- The paper establishes the equivalence between the HJB equation and Feynman–Kac representation for optimal harvesting under stochastic control.

- It employs rigorous stochastic analysis and numerical simulations using fisheries data to derive and validate a feedback optimal harvesting policy.

- The study offers practical insights for adaptive resource management by integrating dynamic programming and backward stochastic frameworks.

Optimal Harvesting under Stochastic Control: Unified HJB and Feynman–Kac Approaches

Introduction

This paper, "Optimal Harvesting under Stochastic Control: HJB Equation and Feynman-Kac Representation" (2606.08428), systematically develops and analyzes stochastic control paradigms for renewable resource management under ecological and economic uncertainty. Focusing on renewable stock dynamics subject to stochasticity and management decisions, the work bridges two foundational approaches: the PDE-driven dynamic programming principle via the Hamilton–Jacobi–Bellman (HJB) equation and the martingale/backward stochastic framework of the nonlinear Feynman–Kac (FK) representation.

Under a controlled SDE for resource dynamics, the study constructs, analyzes, and empirically implements a finite-horizon discounted expected profit maximization problem. Rigorous existence, uniqueness, and verification theorems for value functions and optimal controls are provided, and the exact mathematical equivalence of the HJB and Feynman–Kac approaches is both established theoretically and validated numerically. The empirical component, using production data from major capture fisheries, demonstrates the translation of theory into practice for policy-relevant inference.

Stochastic Control Framework

The stock process X(t) evolves according to a controlled SDE with multiplicative noise, where the control E(t) acts via extraction-induced drift shrinkage:

dX(t)=[f(X(t))X(t)−qE(t)X(t)]dt+σX(t)dW(t).

Here, f(⋅) is the per capita growth rate, q the catchability coefficient, σ the volatility, and E(t) the admissible harvesting effort, all under Brownian environmental perturbation. Empirical implementation utilizes normalized annual data, with model drift and volatility estimated for several leading fishing nations.

The objective is to maximize expected discounted profit over [t,T]:

J∗(t,X)=E(⋅)maxE[∫tTe−δ(s−t)Π(s,Xs,Es)ds∣Xt=X],

subject to the cost/benefit structure

Π(s)=pqE(s)X(s)−c1E(s)−c2E(s)2,

with E(t)0 the discount rate, E(t)1 the price, and E(t)2 the cost parameters. By imposing strict concavity (via E(t)3), existence and uniqueness of optimal feedback controls are rigorously ensured.

The HJB Equation and Feedback Optimal Policy

Dynamic programming and Itô calculus yield the HJB PDE for the value function E(t)4:

E(t)5

with terminal condition E(t)6.

The control optimization yields the unique feedback law:

E(t)7

The optimal effort is thus explicitly regulated by the current state and the gradient E(t)8, realizing the marginal economic value of the stock in the control.

