- The paper establishes an equilibrium model featuring divergent behavioral regimes where institutional investors use Kelly optimization and retail consumers drive utility-based token dynamics.

- It reveals that speculative token bubbles emerge in regimes of persistent retail HODLing, generating significant structural excess returns through leveraged fiat inflows.

- In contrast, rational two-way consumer flows dissolve institutional arbitrage, anchoring token prices to utility-driven baselines and preserving network security.

Token Valuation Dynamics in Proof-of-Stake under EIP-1559: Institutional Capital, Consumer Behavior, and Equilibrium Structures

Model Architecture and Behavioral Regimes

This paper introduces a rigorous open-economy macroeconomic equilibrium model capturing the interplay between a Kelly-optimizing institutional investor and a utility-driven retail consumer in a PoS system with EIP-1559 fee-burn. The work delineates two primary behavioral regimes: (i) the Unbounded Accumulation Model, characterized by perpetual retail HODLing and exogenous fiat inflow, and (ii) the Utility-Consumption Model, where the consumer dynamically balances crypto holdings with real-world consumption, utilizing a Cobb-Douglas utility specification.

Each agent type is parameterized by explicit state variables encompassing portfolio weights, wealth, token demand, and liquidity preferences. The institutional investor maximizes long-term expected geometric wealth in the presence of inefficient fiat opportunity cost (μr−σr2<0), adjusting their risk through Kelly optimization. The retail consumer injects outside capital for utility or speculative accumulation, with transaction utility modulated by the fee-burn mechanism—enforcing permanent principal and yield destruction for gas consumption.

Unbounded Accumulation: Speculative Dynamics and Investor Alpha

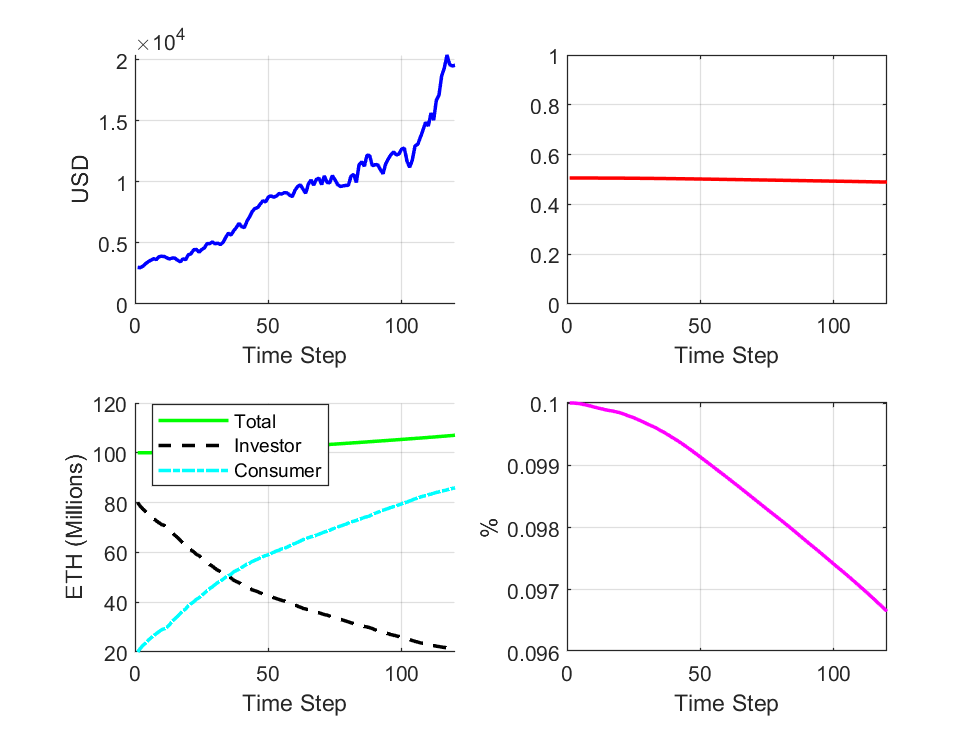

In the unbounded accumulation baseline, the retail consumer injects exogenous fiat and accumulates tokens unidirectionally (HODL), while the institutional investor serves as a sole liquidity provider, persistently offloading native tokens to consumers. The model formalizes a deterministic structural bubble, with fiat inflows creating compounding buy-side pressure that is systematically arbitraged by the institutional participant. Notably, simulations indicate pronounced exponential drift in token price over a decadal horizon, despite volatility propagated via exogenous TradFi shocks. Investor token balances (and hence network monopoly risk) decrease monotonically due to relentless Kelly-driven portfolio rebalancing.

