- The paper proposes a novel control-function approach to jointly identify quantile coefficients, measurement error distribution, and copula parameters.

- It employs a two-step sieve maximum likelihood estimator that achieves significant bias reduction and reliable bootstrap inference under endogenous conditions.

- Monte Carlo simulations demonstrate that the 2SSMLE markedly outperforms standard estimators, especially under high endogeneity and non-Gaussian measurement errors.

Endogenous Quantile Regression with Measurement Error in Dependent Variable

The paper "Endogenous Quantile Regression with Measurement Error in Dependent Variable" (2605.20601) addresses the bias arising in quantile regression (QR) when the regressor is endogenous and the dependent variable is subject to additive measurement error (EIV). Standard QR estimators are non-robust to these complications, with measurement error causing substantial bias in nonlinear models—contradicting classical results for linear regression. The analysis extends beyond existing work (e.g., Hausman et al.) by removing conditional independence between regressors and unobserved heterogeneity, which is typical when endogenous treatment selection is driven by equilibrium and omitted heterogeneity.

The identification challenge is addressed via a control-function approach within a triangular system, using instruments to construct a continuous control variable that restores conditional independence between the endogenous regressor and latent rank. Critically, the dependence between unobservable heterogeneity and the control function is nonparametrically modeled through a copula with uniform margins. The main nonparametric identification theorem shows that, under mild regularity and support conditions, the conditional quantile coefficient function, the measurement error distribution, and the copula are jointly identified from the observed conditional distribution.

Estimation Methodology: Two-Step Sieve ML

Building on constructive identification, the estimation is conducted via a two-stage sieve maximum likelihood estimator (2SSMLE). The first stage estimates the control variable either parametrically (e.g., OLS with known first-stage distribution) or nonparametrically (e.g., series approximation of FX1∣Z). The second stage implements sieve MLE for the quantile coefficient function, flexibly modeling nuisance distributions of the measurement error and copula. The integration of the control variable into the second-stage likelihood uses copula weights, facilitating inference on conditional quantile treatment effects.

With sieve spaces defined by monotonic spline basis and parametric families for the measurement error and copula, the estimator achieves consistency and asymptotic normality. Its convergence rate is governed by the minimum eigenvalue of the information matrix, reflecting the degree of ill-posedness. The first-stage error propagates into the second-stage variance, and, with mild undersmoothing conditions, bootstrap inference remains valid.

Asymptotic Theory and Bootstrap Inference

The estimator's asymptotic properties are rigorously established under both parametric and nonparametric first stage. The convergence rate for the quantile coefficient function is Op(Jn2λ/(λ+1)n−1/2(λ+1)), with Jn as sieve dimension and λ as smoothness order (cf. ordinary vs supersmooth error distributions). The estimator is (nκJn)−1/2-consistent, where κJn captures ill-posedness. Asymptotic normality is demonstrated for all component parameters—including finite-dimensional nuisance parameters—with variance decomposing into contributions from both estimation steps. The practical implication is that the second stage dominates the convergence rate and variance structure, though first-stage errors are non-negligible.

Pointwise bootstrap confidence intervals are recommended for inference, accounting for both stages' estimation uncertainty. Bootstrap validity for coverage of quantile coefficients and distributional parameters is established formally.

