- The paper demonstrates that tuning fractional differencing (d ≈ 0.4) preserves long memory, enabling improved forecasting accuracy.

- Methodologically, lag-based MLPs effectively exploit persistence in bond index series, while CNN-GAF models underperform due to information bottlenecks.

- The findings highlight that optimal preprocessing and series transformation are critical for robust one-step-ahead predictions in fixed-income markets.

Statistical Structure and Preprocessing of Bond Index Time Series

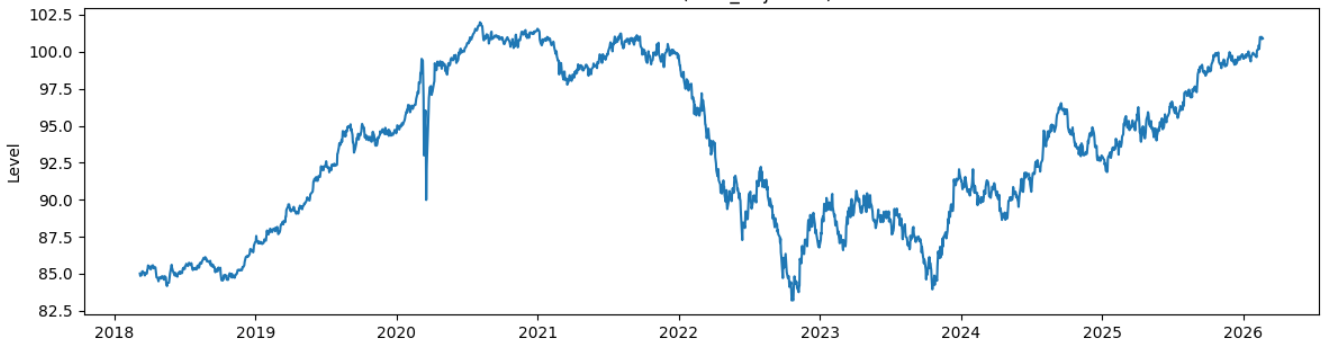

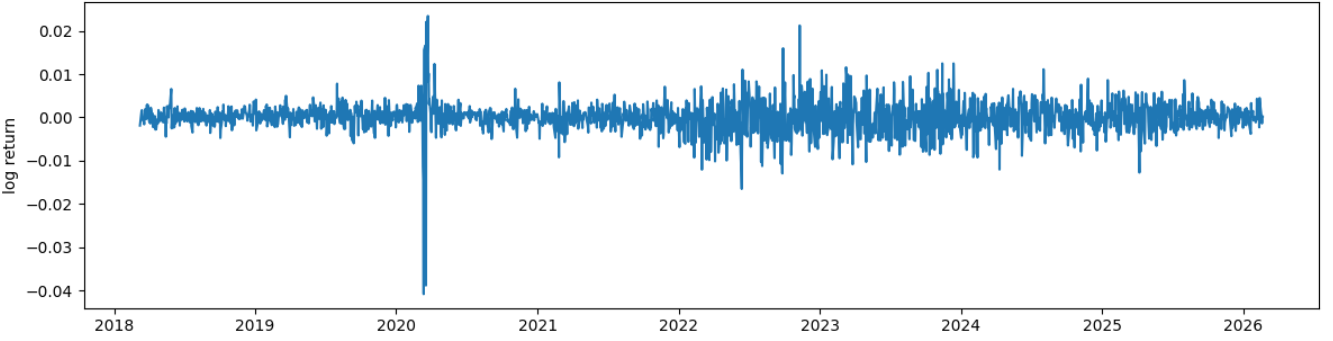

The paper systematically analyzes the daily time series properties of the U.S. Aggregate Bond Index from March 2018 to February 2026. Raw levels display near unit-root persistence, evidenced by autocorrelations near unity and ADF statistics failing to reject the null of integration order one (I(1)). In contrast, log returns are covariance-stationary (I(0)), with rapid mean reversion and volatility clustering, confirming classical financial time-series stylized facts. These statistical structures directly inform preprocessing strategy and set the stage for model selection and transformation approaches.

Figure 1: Daily closing levels of the U.S. Aggregate Bond Index, 2018–2026.

Figure 2: Daily log returns of the U.S. Aggregate Bond Index, 2018–2026.