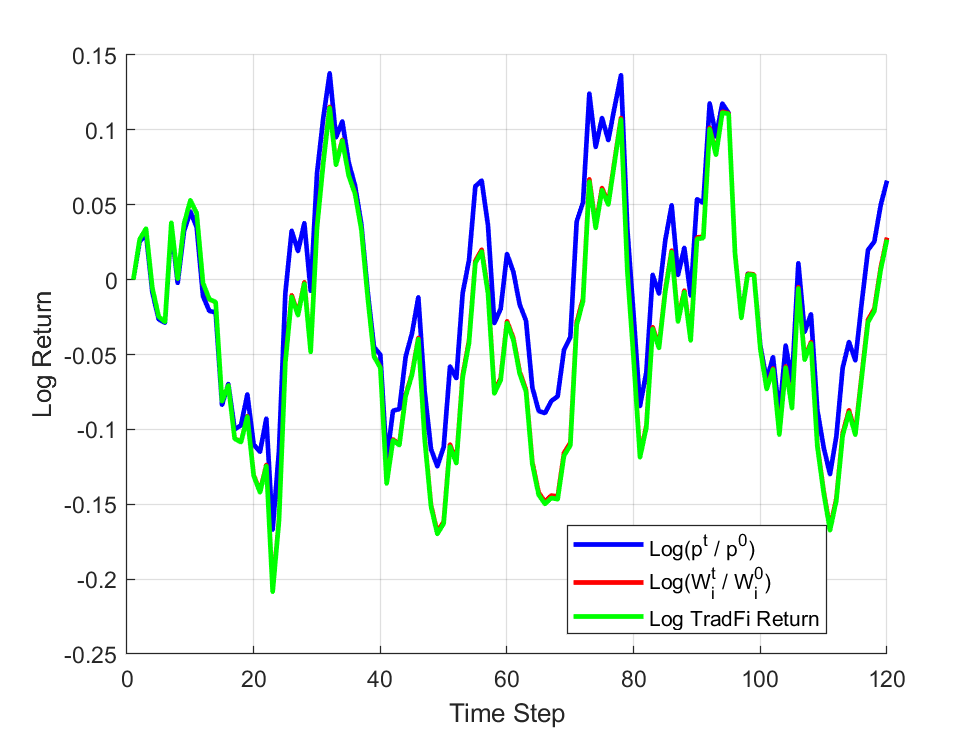

Figure 1: Time-series evolution in the unbounded accumulation regime, showing persistent price drift and the steady hand-off of token balances from investor to consumer, with stable yield.