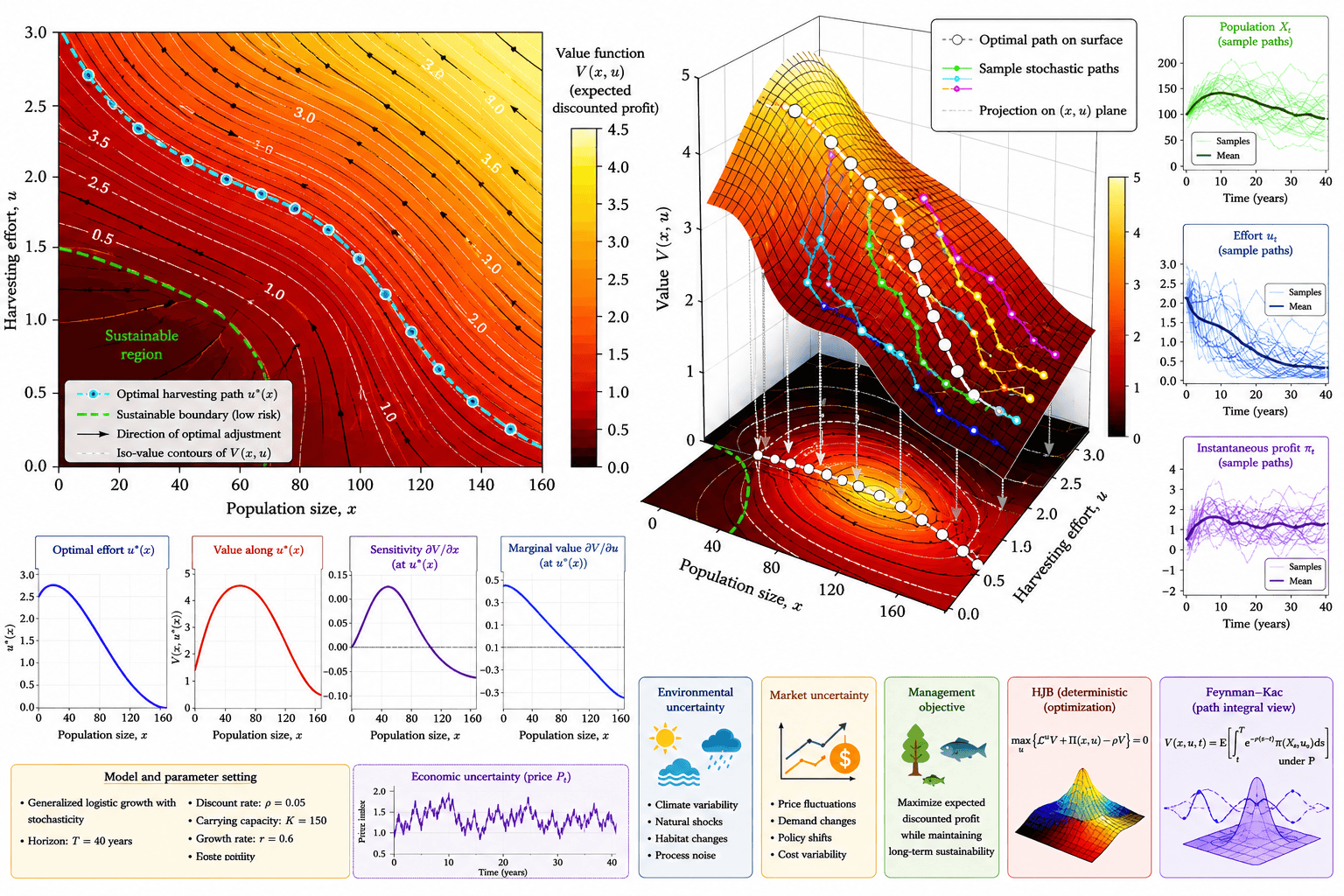

Figure 1: Optimal harvesting under stochastic ecological and economic uncertainty using heatmap and three-dimensional value function representations.

Feynman–Kac (Nonlinear BSDE) Path Representation

The nonlinear Feynman–Kac theorem provides a forward-backward SDE characterization of the value process and its stochastic sensitivity:

E(t)9

where the driver

dX(t)=[f(X(t))X(t)−qE(t)X(t)]dt+σX(t)dW(t).0

encapsulates the quadratic HJB nonlinearity and control feedback.

This nonlinear backward stochastic representation is essential for analyzing path-dependent payoffs, allowing a probabilistic interpretation as an expectation over controlled state trajectories and matching the PDE-based value.

