- The paper shows that in auctions with horizontal differentiation, winning generates a positive conditional value (winner’s bliss) when the alignment parameter μ is below 0.5.

- It derives symmetric Bayes-Nash equilibrium strategies, highlighting how bids exceed ex-ante values at low signals due to heterogeneous bidder preferences.

- The analysis reveals that auction revenue declines with increased preference alignment and that state disclosure can reduce competition in such settings.

Winner’s Bliss in Common-Value Auctions under Horizontal Differentiation

Introduction and Context

This paper establishes the effect termed as “winner’s bliss” in common-value auctions by introducing horizontally differentiated preferences among bidders. Contrary to the conventional winner’s curse—in which winning signals over-optimism—the analysis demonstrates that when bidder valuations are based on divergent interests over possible states, winning can instead be affirming. In particular, the framework considers a parametrized departure from pure horizontal differentiation (μ=0) to fully aligned values (μ=1), showing that the selection effect is reversed in the presence of horizontal heterogeneity.

The authors motivate the study by highlighting its relevance to online advertising markets and bilateral trading environments wherein bidders’ preferences are not purely vertically ordered but depend on partially disjoint criteria. They reference recent theoretical work exploring alternative “winner’s blessing” channels (e.g., allocation bias, uncertain market thickness), emphasizing that horizontal heterogeneity constitutes a fundamentally distinct mechanism.

Model Structure

A two-bidder first-price auction environment is introduced. The object has an unknown binary state θ∈{A,B}, with each bidder’s payoff determined by whether the realized state matches her private type. Types are correlated with probability μ; for μ=0 there is complete horizontal differentiation, and for μ=1, bidders are perfectly aligned. Bidders receive independent uniform signals about the state, and their expected valuations depend on both signals.

This configuration enables tractable characterization of equilibrium strategies for all μ∈(0,1]. Notably, the equilibrium collapses in pure horizontal settings (μ=0), since monotonicity fails: strategic outbidding (even at low signals) is incentivized when preferences are maximally differentiated.

Main Results

Equilibrium Bidding Strategies

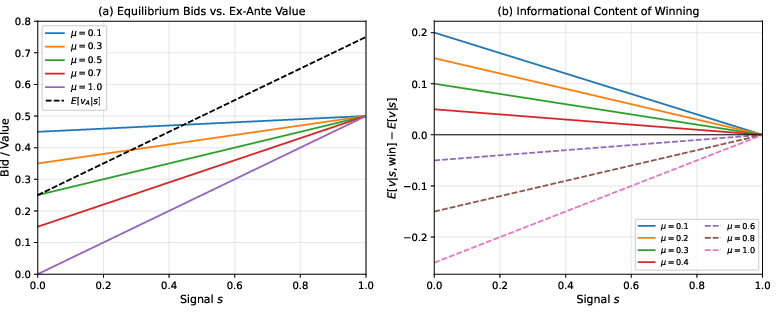

The symmetric Bayes-Nash equilibrium bid functions exhibit monotonicity in the signal and interpolate between private-value and common-value cases as μ varies:

Figure 1: (a) Equilibrium bidding strategies for varying μ; dashed line is the ex-ante value μ=10. For μ=11, bids exceed ex-ante value at low signals. (b) Conditional value gain from winning, positive for μ=12 (winner's bliss), negative for μ=13 (winner's curse).

The analysis reveals that when μ=14, “winner's bliss” is realized: the act of winning yields a conditionally higher expected value than the ex-ante expectation from one’s own signal, as winning implies the rival holds a confirmatory signal. Conversely, with sufficiently aligned preferences (μ=15), the winner's curse arises: winning is evidence of overestimation.