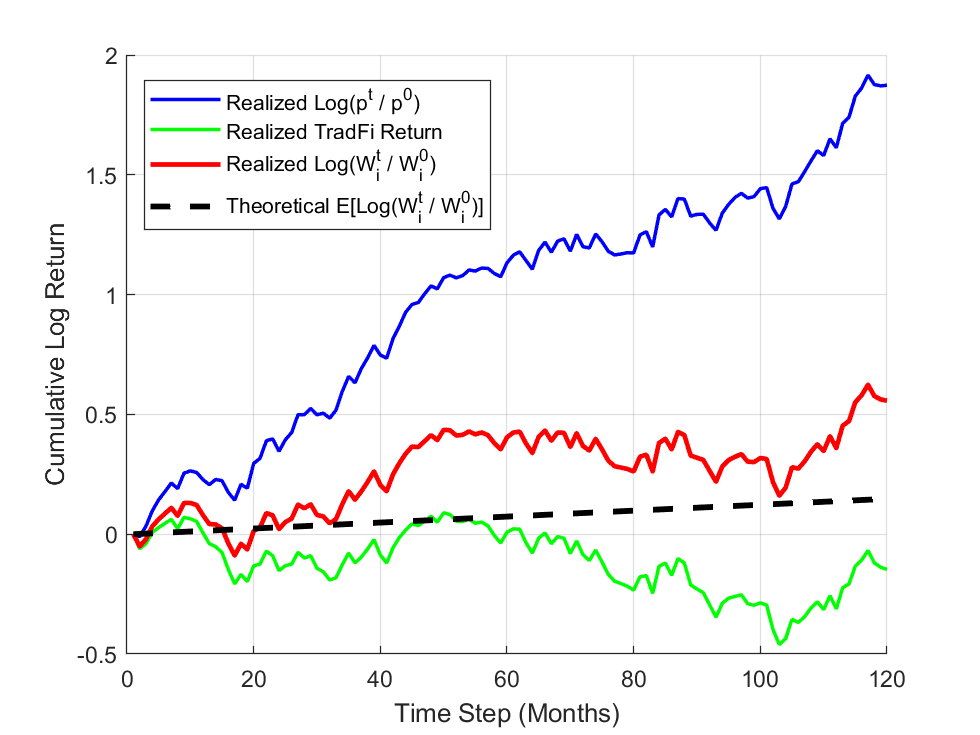

Figure 2: Uninterrupted structural returns for the investor across a decade, showcasing leveraged extraction from aggregated retail inflow.

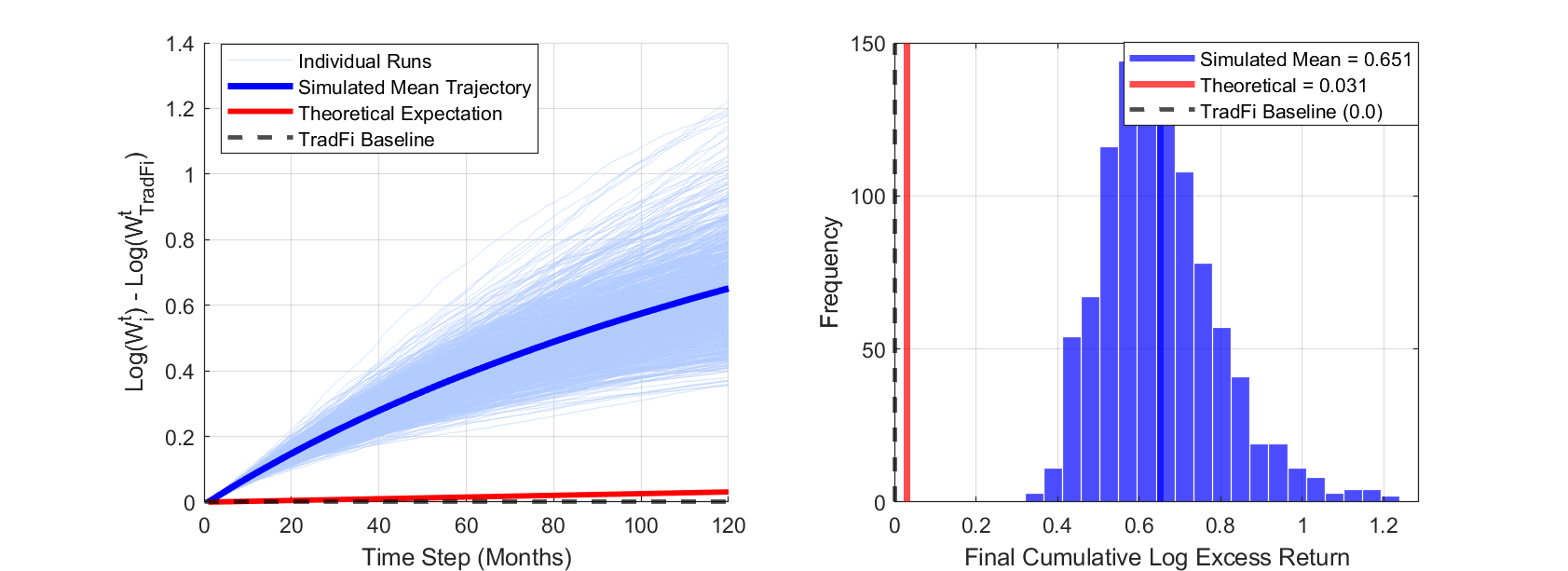

Numerical evidence confirms structural excess returns for the investor, with the mean log geometric excess return approximating 0.656 at 10 years—far exceeding the TradFi baseline. This outperformance is strictly attributable to leveraged capture of price-insensitive, utility-driven retail inflows, not native to the PoS protocol mechanics or algorithmic staking yield.