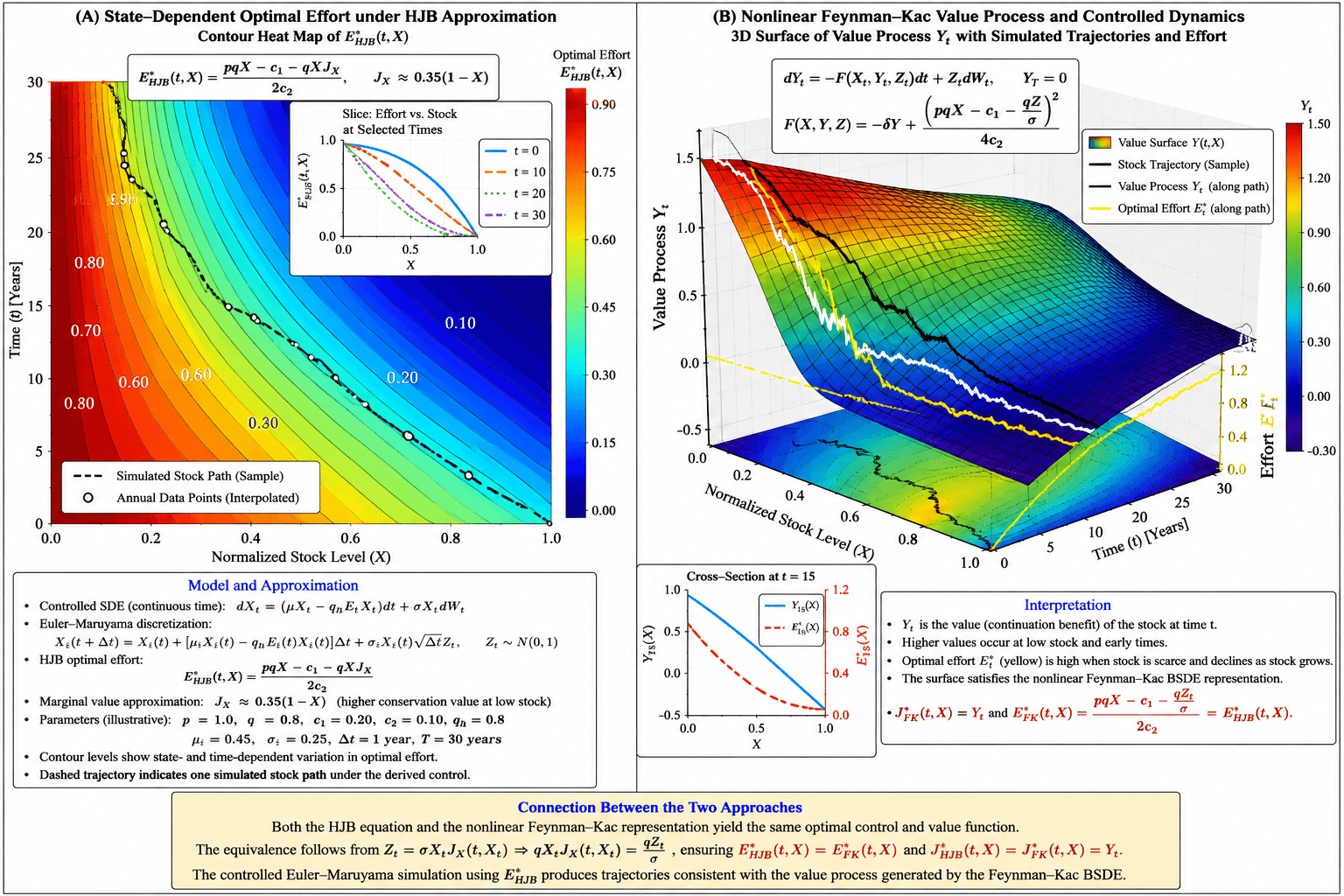

Figure 2: Contour heat map and three-dimensional representation of the controlled stochastic harvesting model under the HJB equation and nonlinear Feynman--Kac representation.

Equivalence of HJB and Feynman–Kac Approaches

A key result—proved via Itô's lemma and uniqueness of solutions—is that the HJB value function and optimal policy are exactly reproduced by the Feynman–Kac backward SDE representation. The relationship dX(t)=[f(X(t))X(t)−qE(t)X(t)]dt+σX(t)dW(t).1 maps the PDE gradient to the BSDE martingale integrand, and both approaches generate identical optimal effort and value paths under admissible state processes.

Numerical Methods and Data-Driven Simulation

Numerical implementation combines:

- Euler–Maruyama discretization for controlled SDEs,

- Empirical estimation of drift and volatility from normalized fisheries catch data,

- Value gradient approximations (dX(t)=[f(X(t))X(t)−qE(t)X(t)]dt+σX(t)dW(t).2) for computational tractability,