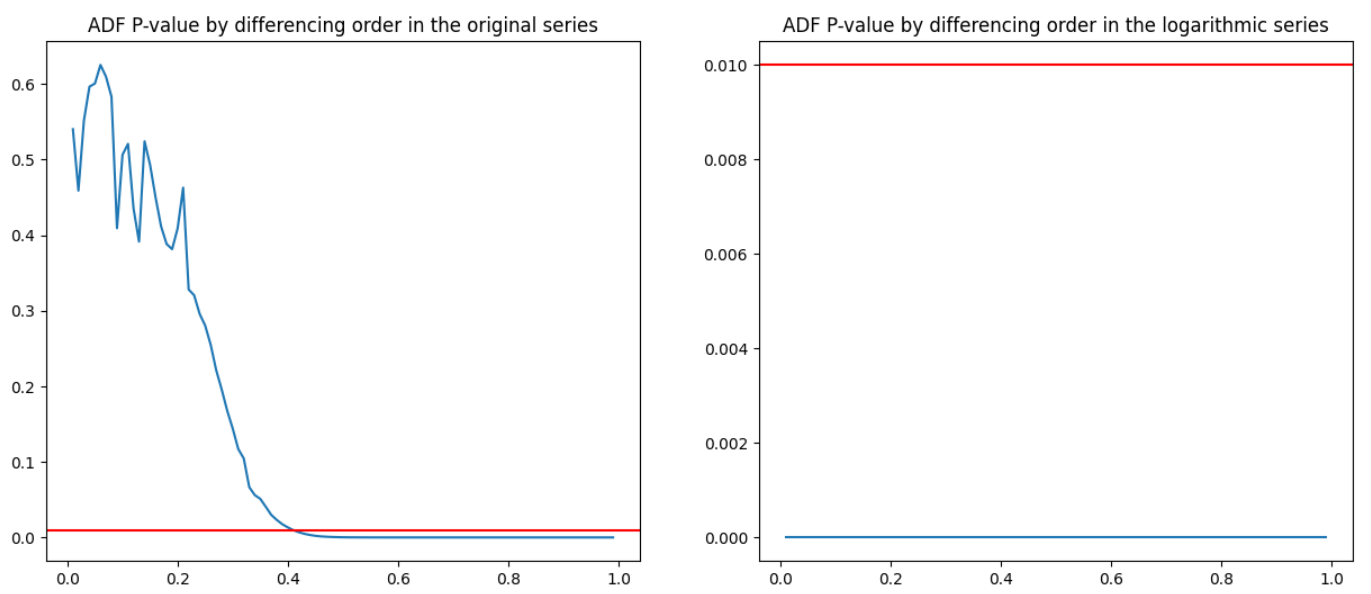

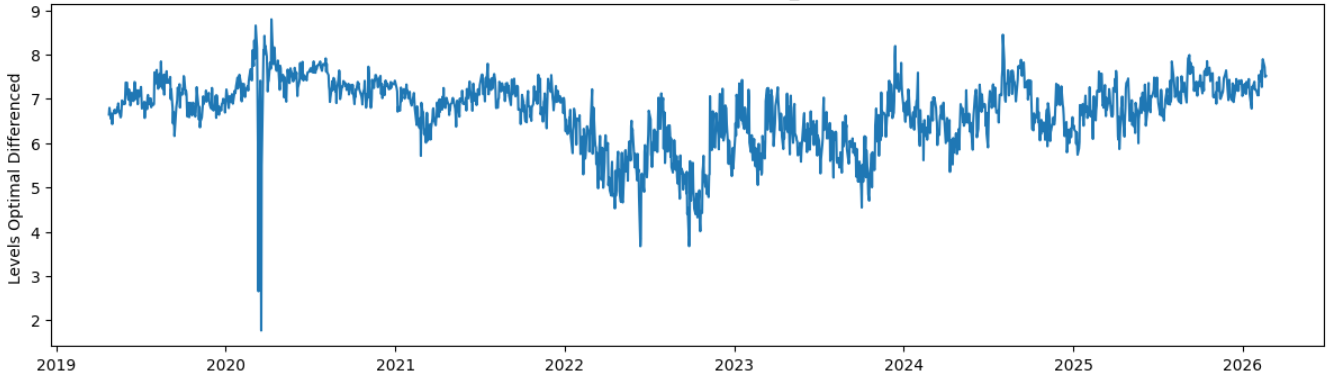

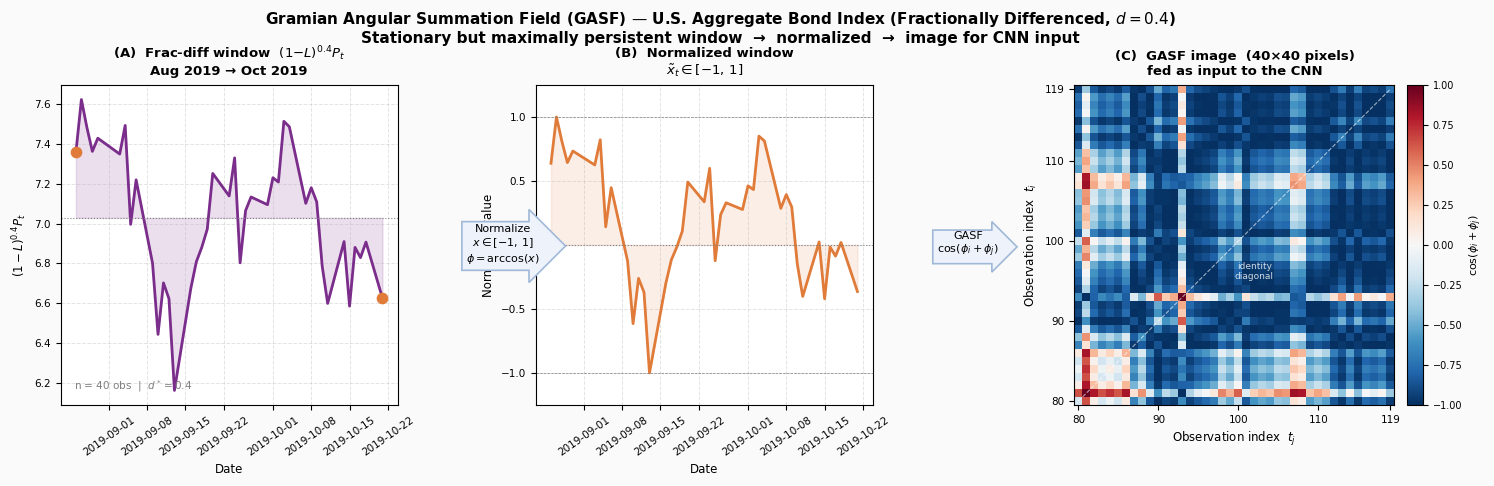

The study highlights the trade-off between full differencing (which risks destroying predictive low-frequency structure) and insufficient removal of stochastic drift. Employing the fractional differencing framework (Granger and Joyeux; Hosking), the authors select an optimal differencing parameter d∗≈0.4, guided via ADF p-value minimization following the L{ó}pez de Prado methodology. This yields a "stationary but maximally persistent" representation—retaining long memory while (nearly) fulfilling stationarity requirements.

Figure 3: ADF p-value as a function of differencing order d: d≈0.4 achieves minimal order needed for stationarity in the original-level series.

Figure 4: U.S. Aggregate Bond Index after fractional differencing at d=0.4: stochastic trend attenuated but persistent swings remain.

Forecasting is posed as a one-step-ahead regression problem with lagged embeddings. Comprehensive hyperparameter tuning is applied for MLP architectures, including joint search over lag length, hidden layers, units, regularization, and learning rate. Temporal train/test splits ensure causal integrity.

Empirical results demonstrate:

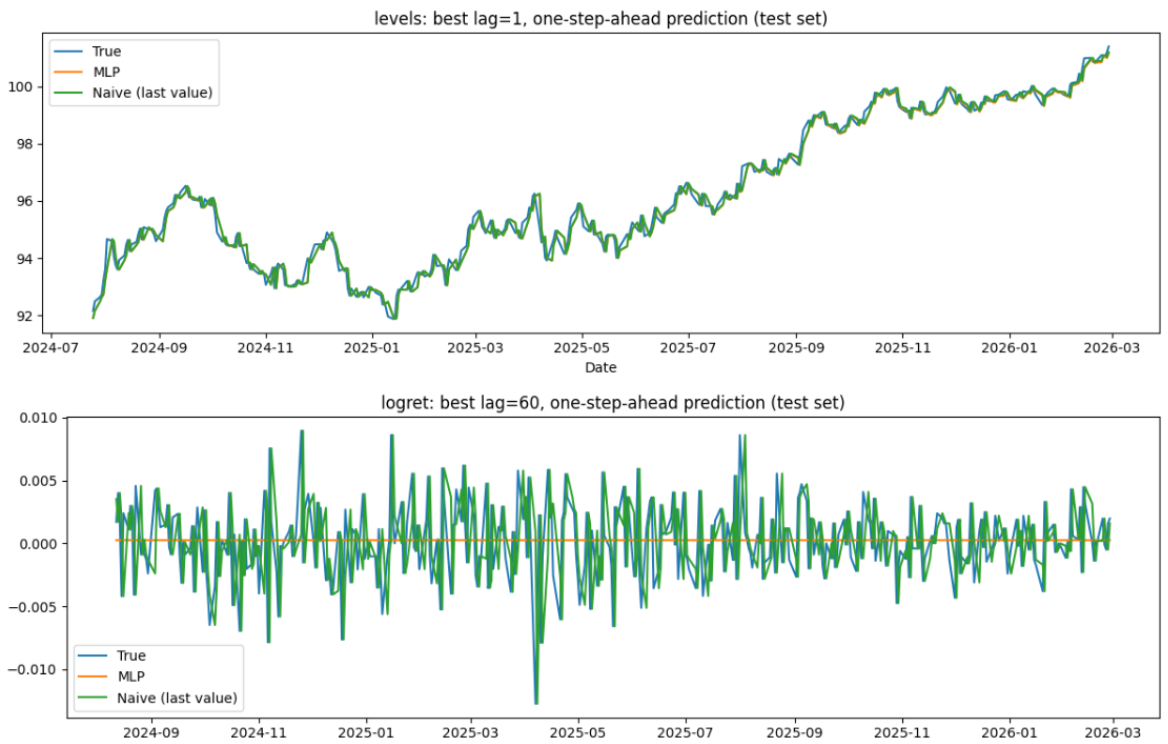

- Levels (I(1)): The MLP reduces to a near-identity last-value predictor with L=1, matching the naive baseline and yielding near-optimal R2 (I(0)0). The predictable variation is almost entirely due to persistence, and model complexity confers no measurable advantage.

- Log Returns (I(0)1): Despite a longer optimal lag window, the MLP collapses to a mean predictor (I(0)2), reflecting lack of exploitable autocorrelation and aligning with weak-form efficiency.