Figure 3: Monte Carlo analysis over 1,000 simulations, highlighting consistent investor outperformance (left) and the statistical concentration of excess returns at the final horizon (right).

Utility-Consumption Anchoring: Steady-State Tokenomics and Dissolution of Institutional Alpha

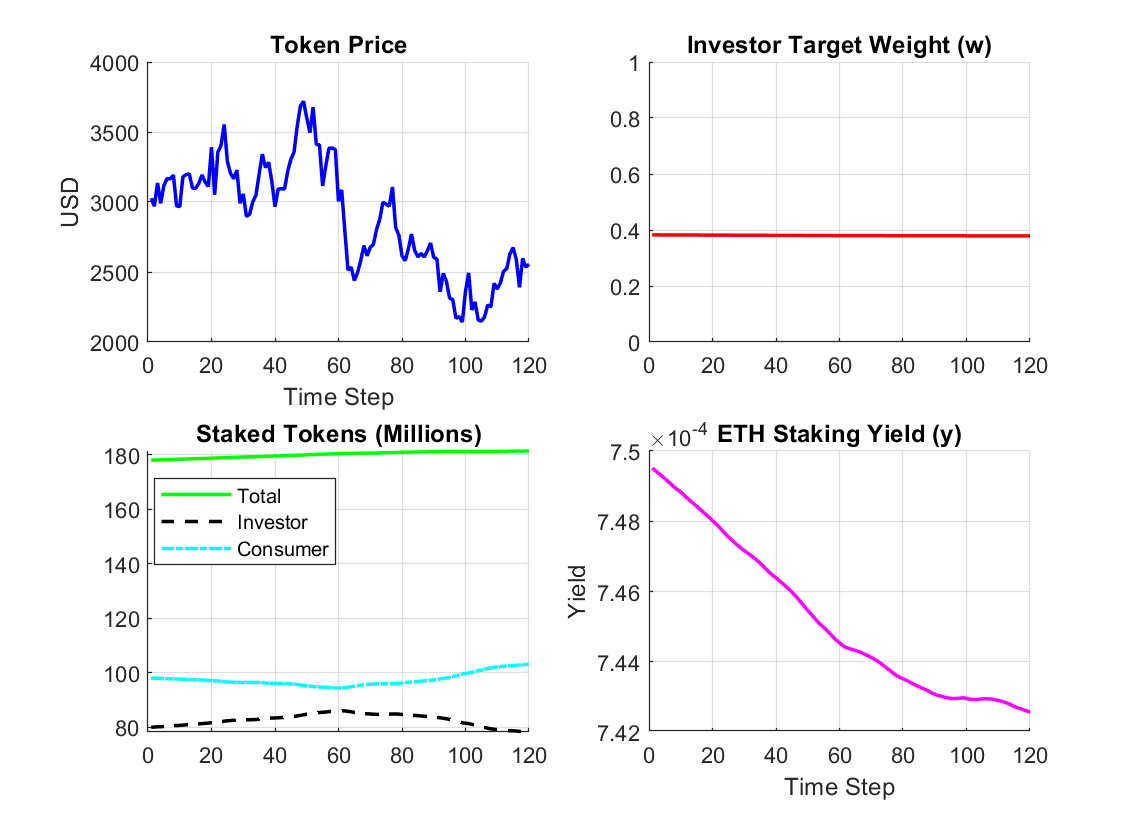

Transitioning to the utility-consumption regime, the model endogenizes two-way consumer flows. Retail agents now periodically liquidate a fraction of crypto allocations for fiat, dynamically adjusting according to the aggregate utility of real-world consumption versus network utility. The resulting equilibrium structure is mathematically tractable and admits an explicit steady-state solution for the price baseline, which scales linearly with network adoption (N) and core utility preference (γ).

