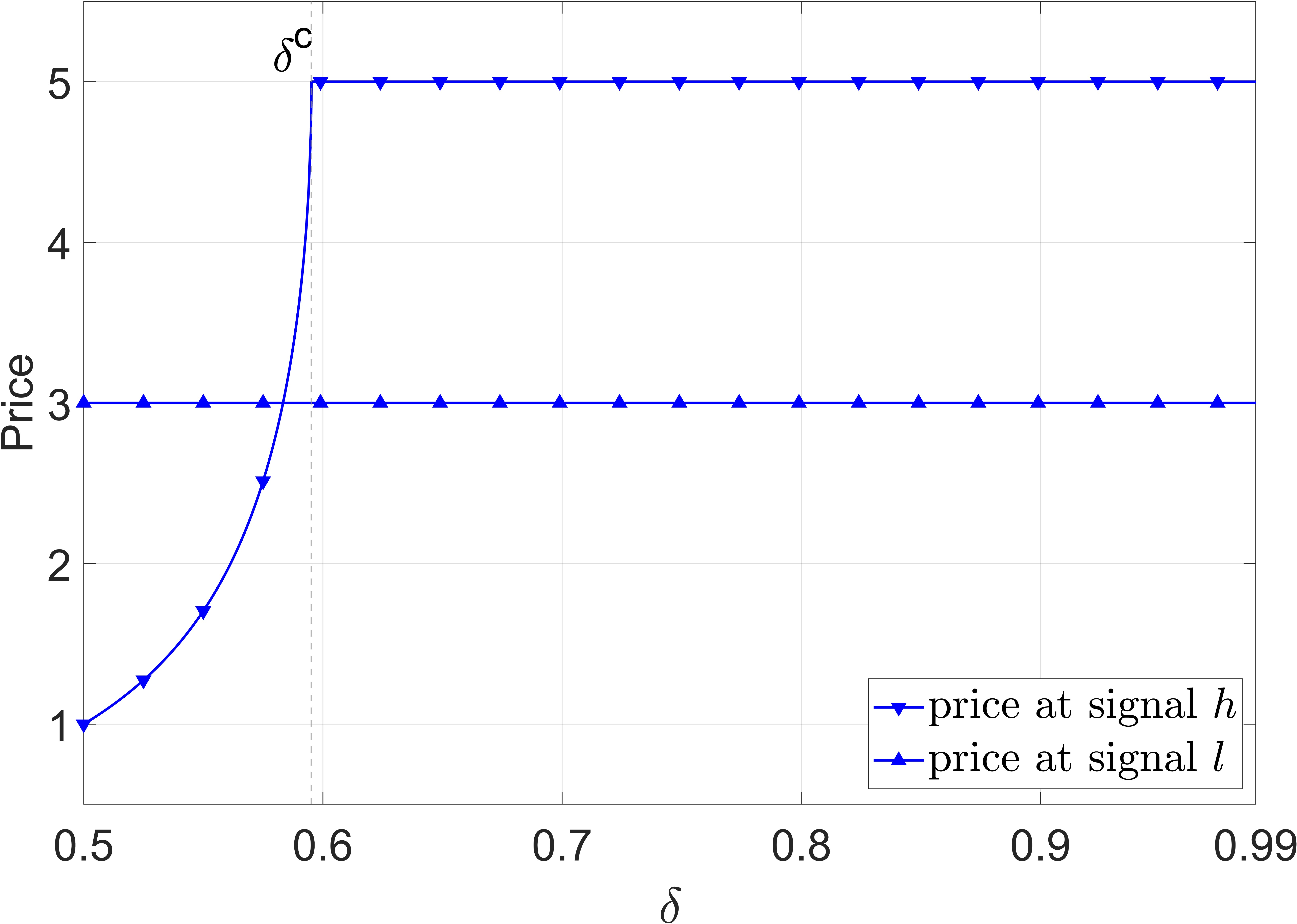

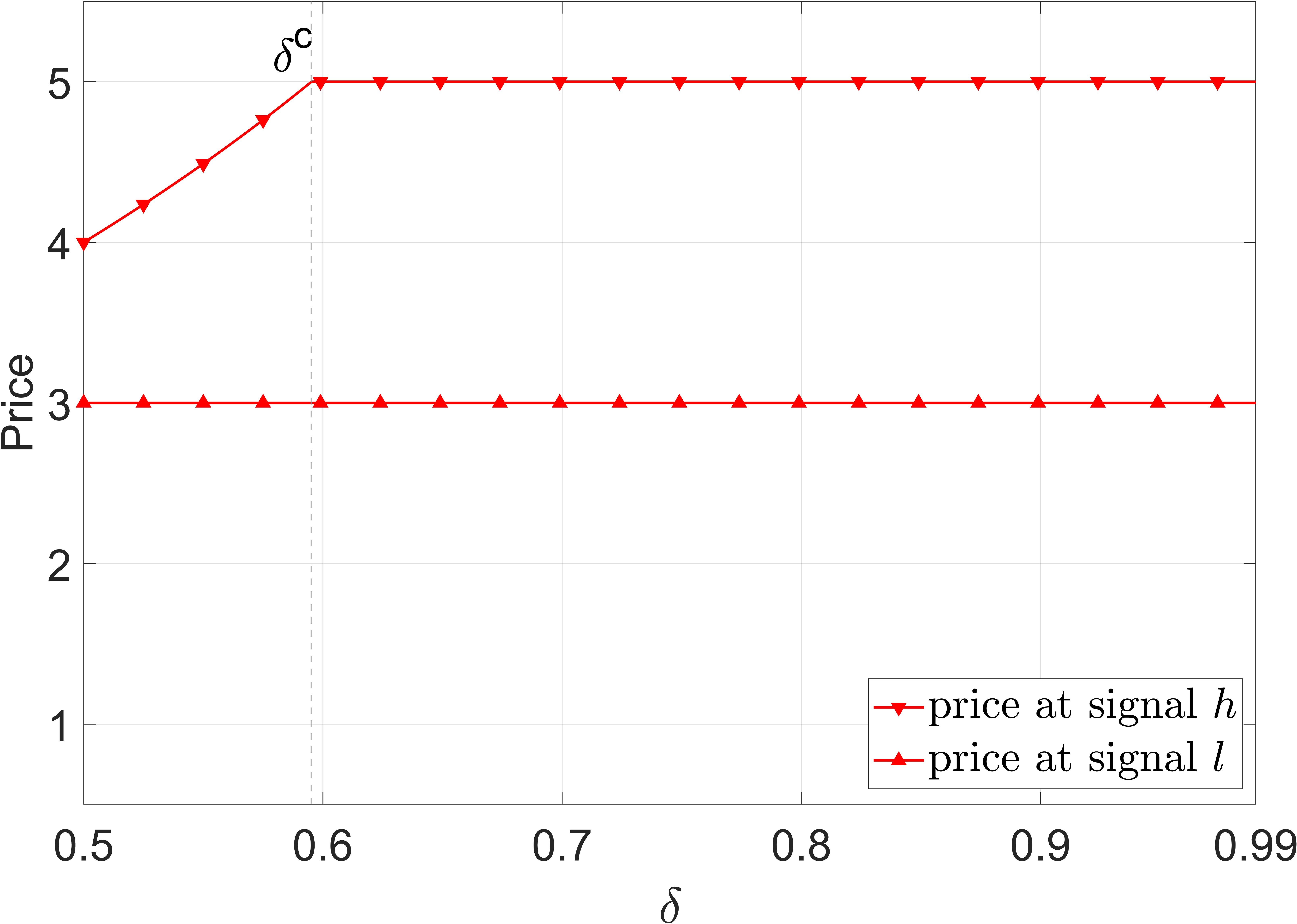

- Upper Censorship: Low demand states are revealed truthfully with probability ρ; high states are always reported truthfully. By pooling information about high-demand states, this rule is designed to optimally balance incentive constraints and collusive profit.