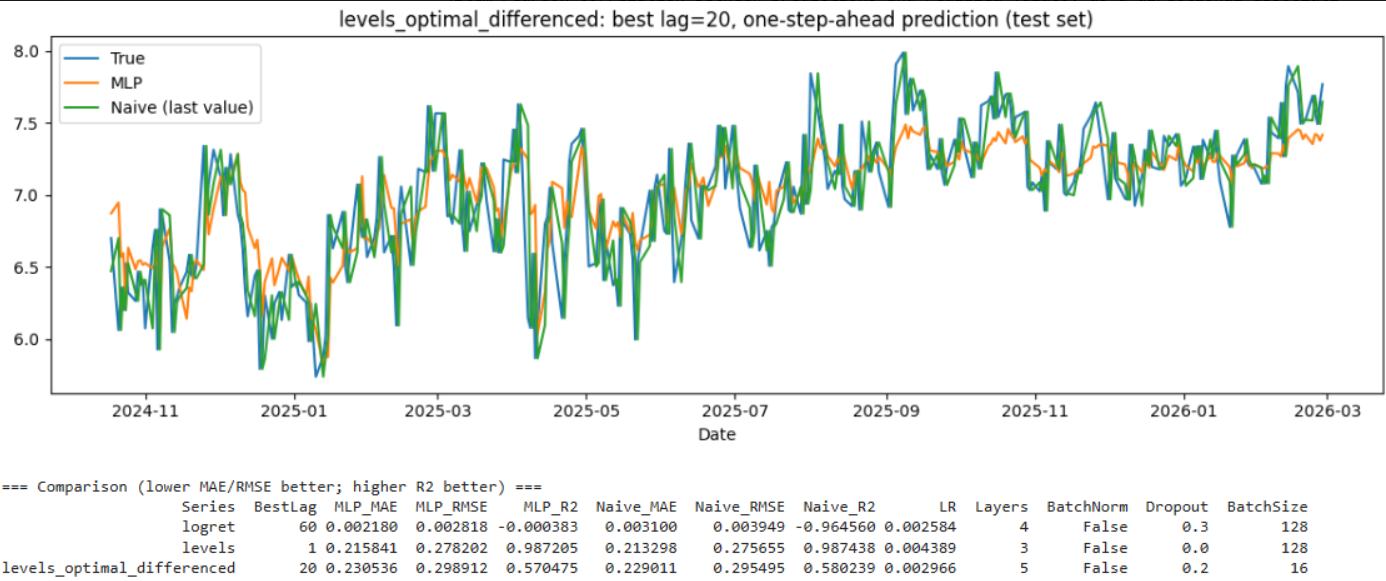

- Frac. Diff. (I(0)3): MLP achieves meaningful incremental performance (I(0)4), capitalizing on preserved long-memory; smoothing and lag-based structure are exploited.

Figure 5: Test-segment forecast trajectories for levels and log-returns: MLP tracks the naive benchmark for levels; both models nearly flat for returns.

Figure 6: Forecast on fractionally differenced series (I(0)5): MLP outperforms naive baseline where moderate dependence remains.

