- The paper presents OLCP and OLCP-Hedge to merge localized calibration with online error feedback for robust coverage under nonstationary conditions.

- It uses a weighted local quantile framework and online gradient updates to adapt prediction intervals based on local covariate distributions.

- Empirical results show that OLCP maintains near-nominal coverage while producing narrower intervals than traditional global calibration methods.

Introduction and Motivation

The conformal prediction framework has long served as a principled approach to obtaining distribution-free, finite-sample uncertainty quantification in regression and classification. However, standard CP guarantees rely on exchangeability—a property routinely violated in time-series, streaming, or otherwise heterogeneously dependent data. While recent online conformal methods attain long-run validity under distribution shift (notably, Adaptive Conformal Inference (ACI) and its variants), their global calibration is fundamentally inefficient in the presence of covariate-dependent heteroskedasticity or distributional heterogeneity. In contrast, Localized Conformal Prediction (LCP) enables the size of prediction sets to adapt to local uncertainty regimes but relies on exchangeability and does not address temporal dependence or nonstationarity.

The paper "Online Localized Conformal Prediction" (2605.05497) synthesizes these two approaches, introducing a method—OLCP—that delivers coverage-guaranteed, locally adaptive conformal intervals in online or temporal settings. Further, the method is made robust to bandwidth selection for the localization kernel via OLCP-Hedge, an expert-aggregation scheme formulated as constrained online convex optimization. This architecture yields provable long-run marginal coverage with improved efficiency in heterogeneous, nonstationary settings as demonstrated both theoretically and empirically.

Methodological Framework

Localized Online Coverage-Tracking

OLCP operates in a sequential setting, constructing prediction sets Ct(Xt) for Yt at each time point t given observed covariates Xt. Instead of calibrating quantiles globally, OLCP induces a localized empirical distribution over conformity scores, weighting calibration residuals via proximity in covariate space (using, for example, an exponential kernel with bandwidth h). In analogy with LCP, but now in the strictly online setting, only past observations within a rolling window are used at each time. For a selected bandwidth, the weighted quantile function Q(1−β;Dt(h)(Xt)) determines set radii.

Critically, the nominal miscoverage level αt (analogous to $1 -$ coverage) is not fixed but is updated online using observed errors, following a projected online gradient descent rule:

αt+1=Π[0,1](αt+γ(α−errt))

where γ is a stepsize, Yt0 denotes projection onto Yt1, and Yt2 is the miscoverage indicator at time Yt3. This update aligns the empirical long-run mean miscoverage with the target, even under nonstationarity.

Expert Aggregation: OLCP-Hedge

Selecting the bandwidth governing the localization kernel severely impacts efficiency and validity; aggressive localization responds to heterogeneity but can become unstable, while large bandwidth reverts to global calibration. The OLCP-Hedge algorithm addresses this by running a pool of OLCP experts (each with a distinct bandwidth) and casting bandwidth selection as online convex optimization with adversarial constraints.

At each round, OLCP-Hedge selects a randomized mixture over experts to minimize expected prediction interval width, subject to the constraint that excess miscoverage remains controlled. This is implemented via a Lyapunov-augmented, AdaHedge-like algorithm, yielding Yt4 regret in set size and Yt5 cumulative expected excess miscoverage. The analysis derives from projection-based arguments and exploits full-information feedback.

Empirical Results

The paper demonstrates the efficacy of OLCP and OLCP-Hedge on synthetic and real-world time series benchmarks, measuring both marginal coverage and average interval width relative to classical and adaptive baselines. Numerical results show that OLCP and OLCP-Hedge consistently achieve near-nominal coverage (typically Yt6) with narrower intervals than ACI or DtACI, especially under covariate heterogeneity or abrupt distribution shifts.