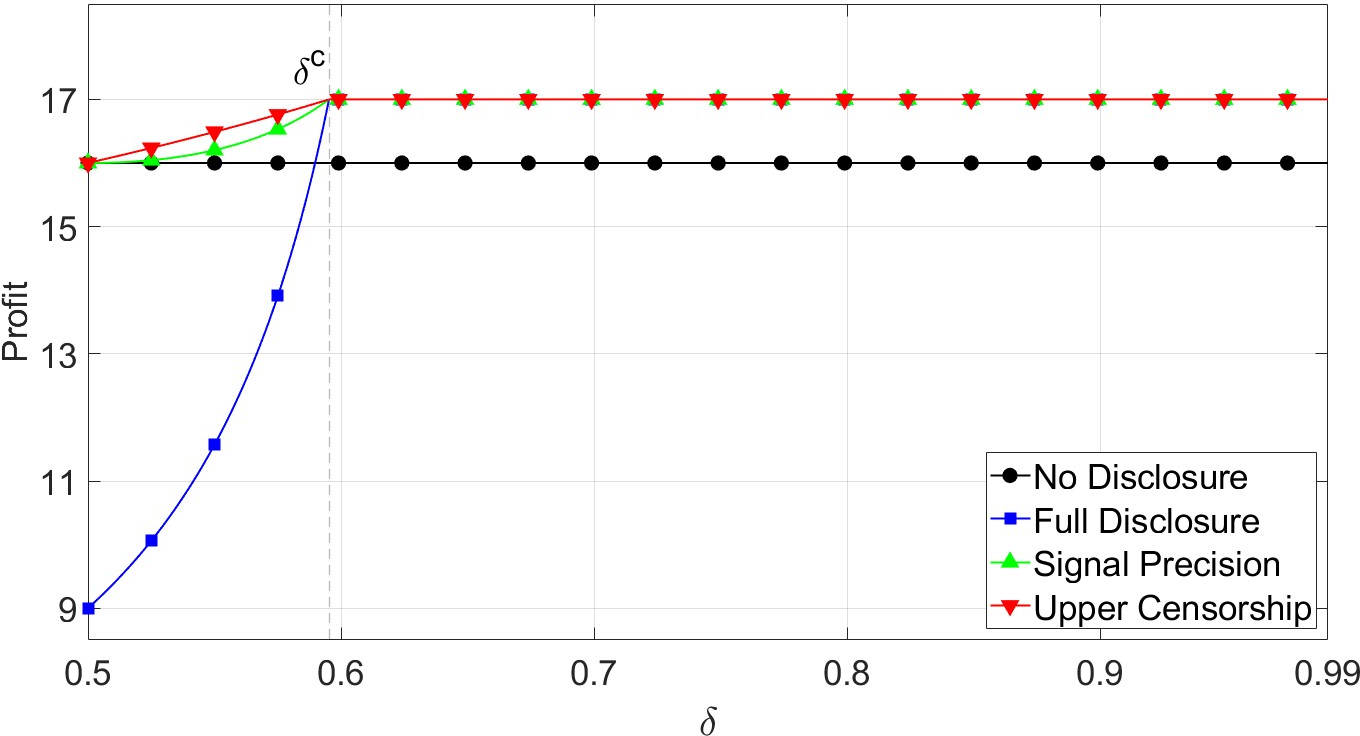

The theoretical analysis seeks the optimal collusive profits attainable under each rule by solving an information design problem that parallels the Bayesian persuasion literature. The core tradeoff is between maximizing monopoly prices when demand is high and maintaining incentive compatibility (i.e., limiting profitable deviation).

The optimal theoretical joint profit curves under each rule are summarized in (Figure 1):

Figure 2: Theoretical joint profits as a function of the discount factor δ under no disclosure, full disclosure, and upper censorship.