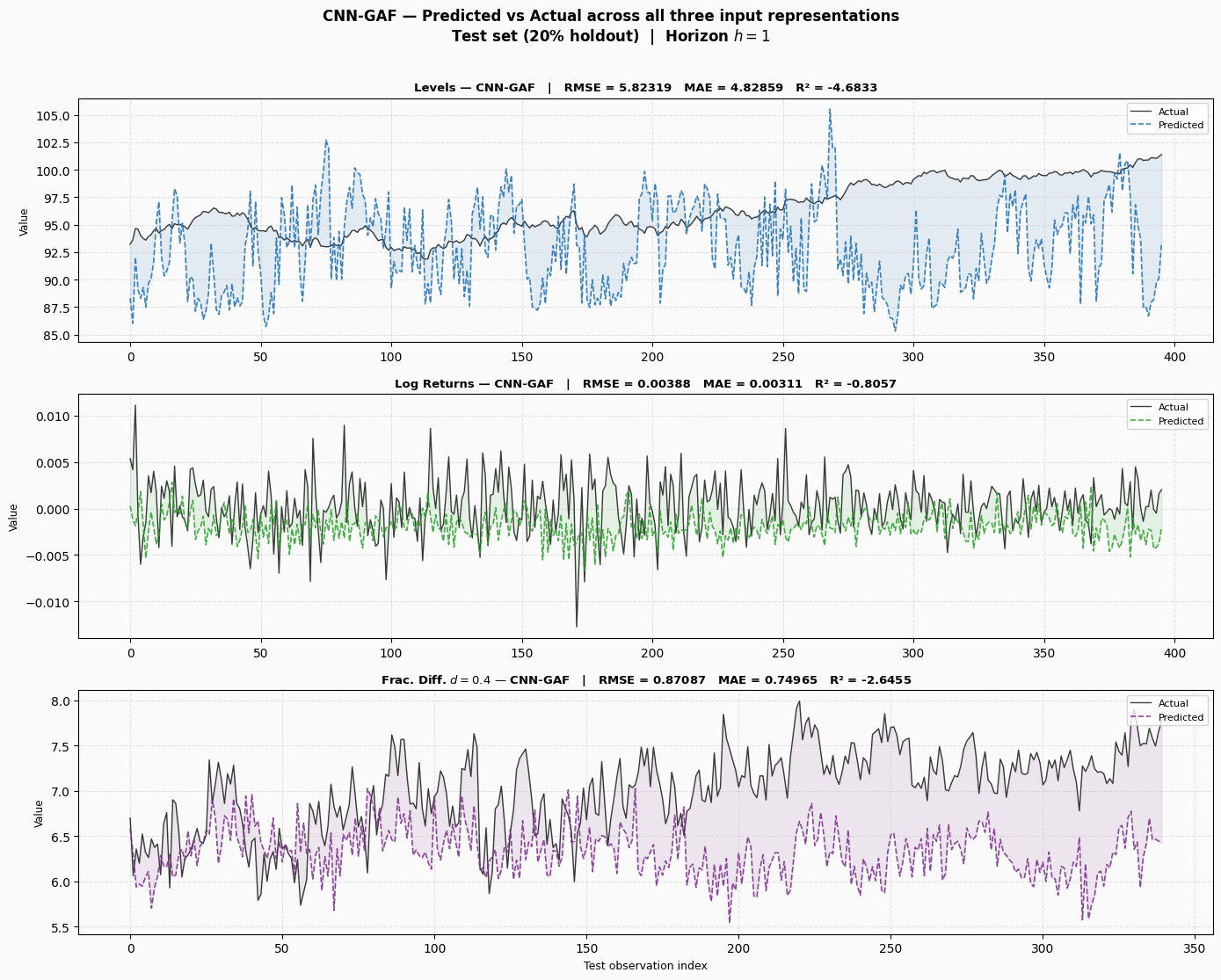

CNN-GAF Pipeline: Image Encoding, Model Fit, and Generalization

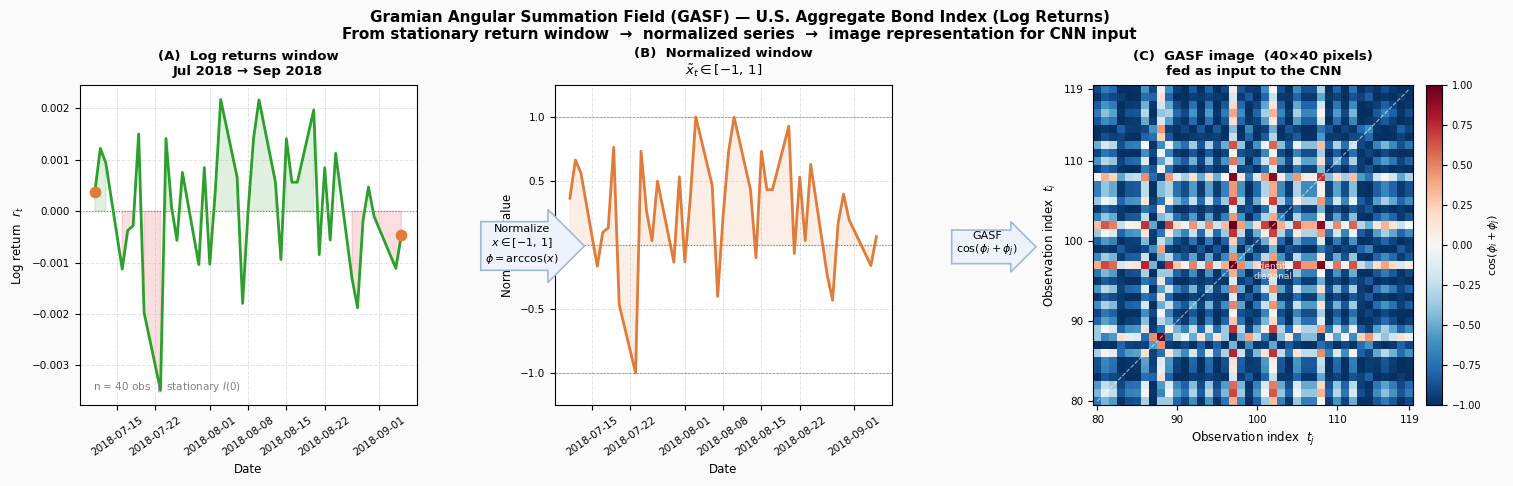

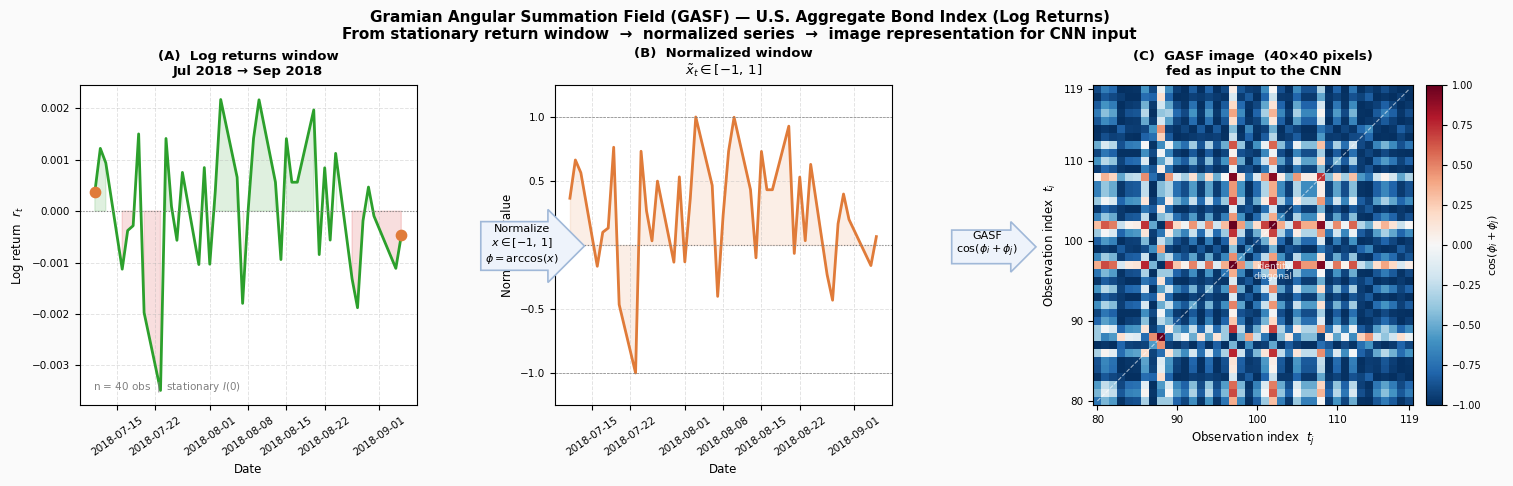

The study evaluates convolutional models trained on Gramian Angular Field (GAF) images derived from sliding windows of the time series. The GAF transformation encodes temporal relationships as image structure, aiming to facilitate pattern-based prediction.

Figure 7: GAF encoding pipeline and resulting image for original-level series.

Figure 8: GAF encoding pipeline and image for log-return series.

Figure 9: GAF encoding pipeline for fractionally differenced series (I(0)6).

Out-of-sample evaluation reveals uniformly negative I(0)7 for CNN-GAF models across all input transformations:

The results substantiate that the efficacy of forecasting architectures is fundamentally governed by the statistical structure of the series and the alignment of input representation with inductive bias:

- Lag-based MLPs exploit persistence directly, aligning with time series where the prior lag is sufficient statistic.

- CNN-GAF approaches are potent for pattern-based or regime classification tasks but misaligned with persistence-driven dynamics and suffer from information bottlenecks in short windows.

The study makes a contradictory claim relative to much contemporary literature: architectural complexity and geometric encoding (e.g., CNNs with GAF) do not confer advantage in classical financial series forecasting unless the transformation enhances the signal-to-noise ratio and matches the forecasting task's requirements.

Practical and Theoretical Implications

