- The paper develops a unified pricing and hedging framework incorporating jump-diffusion dynamics and counterparty default risks to evaluate EPS contracts.

- It derives closed-form valuation formulas and effective static hedging strategies, highlighting significant impacts of crisis events and default adjustments.

- Numerical experiments confirm that properly priced default adjustments and super-hedging premiums are crucial for accurate risk management in incomplete markets.

Valuation and Hedging of Variable Annuities with Equity Protection Swaps under Jumps and Default Risks

Introduction and Problem Statement

This work rigorously investigates the valuation and hedging of Equity Protection Swap (EPS) contracts, a flexible class of insurance derivatives targeting retirement portfolios. EPS contracts are not variable annuities (VAs) per se, but attach to existing equity exposures to mitigate tail risks, such as those arising during market crises. The core innovation is the integration of both sudden asset price jumps—as stylized proxies for crisis events—and third-party counterparty default risks into a unified pricing and hedging framework.

A salient feature of real-world EPS programs is the non-negligible delay between premium quotation and effective hedge construction by providers, introducing basis risk in volatile markets. The paper systematically models these frictions, analyzes incomplete-markets impacts, and gives explicit valuation kernels across several structural scenarios, focusing on key EPS contract forms (buffer, floor, and floor-cap).

Structural Models and Analytical Framework

Jump-Diffusion Dynamics

A central modeling device is Merton’s jump-diffusion process. The risky asset St evolves through a stochastic differential equation:

dSt=μSt−dt+σSt−dWt+St−dJt,

where Wt is Brownian motion and Jt is a compound Poisson process with jump sizes Yi∼N(α,δ2) and jump intensity λ. Under risk-neutral measure, the drift is adjusted by the compensator μJ to satisfy no-arbitrage requirements. Jumps—primarily calibrated as negative—represent rare, severe market dislocations (e.g., crashes).

Counterparty Default: Random Time Hazard

Default risk is introduced via an independent hazard process context (Szimayer’s random time model). The default event occurs at a stochastic time τ, modeled as the first event in a Cox process with intensity γP. This is external to the filtration of S, rendering the default probabilistically independent of asset trajectories (a plausible, if not exhaustive, stylization for certain structured derivative books).

EPS Payoff Structures

Under a unified notation, the terminal EPS provider cashflow, normalized to unit notional, is dSt=μSt−dt+σSt−dWt+St−dJt,0. dSt=μSt−dt+σSt−dWt+St−dJt,1 is a continuous, non-decreasing, piecewise-linear map of the portfolio return dSt=μSt−dt+σSt−dWt+St−dJt,2. Three families of contracts receive detailed focus:

- Buffer EPS: Offers loss protection below a buffer dSt=μSt−dt+σSt−dWt+St−dJt,3 and returns participation fee for gains above dSt=μSt−dt+σSt−dWt+St−dJt,4.

- Floor EPS: Ensures payouts for dSt=μSt−dt+σSt−dWt+St−dJt,5, with gains shared above dSt=μSt−dt+σSt−dWt+St−dJt,6.

- Floor-Cap EPS: Imposes both a floor and cap, bounding losses and gains.

Closed-form European-style option pricing equations are derived under both the jump-diffusion and random time default settings.

Jump-Diffusion Options

European option values become infinite weighted mixtures of shifted Black-Scholes prices:

dSt=μSt−dt+σSt−dWt+St−dJt,7

For dSt=μSt−dt+σSt−dWt+St−dJt,8, the above integrates to a closed convolution using normal summations.

Put-call parity is shown to be modified: in jump-diffusion, the difference of call and put prices reflects the drift induced by the compensated jump process and is no longer simply the present value of forward minus strike.

Default-Adjusted Valuation

When independent default is incorporated, the present value of a claim dSt=μSt−dt+σSt−dWt+St−dJt,9 under risk-neutral measure is

Wt0

i.e., risk-neutral discounting adjusts for default with an augmented exponential term determined by the hazard intensity.

Hedging and Incompleteness

Static Hedging under No-Default

Following [Xu et al. 2024], the EPS can be statically replicated by a portfolio of vanilla puts (for the protection leg) and (short) calls (for the fee leg):

Wt1

The initial premium Wt2 is set so that the provider’s discounted end-of-period cashflow is zero-mean under the risk-neutral measure.