The asset-clearing mechanism ensures that any exogenous price appreciation triggers profit-taking and selling, immediately suppressing further speculative drift. Powerfully, investor excess yield vanishes: the distribution of log excess returns is centered at zero, with no long-term arbitrage available, in stark contradiction to the unbounded accumulation case.

Figure 4: Steady-state regime with utility-driven buy/sell equilibrium, showcasing mean-reverting dynamics for price, yield, and token supply.

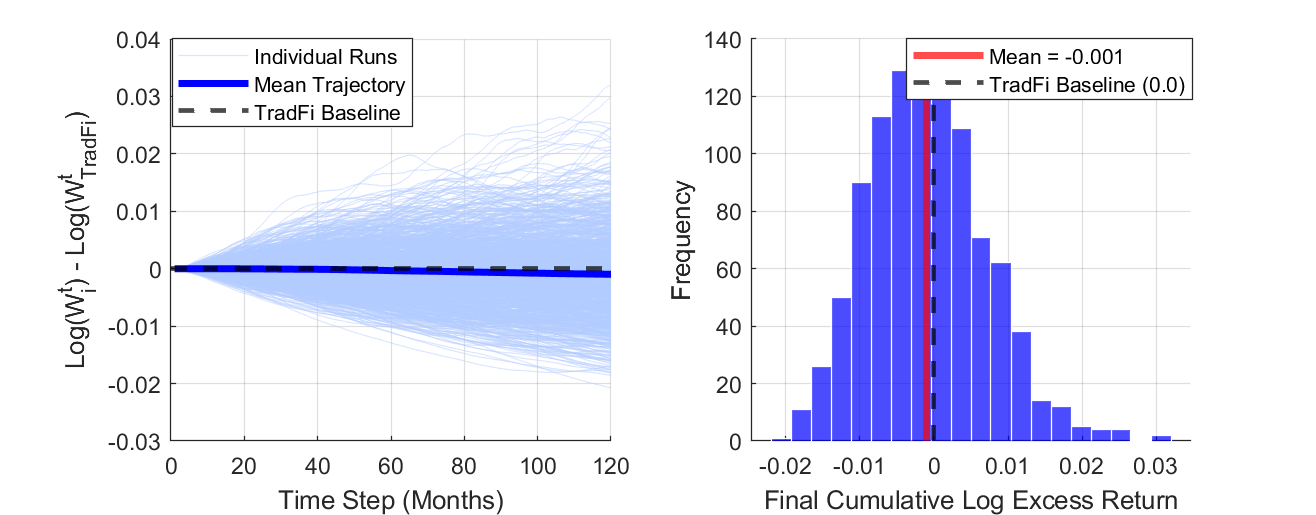

Figure 5: Sample path of returns, highlighting the absence of persistent drift or alpha and the role of macro shocks on investor performance.

Monte Carlo simulations validate the theoretical findings. Investor returns manifest as a symmetric distribution tightly clustered around zero (mean: -0.001 after 10 years), indicating no compensated risk for institutional participation. Volatility exposure is present, but systematic alpha extraction is not.

Figure 6: Distribution of investor log excess returns over 1,000 simulations, depicting zero mean premium and substantial cross-sectional volatility.