For practitioners, the primary determinants of forecast performance are choice of preprocessing and series transformation, rather than model sophistication. In fixed-income time series with pronounced persistence or weak-form informational efficiency, lag-based architectures are competitive and frequently optimal. Theoretical implications suggest that sophisticated deep learning pipelines—unless explicitly designed for the statistical structure—are prone to underperform naïve or classical approaches. Further, fractional differencing offers a nuanced trade-off: by carefully calibrating d∗≈0.41, one can balance stationarity with retention of economically relevant memory, enhancing downstream model utility.

Future developments may explore the inclusion of cross-sectional asset signals, macroeconomic features, alternative architectures (LSTM, Transformer), or extend the task to regime detection or long-horizon prediction, potentially providing scenarios where pattern-based (CNN/GAF) approaches are better aligned and performant.

Conclusion

The study rigorously demonstrates that predictive modeling for the U.S. Aggregate Bond Index is governed by the transformation and statistical structure of the series, not by architectural complexity. Lag-based MLPs on appropriately transformed series yield reliable short-horizon forecasts, while CNN-GAF pipelines underperform in persistence-dominated settings. Series transformation—particularly fractional differencing—serves as an optimal compromise, enabling stationarity with preserved memory. These findings direct future research to prioritize alignment of series properties and model inductive bias, challenging prevailing assumptions about the universal superiority of deep image-based architectures for financial forecasting (2605.27977).