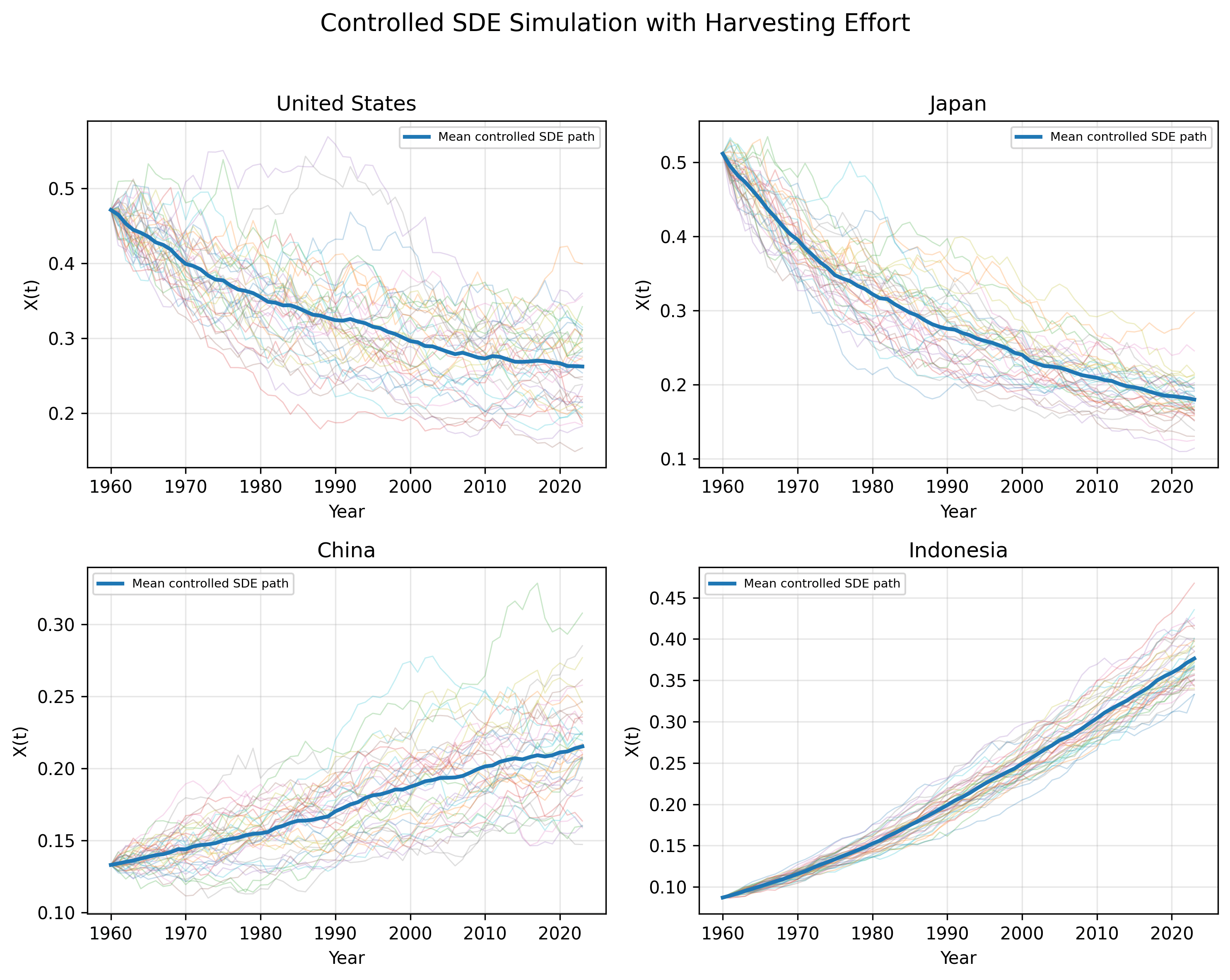

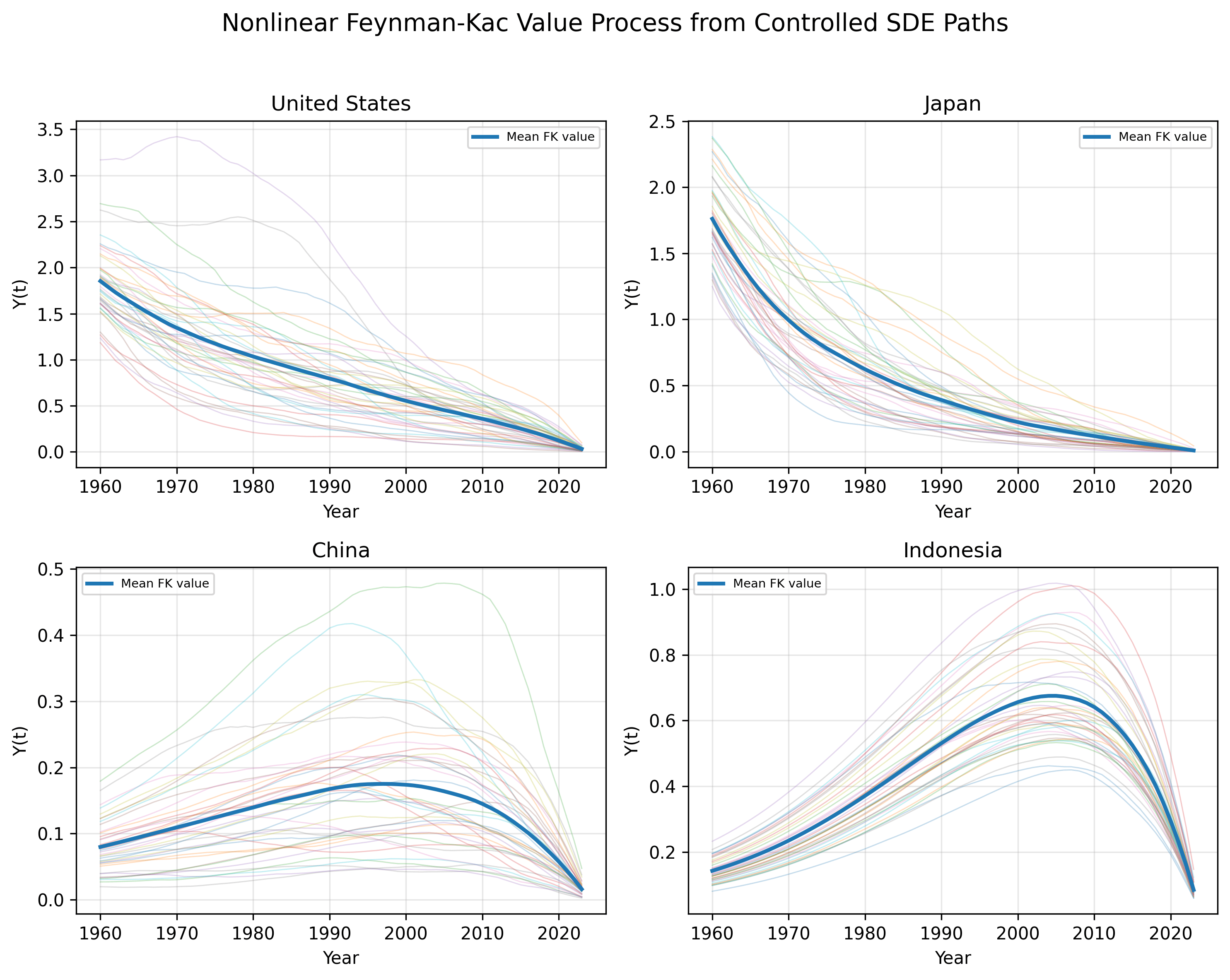

- Simulation of paths and controls for China, Indonesia, Japan, and the United States.

The empirical drift and volatility estimates reflect diverse fisheries realities: strong positive drift for Indonesia (rapid stock growth), negative drift for Japan (stock decline), and largest volatility for the United States.

Figure 3: Controlled SDE state paths using real-data-estimated drift and volatility. Thin lines represent simulated controlled paths, while the thick line represents the mean controlled path.