Monte Carlo Results

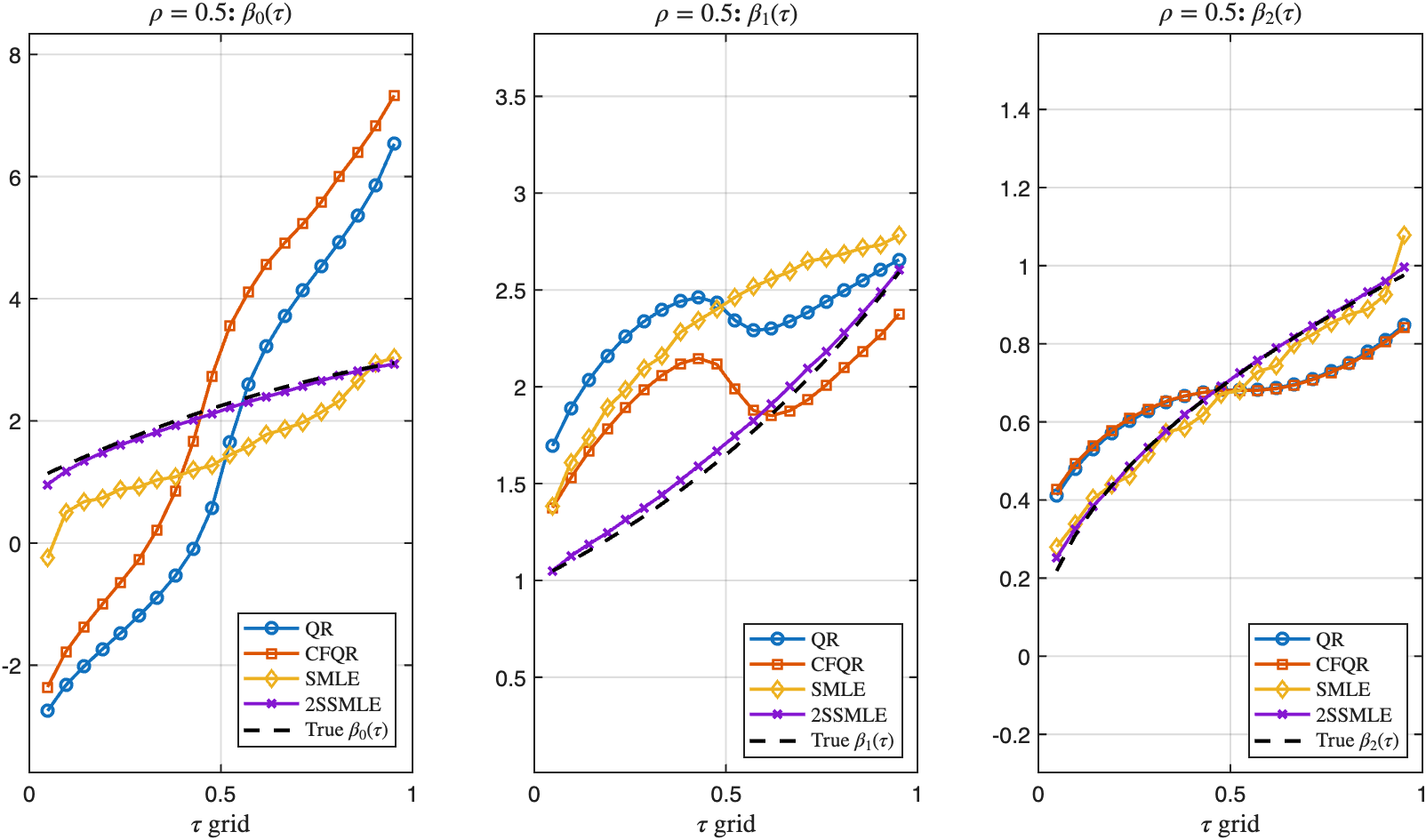

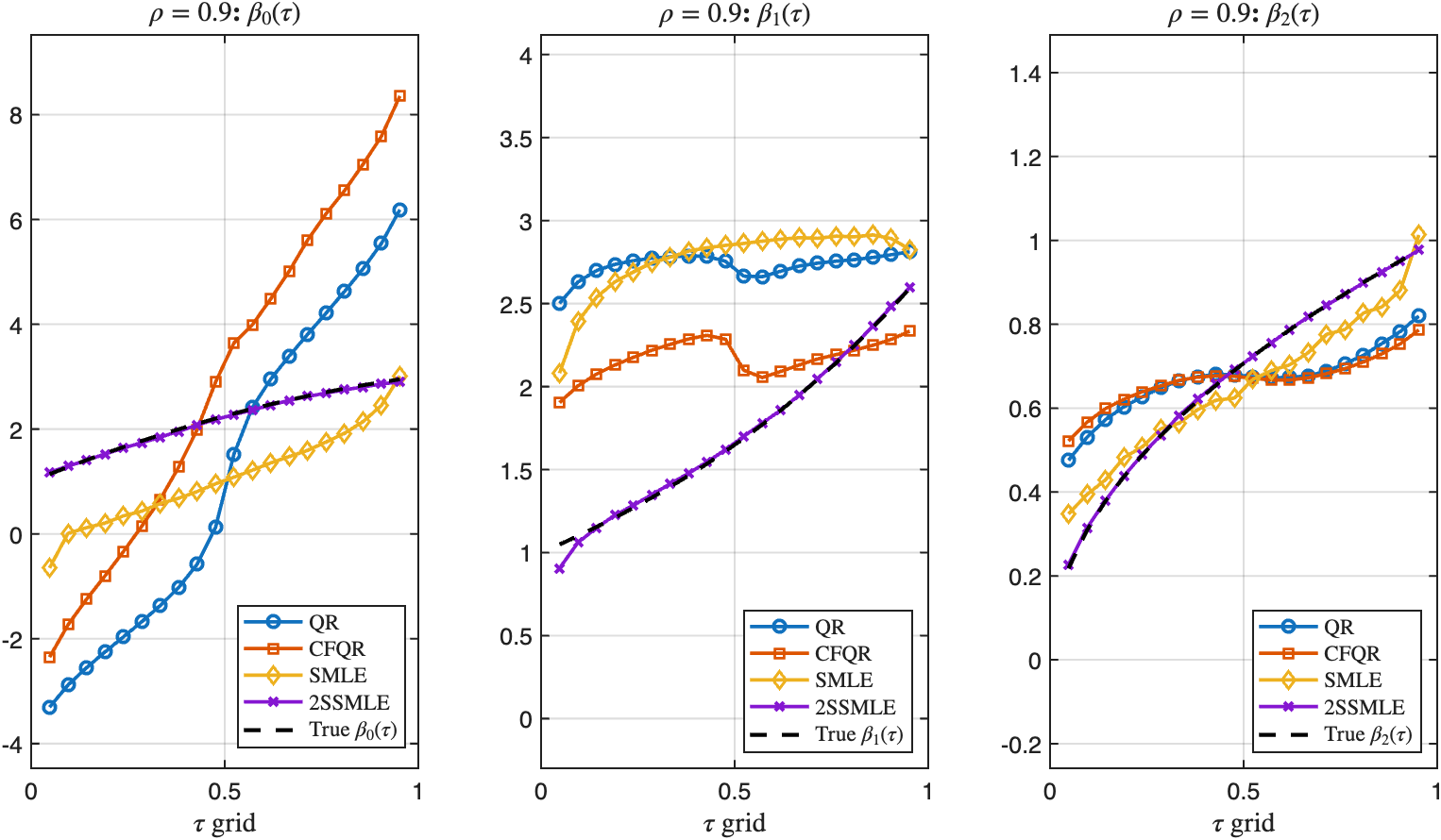

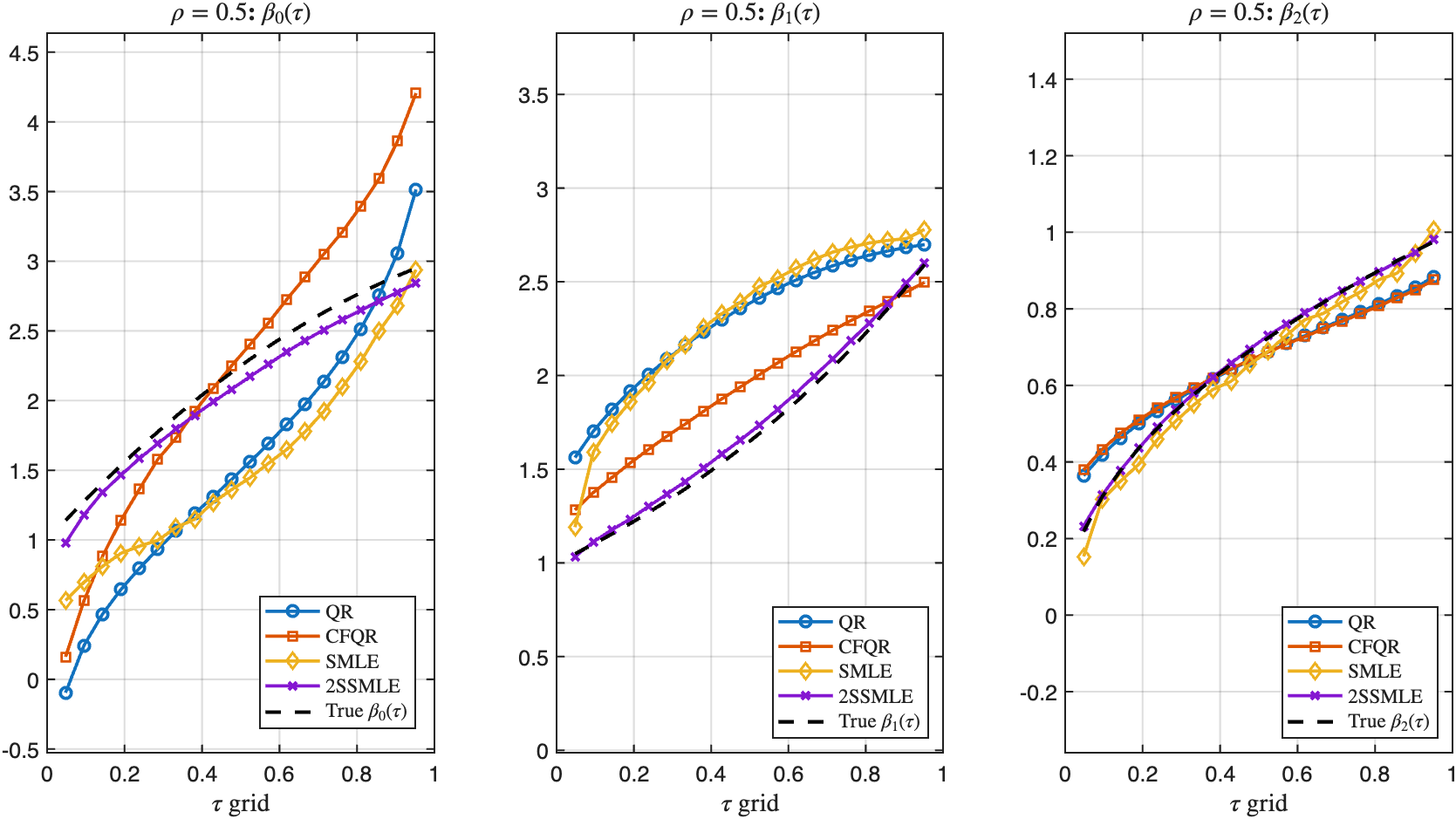

Monte Carlo simulations demonstrate the substantial bias in conventional QR when both endogeneity and measurement error are present, and quantify the efficacy of the proposed correction. Bias patterns are visualized across quantiles for four estimators: QR, control-function QR, sieve MLE (measurement error only), and the full 2SSMLE.

Figure 1: MC Results Comparison (ε∼3N): 2SSMLE outperforms baseline and partial estimators, especially in recovering the correct quantile coefficients across the spectrum.

Empirical results reveal that 2SSMLE reduces average absolute bias in the slope quantile coefficient (e.g., β1) to 4% of the true value, compared to 43% for standard QR, Op(Jn2λ/(λ+1)n−1/2(λ+1))0 for control-function QR, and Op(Jn2λ/(λ+1)n−1/2(λ+1))1 for sieve MLE. The estimator tracks the true coefficient functions uniformly across quantiles, including non-endogenous covariates (where bias is solely due to measurement error).

