- The paper introduces a fully Bayesian loss-based method that efficiently selects sparse vine copula models in high dimensions.

- The approach integrates sparsity-inducing priors with a parallel Shotgun Stochastic Search algorithm to jointly choose vine structure, copula families, and parameters.

- Simulation and real-data financial studies demonstrate rapid convergence, reduced complexity, and consistent model selection with improved prediction accuracy.

Loss-Based Bayesian Model Selection of Vine Copulas

Introduction and Motivation

The paper "Bayesian model selection of vine copulas: a loss-based perspective" (2606.21512) addresses the challenge of Bayesian model selection for vine copulas in high-dimensional dependence modeling. Vine copulas are a powerful class of multivariate tools that assemble flexible, hierarchical dependence structures from bivariate pair copulas, enabling tailored modeling of heterogeneity and tail dependence across variables. However, existing Bayesian approaches suffer from computational intractability as the dimensionality increases, due to the super-exponential growth in possible vine structures and the necessity of jointly selecting copula families and parameters.

This work systematically integrates sparsity-inducing loss-based priors with a scalable Shotgun Stochastic Search (SSS) algorithm to enable efficient exploration of the vine structure space, including truncated and sparse vine models. The methodology is fully Bayesian: it jointly identifies the vine structure, selects copula families, and estimates parameters while promoting parsimony. The authors demonstrate both theoretical rigor and practical advances via extensive simulation studies and a substantive financial application.

Vine Copula Representation and Complexity

Regular vine copulas (R-vines) decompose multivariate distributions into a sequence of trees, each comprising edges associated with pair-copulas. The number of possible vine structures grows as 2(d−3)(d−2)/2−1d!, and the number of possible pair-copula combinations grows factorially with dimension, leading to computational challenges. Classical approaches prioritize canonical (C-vine) or drawable (D-vine) structures to restrict this space, but even with fixed orderings, model selection remains nontrivial as the family and parameters of each bivariate copula must be chosen.

The paper adopts the simplifying assumption that pair-copula densities are independent of the conditioning values—a tractable and widely used approximation in vine copula modeling.

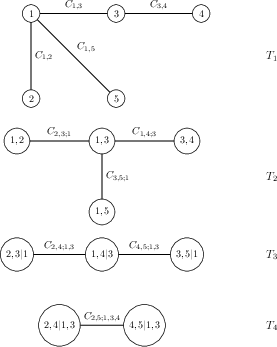

Figure 1: Example of a five-dimensional regular vine structure, illustrating the multi-level nested tree representation and the assignment of pair copulas to edges.

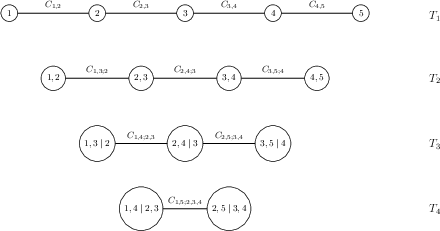

Figure 2: Example of a five-dimensional drawable (D-vine) structure, highlighting the sequential path-based tree construction.

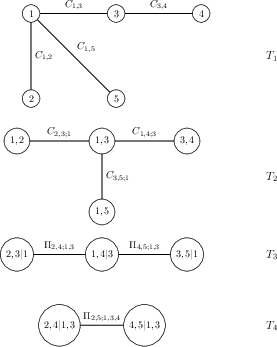

Figure 3: Truncated five-dimensional regular vine structure, where pair-copulas beyond level 2 are set to independence, illustrating sparsity induction.

Loss-Based Priors for Sparsity and Model Complexity

The cornerstone of the proposed framework is the loss-based prior, originally inspired by Villa and Walker [Villawalker2015JASA], which quantifies the penalty for omitting the true model from the search space by combining:

- Information Loss: The Kullback–Leibler (KL) divergence between the candidate model and the closest alternative, encapsulating the cost of discarding a model if it is true.

- Complexity Loss: Explicit penalization of model complexity, parameterized by the number of copulas and the structural depth (truncation level) of the vine.

The prior mass for a model is proportional to exp{−LossI(M)−LossC(M)}, with tuning parameters governing the sparsity-inducing strength. Higher complexity and deeper tree levels are penalized, promoting selection of parsimonious structures.

Figure~\ref{fg:fullprior_d10} (not shown) demonstrates via simulation that increasing complexity penalties in the prior sharply concentrate probability on sparse and truncated models, reducing the selection of saturated vines.

Bayesian Posterior Computation and Model Selection

Posterior inference is conducted in two stages:

- Model Selection: Efficient traversal of the discrete vine and copula family space is performed using a parallelized Shotgun Stochastic Search (SSS) algorithm, which rapidly explores neighborhoods by proposing local perturbations and maximizing posterior mass.

- Parameter Estimation: For the chosen optimal model, parameters are estimated via MCMC with adaptive proposals, where uniform priors are set on support consistent with the copula family of each pair.

The approach enables movement between full, truncated, and sparse vine models within the same structure, allowing the SSS to escape local optima and converge swiftly even in high dimensions.

Simulation Study: Numerical Validation and Consistency

Three simulation investigations validate the approach:

- Performance Validation: In low dimensions (4, 6), the method achieves strong recovery of true copula families and truncation levels. Selection error rates for copula families decline sharply with increasing sample size, and estimated Kendall's τ parameters are close to generative values.