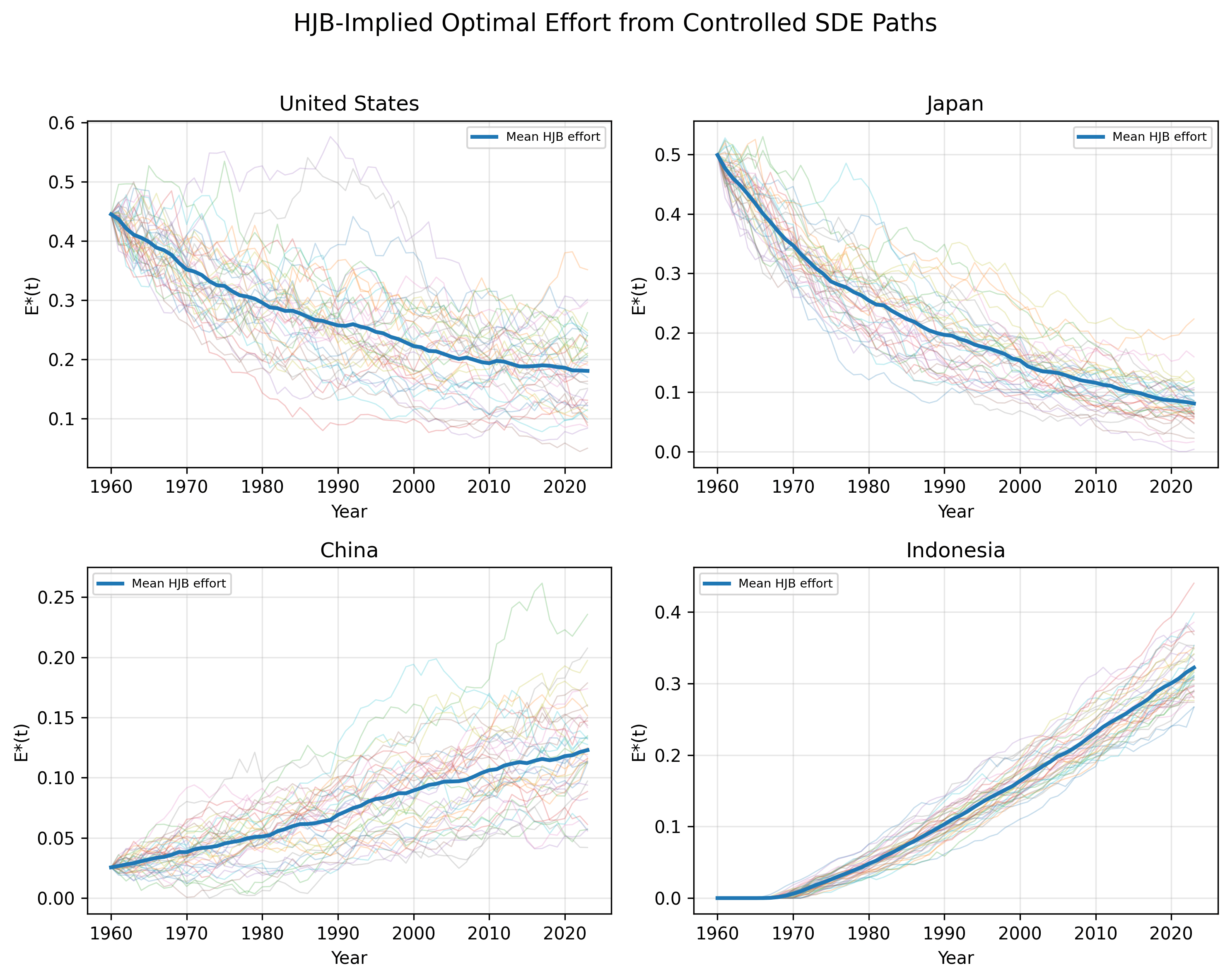

Figure 4: HJB-implied optimal effort paths generated from controlled SDE simulations.