The analysis yields three key predictions: (1) upper censorship strictly dominates full disclosure in attainable profits; (2) for low δ, no disclosure yields higher profits than full disclosure; and (3) for high δ, full disclosure surpasses no disclosure—i.e., the standard comparative statics from collusion theory.

Q-Learning Algorithmic Implementation

The Q-learning agents discretize the price space and operate with K=1 memory (state includes previous prices and received signals), using ε-greedy exploration decaying over time. Signal structures map to distinct state-space partitions depending on the information environment, and Q-matrices are independently updated. Agents learn via asynchronous Q-updates, with profits and optimal policies estimated after convergence as characterized by the price cycle (absorbing strongly connected component in the induced Markov process).

The implementation simulates $1,000$ independent runs per configuration, varying δ from θH0 to θH1 and, for censorship, grid-searching optimal θH2.

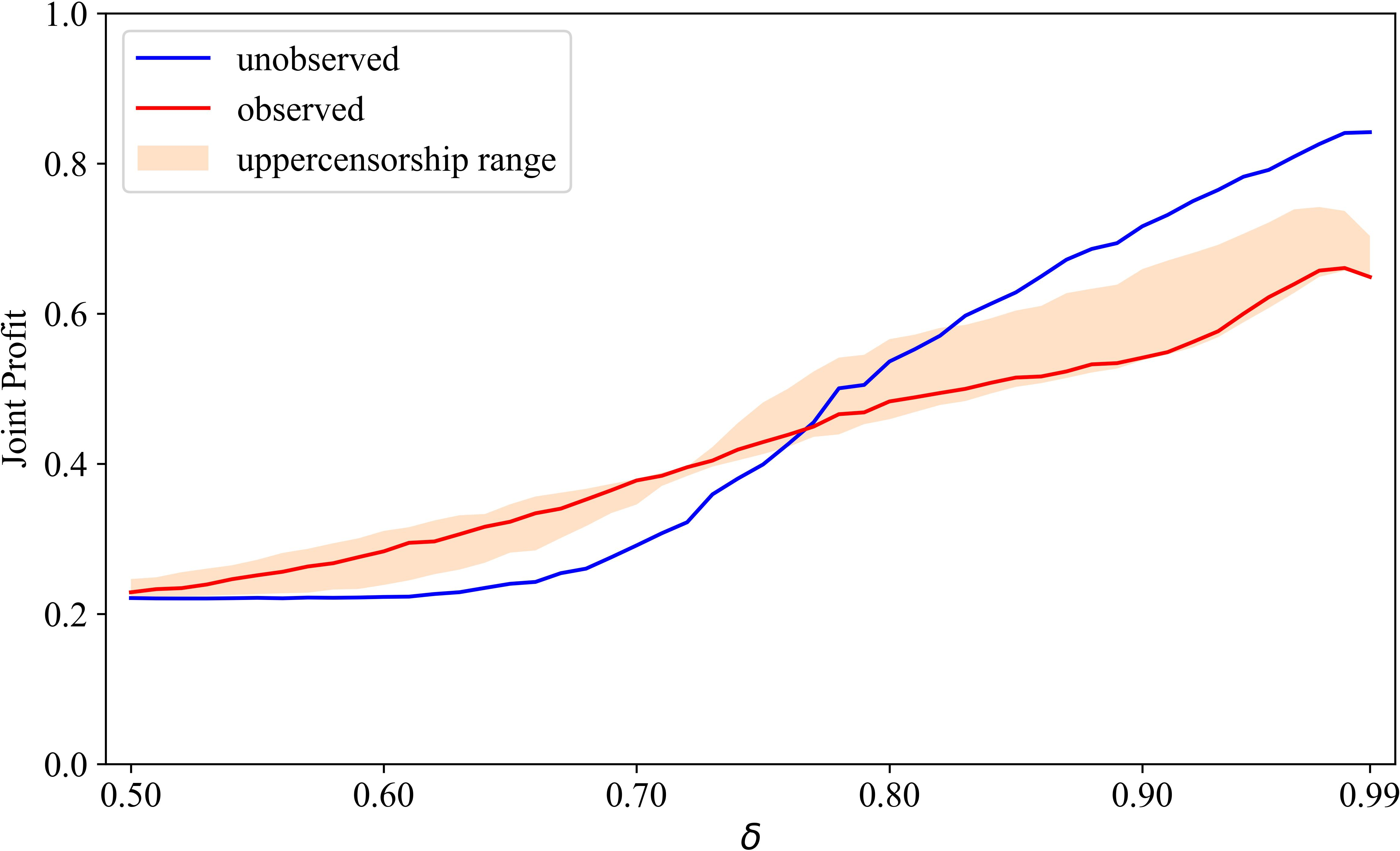

Empirical Results: Learning Dynamics and Profit Comparisons

Simulation reveals that Q-learning agents respond systematically to information structure, and numerical profit comparisons deviate sharply from theoretical equilibrium predictions. The main results are:

Analysis of No Disclosure

The pricing dynamics and profit outcomes under the no disclosure regime are particularly revealing: as θH9 increases, agents internalize the long-term value of collusion despite limited information and reach collusive prices rivaling or surpassing those in more informative environments.

Figure 3: Q-learning dynamics and profit outcomes under the no disclosure regime as ρ0 varies.

Robustness and Alternative Environments

The profit reversal and the dominance of upper censorship are robust to several extensions:

- Alternative selective disclosure (signal precision): When signal informativeness is tuned symmetrically via noisy messages, upper censorship remains strictly superior in achievable collusive profits.

- Logit demand environment: The reversal and dominance patterns persist in differentiated logit demand, indicating that the result is not an artifact of linear demand.

- Exploration and memory robustness: Parameter variations in ρ1, ρ2, and memory length do not reverse the qualitative findings regarding profit reversal and information structure sensitivity.

Implications and Future Directions

Theoretical Implications