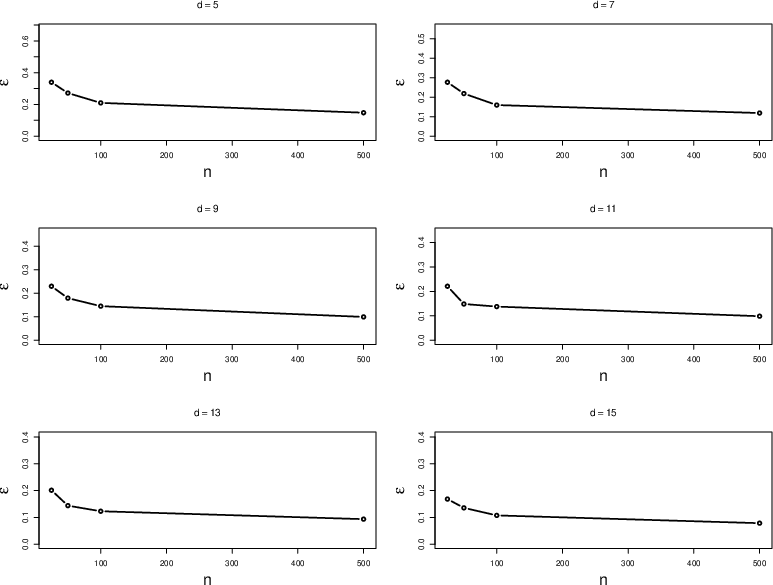

- Consistency in High Dimensions: The overall error rate ϵ for model selection decreases systematically with sample size across dimensions d=5 to d=15, as shown in the simulation panel.

Figure 4: Error rate ϵ (y-axis) versus sample size n (x-axis) for multiple dimensions, evidencing robust consistency and scalability for model selection.

- Prior Sensitivity: As complexity penalty parameters are increased, the frequency of selecting highly truncated models increases, especially at small sample sizes. However, the prior's influence wanes as data accumulates, confirming the Bayesian interplay between prior and likelihood.

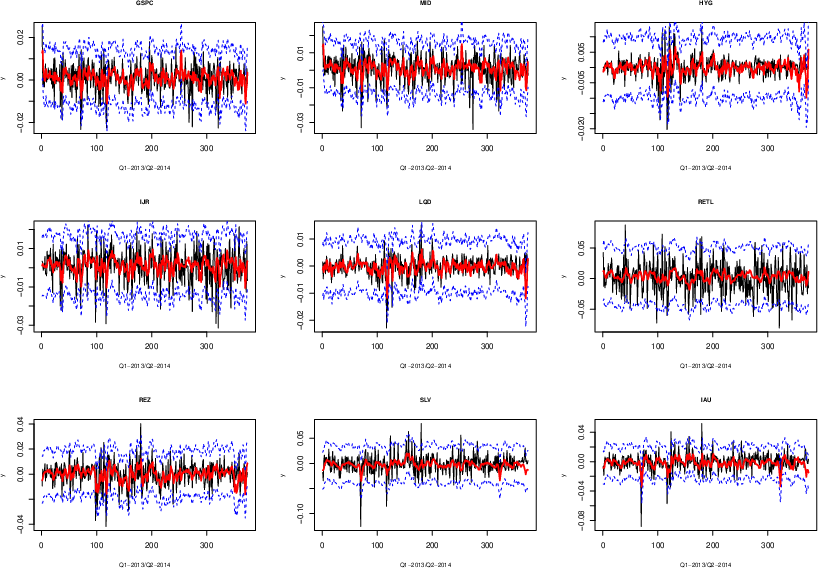

Real Data Application: Financial Portfolio Modeling

The practical efficacy of the approach is showcased on a 9-dimensional ETF returns dataset, previously used in Bayesian vine model selection studies. Marginal distributions are first modeled using dynamic linear models, followed by dependence structure estimation via the proposed Bayesian SSS-loss-based vine method.

The selected model is markedly more parsimonious than the traditional sequential selection yet achieves equivalent out-of-sample prediction performance, as evidenced by identical RMSEs across assets. The optimal R-vine selected truncates after tree level five with numerous pair-copulas set to independence.

Figure 5: Forecasts for each ETF asset over time: red lines indicate predictive means, blue dashed lines denote credible intervals, and black lines show observed realizations.

Implications and Future Directions

This work provides a theoretically sound and practically scalable Bayesian approach for vine copula model selection in moderately high dimensions. By combining rigorous loss-based priors and stochastic search, the method achieves fast convergence, robust consistency, and enhanced interpretability through sparse modeling. Contrasting prior Bayesian attempts, this approach enables real-world deployment in applications where complexity and uncertainty are pervasive (e.g., finance, hydrology, environmental statistics).

Practically, the framework promotes interpretability and computational tractability, enabling analysts to balance model complexity and fit without sacrificing predictive accuracy. Theoretically, it motivates further exploration of loss-based priors in hierarchical and multi-level multivariate models.

Future developments could involve:

- Extensions to dynamic/time-varying vine copula models for streaming data

- Conditional copula modeling with covariate-dependent parameters

- Integration with frequentist sparsity-inducing regularization for hybrid estimation

- Application to ultra-high dimensional genomics and sensor network data

Conclusion

The paper introduces a fully Bayesian solution to vine copula model selection based on sparsity-inducing loss-based priors and parallelizable stochastic search. The methodology achieves competitive predictive performance while substantially reducing model complexity. Simulation and empirical evidence support strong consistency and scalability. This approach advances the feasibility and interpretability of Bayesian vine copula modeling and opens new avenues for complex dependence structure analysis in multivariate domains.