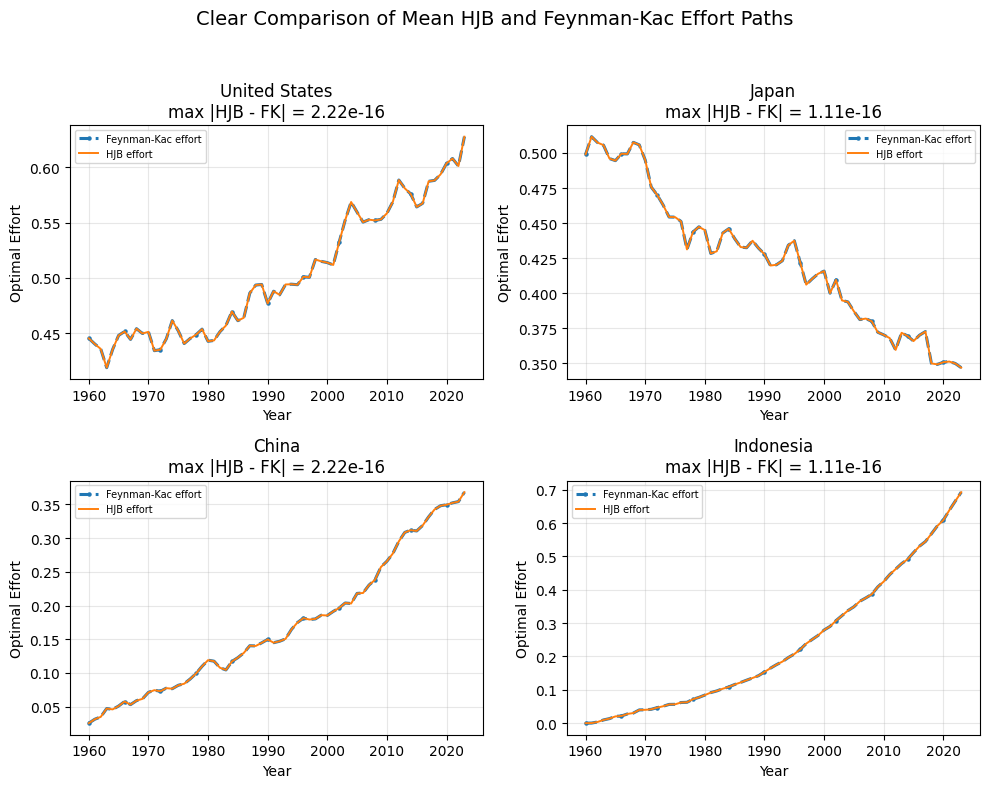

The stochastic controlled paths, value processes, and effort trajectories are compared for each nation. The observed perfect numerical match between HJB and Feynman–Kac derived controls (with discrepancies only at floating-point precision) robustly confirms their equivalence for the empirical cases.

Figure 5: Nonlinear Feynman--Kac value process generated from controlled SDE paths.

Figure 6: Comparison of mean HJB and nonlinear Feynman--Kac effort paths under the controlled SDE.

Practical and Theoretical Implications

Practical Implications:

- The framework enables the construction of robust state- and time-dependent harvesting policies that explicitly adapt to environmental stochasticity and empirical bioeconomic parameters.

- Marginal value regularization (through dX(t)=[f(X(t))X(t)−qE(t)X(t)]dt+σX(t)dW(t).3 or its stochastic analog) naturally dampens overexploitation under resource scarcity, promoting sustainability without constant manual policy adjustment.

- The exact equivalence (in both value and control) between the HJB and Feynman–Kac approaches allows flexibility in numerical implementation—either deterministic PDE solvers (when feasible) or Monte Carlo BSDE simulations—crucial for high-dimensional generalizations (e.g., coupled ecological-economic systems, intricate multi-stock dynamics).

Theoretical Implications:

- The rigorous SDE/BSDE convergence and uniqueness results establish a template for stochastic resource control analysis under finite horizon and with general concave economic functional forms.

- The approach generalizes to models with price volatility, regime-switching, or path-dependent payoffs given the martingale framework.

- The probabilistic representation facilitates the integration of real-world data streams and simulation-based optimization, opening avenues for hybrid data-driven and theory-driven adaptive management algorithms.

Speculation on Future Directions:

- Extension to multi-species, spatially structured, and regime-switching environments, potentially with mean-field feedback, is technically straightforward using the same SDE/BSDE infrastructure.

- Integration with dynamic market pricing and regulatory constraints (e.g., quotas, taxes) is enabled by the direct feedback connection between the marginal value function and optimal control.

- Data-adaptive schemes leveraging reinforcement learning or actor-critic methods may be synthesized with the pathwise BSDE framework, enabling real-time adaptive harvesting policies.

Conclusion

This paper rigorously constructs and empirically implements a unified stochastic control approach to optimal resource harvesting, demonstrating the equivalence of dynamic programming via HJB and backward SDE/Feynman–Kac path integrals. The analytical framework provides robust, mathematically consistent, and practically implementable strategies for resource management under uncertainty, with strong empirical validation using fisheries data. Future developments will likely generalize these models to high-dimensional, multi-agent, and policy-constrained ecological-economic systems, making the theoretical tools established here foundational for next-generation stochastic management science.