Impact of Counterparty Default

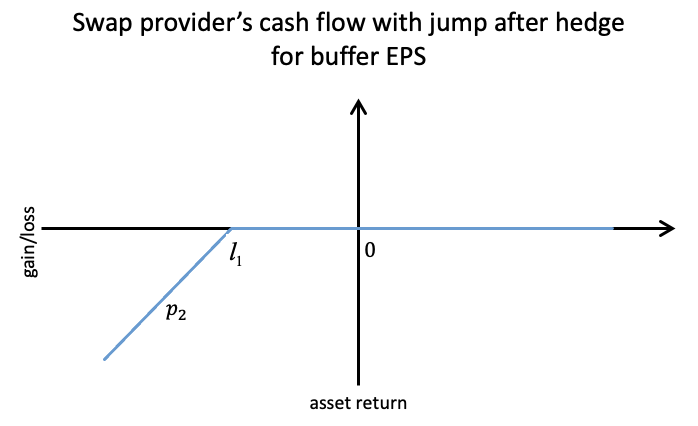

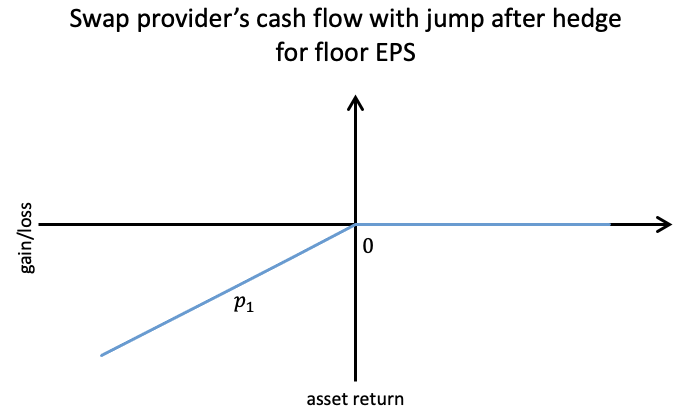

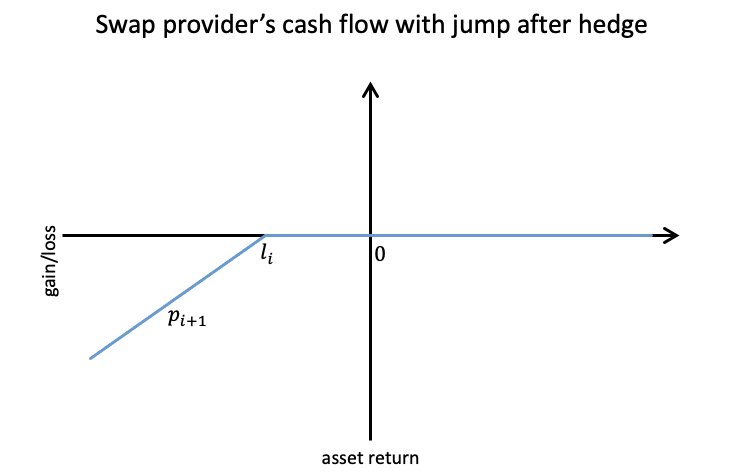

If only the third party (e.g., the long put counterparty) can default, static replication fails. Provider loss after hedge is no longer eliminated but becomes a function of realized negative tails in Wt3 and the participation rate of the first loss leg (for buffer/floor structures).

The default-adjusted initial premium is derived as

Wt4

where DA is the expected (default probability × loss severity), with closed expressions under both Black-Scholes and jump-diffusion settings.

Figure 1: Examples of Swap provider's cash flow after hedge when only third party default.

Numerical studies confirm that default risk leads to strictly negative expected cash flows for providers unless default adjustment is priced in.

Figure 2: EPS provider's general cash flow after hedge when only third party default.

Numerical Results

Option and Hedging Portfolio Valuations

Comprehensive scenario analysis is performed:

- As jump mean Wt5 becomes more negative (large crises), put prices and EPS provider risk rise.

- Increasing jump intensity Wt6 (all else equal) magnifies hedging costs and default risk sensitivity.

- Under the jump-diffusion model with several possible jumps, the hedging cost remains close to the vanilla Black-Scholes value, so long as default is not considered. For exactly one jump (catastrophic event), required premiums spike sharply.

- Default intensity (Wt7 for counterparty) is, as expected, a strong determinant of required premiums; these must materially exceed naive static replication costs even for moderately large default probabilities.

Default Adjustment and Super-Replication

The analysis demonstrates that in the absence of a complete hedge, adding an exact expectation of provider’s residual loss produces a “default-adjusted” fair premium. For conservative providers, a “super-hedge” premium is offered, based on maximum possible post-hedge loss (full asset wipe-out). For realistic default intensities (Wt8 p.a.), such adjustments can represent significant basis points per unit notional, becoming economically meaningful for large notional flows.

Implications and Prospects

From a risk management perspective, the work establishes that:

- Practical pricing of EPS-type contracts in incomplete markets—especially with counterparty and crisis risk—is not possible with naive Black-Scholes replication; jump and credit risk premia are essential.

- Closed-form formulas facilitate stress-testing across a range of realistic portfolio parameters and can be used for real-time margining, product design, and sensitivity analysis.

- The observed resilience of “several-jump” risk-neutral pricing for EPS under Merton dynamics (relative to Black-Scholes) justifies the use of jump models for robust, market-consistent EPS design.

- Numerical experiments highlight that static portfolios may substantially undercompensate insurer risk if default risk is neglected—prompting regulatory and actuarial require ments for explicit capital buffers or super-hedging.

Theoretically, the work clarifies for this derivative class the interplay/limits of static hedging, market incompleteness, and the necessity of scenario-based valuation when event risks (systemic jumps, default) are relevant.

Future Directions

Open research directions include: modeling joint/informationally linked jump-default events (systemic risk), American-style EPS features (early exercise), and the impact of stochastic volatility or alternative Lévy jump structures. Extending explicit valuation and default adjustment results to path-dependent payoffs or longer-term multi-period contracts aligns with current industry re/insurance product trends. Integration with market-consistent models for real-time superannuation fund risk management and regulatory capital calculations is an immediate real-world application.

Conclusion

This manuscript delivers a comprehensive analytical and numerical framework for EPS valuation and hedging under realistic asset and counterparty risk, advancing the actuarial and quantitative finance literature on retirement income products. The analytical tractability of the presented models, combined with their ability to integrate non-negligible event and default risk, make the results directly applicable for practitioners designing market-participation insurance derivatives in incomplete markets.