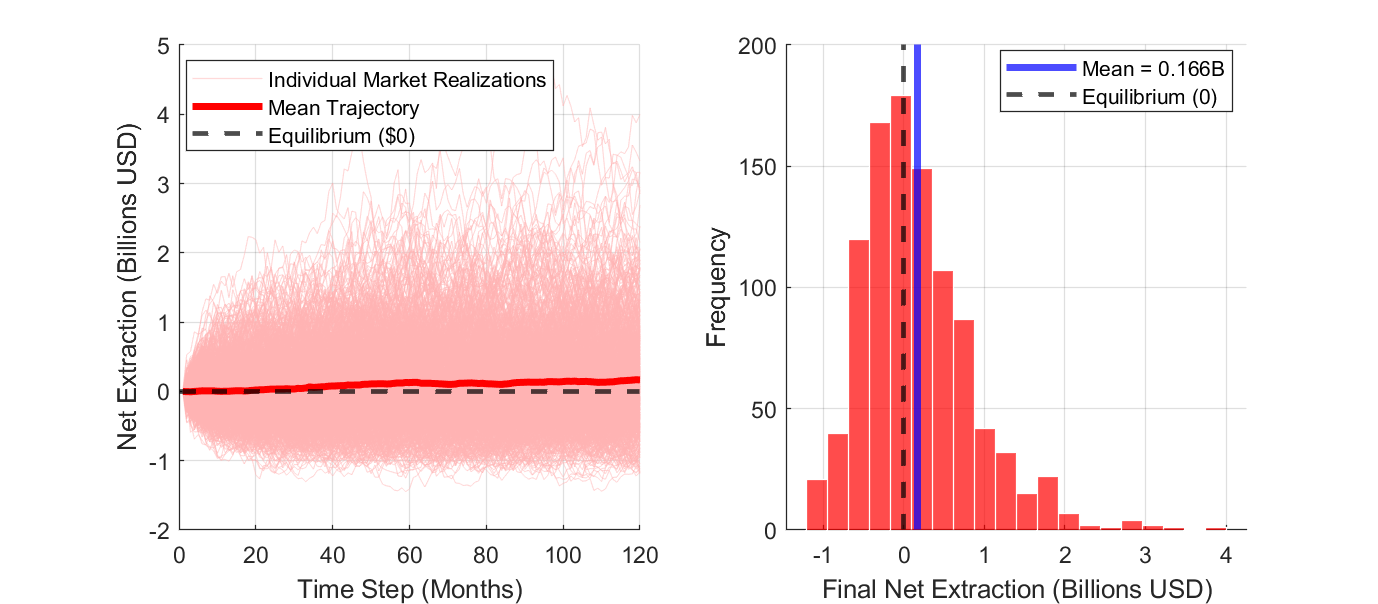

The retail consumer's real-world net extraction also remains tightly bounded around zero, with fluctuations solely due to asset price volatility, not structural drift. The network's cryptographic security threshold is robustly preserved, as retail counter-cyclical flows stabilize staked supply throughout market cycles.

Figure 7: Distribution of consumer net fiat extraction over 1,000 simulations, confirming steady-state anchoring and robust equilibrium stability.

Theoretical and Practical Implications

A central theoretical implication is the proof that structural institutional alpha in PoS networks is not intrinsic, but arises only in regimes where retail acts as an unintelligent, persistent buyer. Introduction of rational two-way retail optimization instantaneously dissolves all arbitrage opportunities, reducing institutional yield to the TradFi baseline. This finding directly contests prevalent narratives around staking as a risk-free or superior hedge for institutional allocators.

From a practical perspective, the study demonstrates that network inflation, yield, and baseline pricing are fundamentally governed by consumer adoption and transaction utility. Price volatility is imported from TradFi shocks, not from the structure of the PoS protocol itself. Network security is shown to be natively anti-monopolistic, as Kelly-optimal investors are compelled to reduce holdings in response to persistent retail inflows, and consumer feedback endogenously stabilizes the staked base near the protocol's cryptographic minimum.

Limitations and Future Directions

While the model incorporates modern transaction fee architectures (EIP-1559) and cross-market capital mobility, real-world complexity may involve additional agent heterogeneity, time-varying preferences, or exogenous shocks not directly modeled. Extensions may include agent-based simulations with expanded utility specifications, direct competition between multiple validator constituencies, and empirical calibration against realized market data for further validation of the asset pricing and security dynamics elucidated in this work.

Conclusion

This paper establishes a formal open-economy framework for evaluating token pricing, wealth distribution, and systemic security in PoS blockchains with EIP-1559. The results conclusively demonstrate that persistent investor alpha and speculative bubbles are emergent only under structurally one-sided consumer flows. In rational dynamic equilibria, PoS token value and staking returns anchor tightly to utility-driven baselines determined by network adoption parameters, with institutional excess returns eliminated and overall network security insulated from both financial shocks and capital concentration.

For researchers in crypto-finance and protocol economics, these findings underscore the necessity of incorporating realistic agent-based dynamics and behavioral heterogeneity into tokenomic and security analyses, particularly as institutional and retail capital flows become increasingly intertwined in next-generation blockchain ecosystems.

Reference: "Bubbles vs. Baselines: Token Valuation and Institutional Capital in PoS Networks under EIP-1559" (2606.07445)