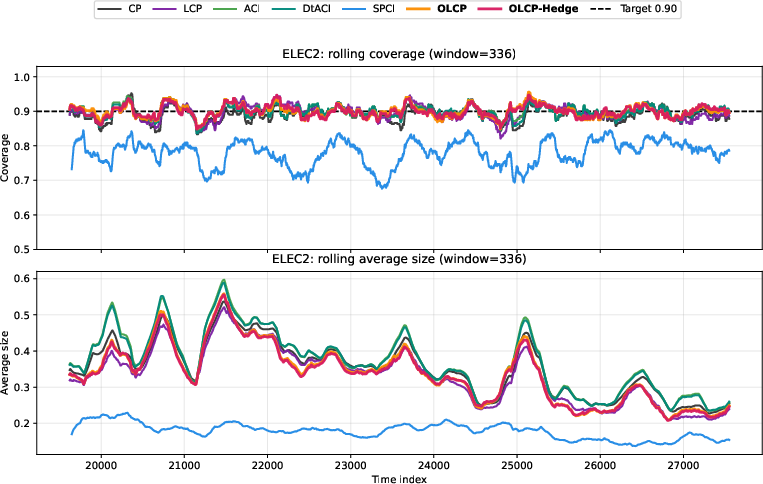

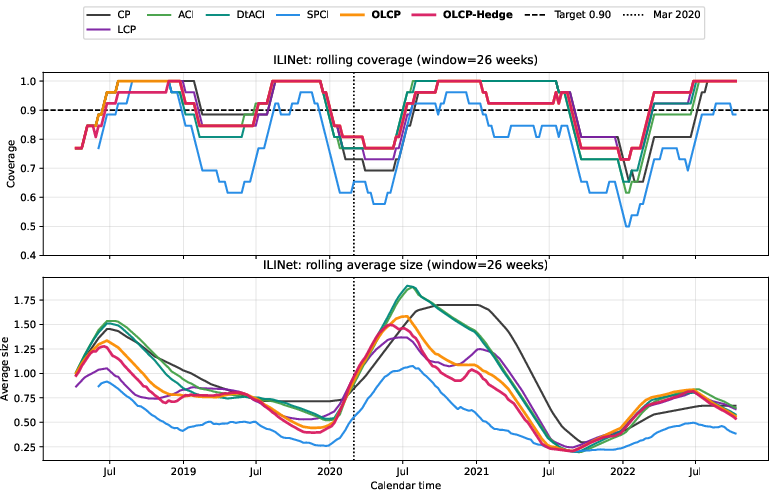

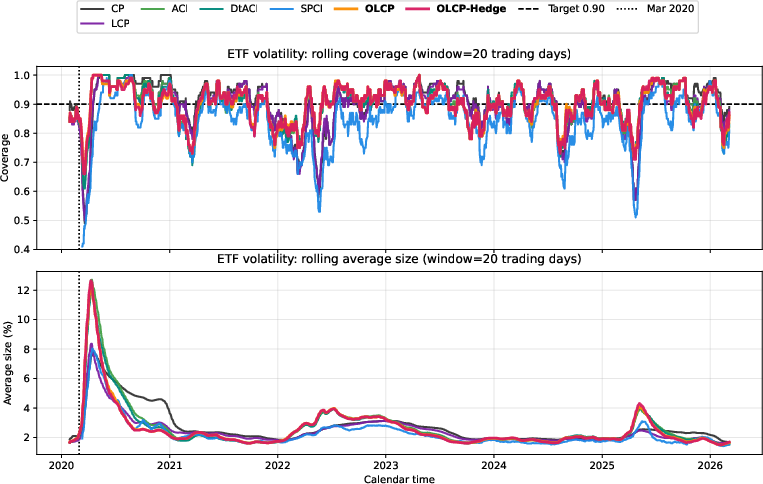

Real-Time Series: Rolling Diagnostics

On real datasets (electricity markets, CDC ILINet, and ETF volatility), the rolling analysis of coverage and size elucidates the benefits of localized adaptation. ACI and DtACI adjust interval sizes only globally and tend to inflate widths to maintain validity under shift, but fail to exploit local heterogeneity. In contrast, OLCP and OLCP-Hedge keep rolling coverage close to the target while producing intervals that are noticeably narrower in benign regimes without compromising validity in volatile regimes.

Figure 1: ELEC2—Rolling coverage and interval size reveal OLCP and OLCP-Hedge maintaining coverage with more efficient intervals compared to global adaptive methods.

Figure 2: ILINet—OLCP and OLCP-Hedge sustain coverage through COVID regime change, maintaining compact intervals relative to ACI/DtACI.

Figure 3: ETF volatility—OLCP-based approaches adapt to volatility clustering, preserving validity with reduced excess width compared to global baselines.

Furthermore, stratification of results by volatility regime (VIX levels) demonstrates that localized methods extract efficiency gains during quieter periods that are missed by globally calibrated approaches, while not sacrificing coverage amid regime changes or stress.

Theoretical Implications

The main theoretical contribution is the demonstration that localization and online feedback calibration can be simultaneously employed without sacrificing coverage guarantees—an open issue in prior work. The proof constructs a non-asymptotic long-run calibration identity for the OLCP update (including projection boundary corrections), and the COCO-based aggregation bound shows regret and constraint violation are tightly controlled as functions of the expert pool size and sample path.

Notably, the analysis does not rely on strong stationarity or exchangeability assumptions. The design ensures that the efficiency-efficiency tradeoff (coverage vs. interval width) can be approached adaptively, rather than fixed a priori.

Practical and Theoretical Implications

Practically, OLCP and OLCP-Hedge supply the first framework for sequential, calibration-valid conformal inference that is robust to both temporal distribution shift and arbitrary covariate heterogeneity, with a built-in mechanism for tuning the critical bandwidth parameter. This makes the method broadly applicable to real-world forecasting, anomaly detection, and sequential decision tasks where both local uncertainty adaptation and long-term validity are required.

Theoretically, this work demonstrates the compatibility between online convex optimization for constrained objectives and nonparametric coverage guarantees, opening avenues for more general forms of expert aggregation (e.g., adapting step sizes, kernels, or window lengths as well). It also motivates new research into doubly-local coverage control and bandit-feedback optimization for conformal quantiles.

Conclusion

"Online Localized Conformal Prediction" establishes a rigorous, broadly applicable solution to the core challenge of valid uncertainty quantification under both temporal and cross-sectional nonstationarity. By joining local kernel weighting with online error feedback, and abstracting hyperparameter selection to a constrained convex optimization paradigm, the approach navigates the classic efficiency--validity tradeoff with strong theoretical guarantees and practical robustness.

Future extensions include dynamic adaptation over additional kernel or calibration configurations, local coverage control, and relaxation of full-information feedback assumptions for highly scalable or partially observed data streams.