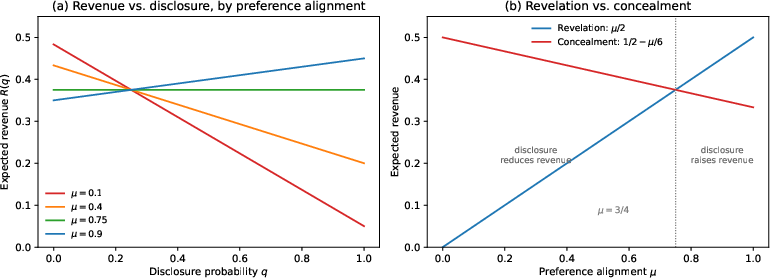

A salient implication concerns auction revenue. The expected revenue μ=16 decreases monotonically with preference alignment. The classical linkage principle is overturned in settings of differentiated preferences: revealing the object’s state reduces revenue for μ=17, as it mitigates the competition that arises when bidders are uncertain but have divergent interests. Disclosure is only revenue-improving for highly aligned agents (μ=18).

Figure 2: (a) Auction revenue μ=19 as a function of disclosure probability θ∈{A,B}0 across values of θ∈{A,B}1, decreasing for θ∈{A,B}2. (b) Crossover point for revelation and concealment: at θ∈{A,B}3, disclosure switches from revenue-reducing to revenue-improving.

This result echoes and refines prior findings that “ignorance promotes competition,” demonstrating that the effect is strictly linked to the nature (and sign) of value interdependence. The allocation effect dominates the standard linkage principle under horizontal differentiation.

Bilateral Trade and Selection Effects

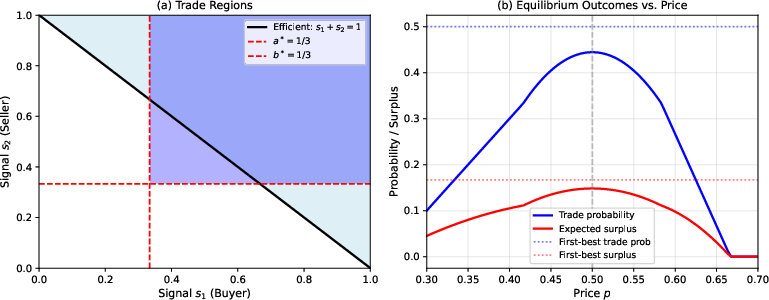

In the two-sided market application, the model shows that, with horizontal differentiation, asymmetric information fosters advantageous selection: the willingness of the counterparty to trade is positive news regarding the value of the good. This fosters high surplus efficiency (88.9%), in sharp contrast to the classical adverse selection effect (no-trade theorem) encountered with aligned preferences.

Figure 3: (a) Trade regions in the signal space: dark region is equilibrium trade, light region is efficient trade. (b) Trade probability and surplus as functions of price θ∈{A,B}4; surplus maximized at θ∈{A,B}5 with realized efficacy close to first-best.

Advantageous selection yields increased trading volumes and surplus, substantiating the hypothesis that horizontal heterogeneity (where “opposed” counterparties infer favorable private information from willingness to transact) is a key determinant of market activity.

Theoretical and Practical Implications

The findings theoretically challenge the universality of winner’s curse, adverse selection, and the linkage principle in environments with horizontally differentiated preferences. For platform design in online advertising and similar settings, optimal information structure pivots critically on the preference alignment parameter θ∈{A,B}6, contradicting recommendations derived under the canonical fully aligned paradigm.

Theoretically, these results open directions for mechanism design in multi-dimensional type spaces where private information may foster, rather than preclude, efficient allocation and transaction. Empirically, there is an impetus to identify environments where winner's bliss and advantageous selection might be observed, and to parameterize real-world auctions along these dimensions.

Conclusion

This work provides a rigorous analysis of common-value auctions with horizontally differentiated preferences, demonstrating that preference heterogeneity induces a reversal of classic selection effects—winner’s bliss and advantageous selection replace winner’s curse and adverse selection. These phenomena have first-order consequences for auction revenue, platform information policy, and bilateral trade outcomes. The results suggest new avenues for mechanism design and empirical validation, particularly in markets characterized by multi-dimensional or stylistically divergent agents.