- The paper introduces an asymmetric interval framework that adjusts prediction intervals for skewed response distributions.

- It employs a three-stage estimation process—central tendency, local scale, and local skewness—using methods like random forests.

- Empirical results on seven datasets demonstrate that the skew-adaptive approach achieves narrower intervals while preserving marginal validity.

Introduction and Motivation

The paper "Skew-adaptive conformal prediction" (2605.16145) presents an extension of the split conformal prediction (CP) framework for regression, designed to address the limitation of symmetric prediction intervals. Standard split CP methods, notably the scaled-score approach, produce intervals that are symmetric around a point estimate, adapting interval width to local uncertainty but not to potential skewness in the conditional distribution of the response variable. This work introduces a principled mechanism for constructing asymmetric (skew-adaptive) intervals that remain marginally valid under exchangeability.

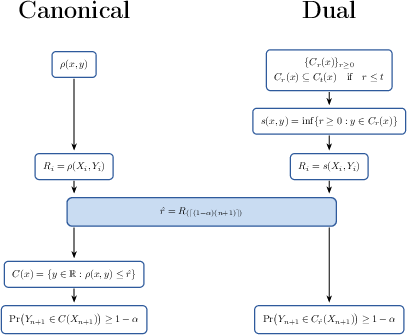

The split conformal framework can be conceptualized from two mathematically equivalent but procedurally distinct views: the canonical (conformity-function-first) and the dual (interval-family-first) constructions.

The canonical view specifies a conformity function (e.g., scaled absolute residuals), computes conformity scores for the calibration sample, and defines the prediction interval as the sublevel set corresponding to a calibrated threshold. The dual view, following Gupta et al. (2022), instead fixes a nondecreasing family of intervals and derives the conformity function as the "gauge" measuring minimal expansion required for y to fall in the interval at x. Both views ensure finite-sample marginal validity, but they permit flexibility in where modeling and design choices are introduced into the procedure.

Figure 1: Diagrammatic comparison of canonical (conformity-first) and dual (interval-family-first) constructions of split conformal prediction, elucidating the convergence of both views to finite-sample valid intervals.

The core methodological contribution is the introduction of an asymmetric interval family parameterized by a central estimator μ^(x), a local scale σ^(x), and a local skewness parameter γ^(x). The interval at expansion factor r is

Cr(x)=[μ^(x)−rσ^(x)e−γ^(x),μ^(x)+rσ^(x)eγ^(x)],

where γ^(x) modulates left/right interval width asymmetrically. The conformity (gauge) score induced by this family for each calibration residual (Xi,Yi) is

Ri=max{σ^(Xi)e−γ^(Xi)(μ^(Xi)−Yi)+, σ^(Xi)eγ^(Xi)(Yi−μ^(Xi))+}.

This construction strictly generalizes the scaled-score method by allowing x0, as a data-driven function, to impart spatially varying tilt to the prediction intervals.

Learning Skewness and Sequential Model Estimation

The three-stage estimation pipeline operates as follows:

- Central Tendency: Train x1 on the features and responses.

- Local Scale: Residuals x2 are modeled by x3 to capture conditional scale heterogeneity.

- Local Skewness: Signed, scaled residuals are further transformed via the inverse hyperbolic sine, i.e.,

x4

to produce a target for learning x5, thus encoding the directionality of predictive errors in a manner matched to the analytic form of asymmetric expansion.

Implementation-wise, all three functions can be estimated by any expressive regression method; the experiments employ random forests for all components. Notably, setting x6 recovers the symmetric scaled-score baseline, clarifying the strict extensibility of this approach.

Prediction Interval Efficiency and Estimation

The calibration sample can be used not only for coverage calibration but also to estimate the relative efficiency of skew-adaptive versus symmetric intervals. The expected width ratio

x7

(where x8 denotes skew-adaptive intervals and x9 the respective calibrated thresholds) can be consistently estimated empirically under regularity conditions. The authors provide theoretical results on consistency and practical estimators for this ratio, enabling model comparison without requiring a labeled test set.

Empirical Evaluation

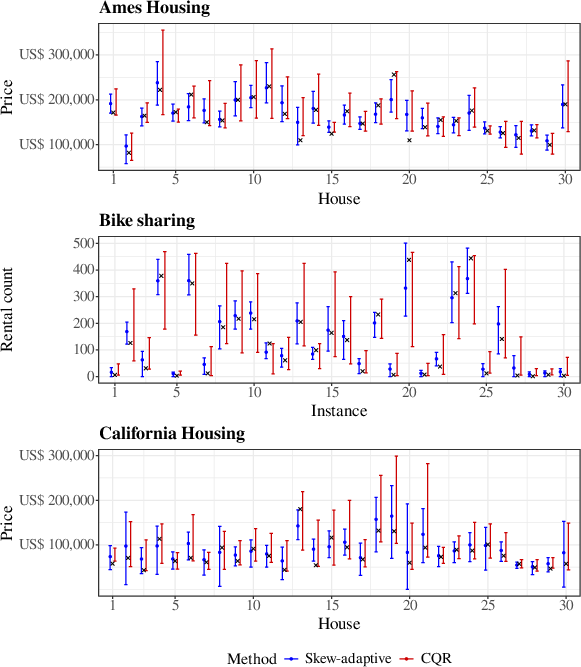

Seven public regression datasets of varying size and skewness were used to compare (a) the skew-adaptive method, (b) the classical scaled-score CP method, and (c) conformalized quantile regression (CQR). Coverage was essentially at the target nominal value across datasets for all methods, consistent with CP guarantees. The strong empirical finding is that the skew-adaptive procedure produces narrower intervals than both comparators, particularly pronounced in settings with asymmetric response distributions.

Figure 2: Test-set prediction interval comparisons on selected datasets, illustrating the adaptivity and asymmetry of skew-adaptive intervals (blue) relative to CQR (red), with responses marked as black crosses and blue dots denoting point predictions.

Across all datasets and coverage levels, the skew-adaptive intervals exhibited the smallest average width, with calibration-based efficiency estimators closely tracking holdout-set empirical averages (as shown in Table 3 of the paper). Thus, the method achieves improved efficiency while maintaining marginal validity, confirming the utility of local asymmetry modeling in practical conformal inference.

Theoretical and Practical Implications

This work advances the theory of conformal prediction by synthesizing the dual/gauge functional formulation with flexible, data-driven modeling of asymmetry in predictive uncertainty. The methodology can be straightforwardly generalized to alternative conformal inference frameworks (e.g., out-of-bag CP, stacked CP), as the estimation and calibration dynamics decouple from the asymmetric geometry.

From a practical standpoint, the implementation is model-agnostic and remains assumption-lean, requiring only data exchangeability for coverage guarantees. The estimator for relative interval efficiency allows practitioners to select the most efficient conformal predictor empirically, even when unlabeled test instances are unavailable.

Conclusion

The skew-adaptive extension to split conformal prediction integrates asymmetry modeling via a theoretically motivated, interpretable parameterization that preserves marginal validity. Empirical evidence shows systematic gains in efficiency relative to standard symmetric conformal methods and conformalized quantile regression. The approach generalizes naturally to other conformal frameworks, suggesting broad applicability for predictive uncertainty quantification in settings with heterogeneous, asymmetric noise. Future directions include the exploration of alternative skewness parameterizations, application to high-dimensional and structured output spaces, and algorithmic refinement for online and streaming contexts.