The results emphasize a profound divergence between equilibrium comparative statics and actual learning dynamics in markets mediated by Q-learning agents. Classical repeated-game theory would predict that more information enables more nuanced trigger strategies (e.g., state-dependent punishments), promoting collusion as patience increases. By contrast, decentralized trial-and-error learning can invert these intuitions: less information may coordinate agents onto robust collusive cycles, especially at high discounting.

Policy and Practical Implications

The findings carry strong implications for the regulation of algorithmic pricing and the design of third-party information platforms:

- Information restriction as an antitrust tool may backfire if algorithms rely on reinforcement learning, as limiting disclosure can inadvertently strengthen supracompetitive outcomes.

- Careful information design (e.g., upper censorship) can systematically influence collusive potential, creating an avenue for regulatory agencies to intervene in market information architectures rather than simply curbing data access.

- The divergence between equilibrium predictions and learned outcomes reinforces the necessity of simulation-based and data-driven policy evaluation when overseeing AI-mediated markets.

AI and Market Design

The paper also highlights that properties of reinforcement learning algorithms, such as bounded memory, function approximation, and action selection, interact nontrivially with market information structure. This amplifies the need for integrated study between algorithmic learning theory and algorithmic mechanism/market design. Extensions to heterogeneous models, multi-agent deep RL, and endogenously evolving market structures are natural directions for further research.

Conclusion

This paper provides an in-depth analysis of how Q-learning algorithms in competitive pricing settings respond to different information disclosure rules, combining formal information design theory with large-scale RL simulation. The evidence demonstrates that optimal information design (upper censorship) reliably maximizes joint profits, while the empirical reversal of profit rankings between no disclosure and full disclosure as a function of ρ3 underscores fundamental discrepancies between learning-based and equilibrium-based comparative statics. These results caution against regulatory approaches that focus solely on information restriction and highlight the need for explicit consideration of algorithmic learning dynamics in the formulation of antitrust and market policy in the era of AI-mediated commerce (2607.04345).