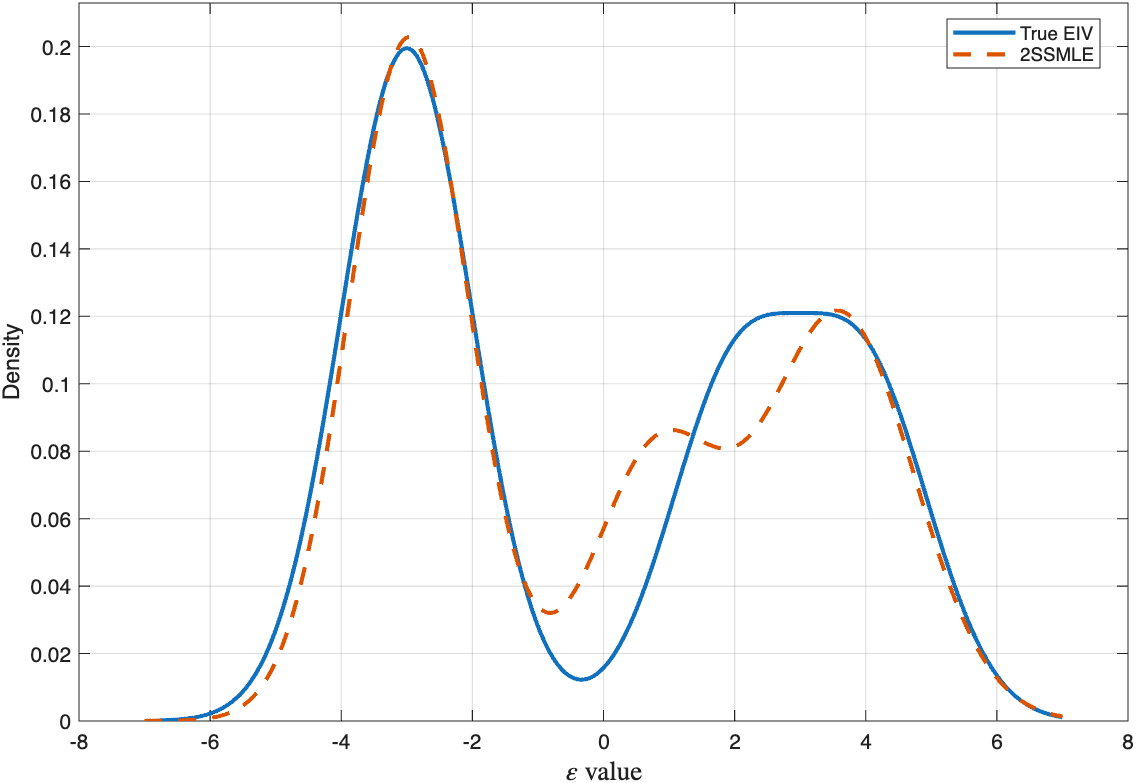

Figure 2: MC Results for 2SSMLE estimating the measurement error density (Op(Jn2λ/(λ+1)n−1/2(λ+1))2): estimator closely tracks the underlying distribution used in simulation.

The impact of bias worsens as copula endogeneity increases. Under severe endogeneity (Op(Jn2λ/(λ+1)n−1/2(λ+1))3), deviation from truth becomes significant for both QR and sieve MLE, while 2SSMLE preserves robustness. When measurement error is Gaussian and moderate, bias is less prominent, consistent with the theoretical predictions for error convolution. The estimator remains effective even when the true measurement error distribution is misspecified (e.g., Student-Op(Jn2λ/(λ+1)n−1/2(λ+1))4 or Laplace), with robustness established through mixture flexibility.

Figure 3: Comparison under high endogeneity (Op(Jn2λ/(λ+1)n−1/2(λ+1))5): 2SSMLE is robust while baseline estimators exhibit pronounced bias.

Figure 4: Comparison under normal measurement error: bias is less pronounced, but endogeneity remains impactful.

Bootstrap results indicate coverage for quantile coefficients is consistently near nominal levels (Op(Jn2λ/(λ+1)n−1/2(λ+1))6) regardless of whether the control variable is estimated parametrically or via splines. The estimator's flexibility extends to semi- or fully nonparametric first-stage specifications.

Practical and Theoretical Implications

The paper provides a general framework for addressing quantile regression under joint endogeneity and measurement error in the outcome. This methodological advance is directly applicable to many empirical domains (e.g., consumption Engel curves, survey-based income processes). The identification theorem confirms the necessity of monotonicity and independence assumptions, extending preceding work to endogenous regimes with weaker dependence restrictions via copulas.

The estimator is robust to model misspecification and is computationally efficient under B-spline sieves and EM-type starting values. Practical applications may include heterogeneous treatment effect estimation, individual demand modeling with self-reported data, and dynamic production settings with noisy outcomes. Theoretical extensions to multiple endogenous regressors via vector-valued copula control functions are outlined, confirming broad applicability.

Conclusion

The paper formally resolves nonparametric identification for quantile models in the presence of endogenous regressors and measurement error, and provides a computationally feasible two-step sieve ML estimator achieving bias reduction and valid inference. Monte Carlo simulations confirm these properties, with bootstrap confidence intervals showing reliable coverage. The methodology extends the QR literature to settings previously considered intractable, and sets the stage for future empirical deployments targeting distributional effects under measurement error and endogeneity.