- The paper establishes that order flow exclusivity drives over 70% of builder revenue, underlining the systemic centralization in Ethereum.

- The study employs statistical metrics (including KL divergence) and a Random Forest classifier to differentiate between atomic and non-atomic MEV flows.

- The analysis reveals that PBS design creates positive feedback loops, deepening capital barriers and reinforcing an emerging builder oligopoly.

Order Flow Exclusivity and Ethereum Builder Centralization: Technical Dissection

Introduction and Motivation

This study, "Order Flow Exclusivity and Value Extraction Mechanisms: An Analysis of Ethereum Builder Centralization" (2605.04471), rigorously interrogates the structural dynamics of centralization within Ethereum's Proposer-Builder Separation (PBS) framework, focusing on the order flow exclusivity phenomenon and the mechanisms of value extraction driving builder oligopolization. While prior analyses often restrict their focus to prominent order flows, this work systematically maps the landscape of both Exclusive Order Flows (EOFs) and under-explored non-atomic Maximal Extractable Value (MEV) strategies using a combination of statistical and machine learning tools. The objective is to provide quantitative evidence for the claim that the centralization of the builder market is an emergent and possibly inevitable consequence of the current PBS protocol design.

Methodology: Comprehensive Order Flow Analysis

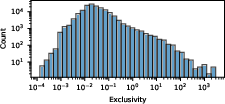

The study leverages a full-scale scan of Ethereum activity between September 2023 and August 2025, encompassing 164,249 order flows over 152 million swap transactions. These flows are defined at the granularity of destination contract, overcoming the granularity-coverage tradeoffs found in purely address- or label-driven methodologies. The authors introduce a statistically grounded exclusivity metric based on the Kullback-Leibler (KL) divergence of a flow's bribe distribution relative to global market share, weighted to correct both for endogeneity (dominant builders naturally absorbing more public order flows) and sample size (avoiding stochastic noise from sparse flows). This enables precise EOF identification and results in a heavy-tailed distribution of exclusivity scores.

Figure 1: Distribution of order flow exclusivity E, highlighting a small number of outlier EOFs among a vast population of low-exclusivity public flows.

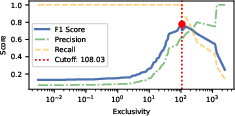

Threshold optimization was conducted using F1-score maximization over a labeled dataset, resulting in an empirically-justified exclusivity threshold.

Figure 2: Threshold selection for EOF classification, illustrating optimal cutoff via F1-score maximization.

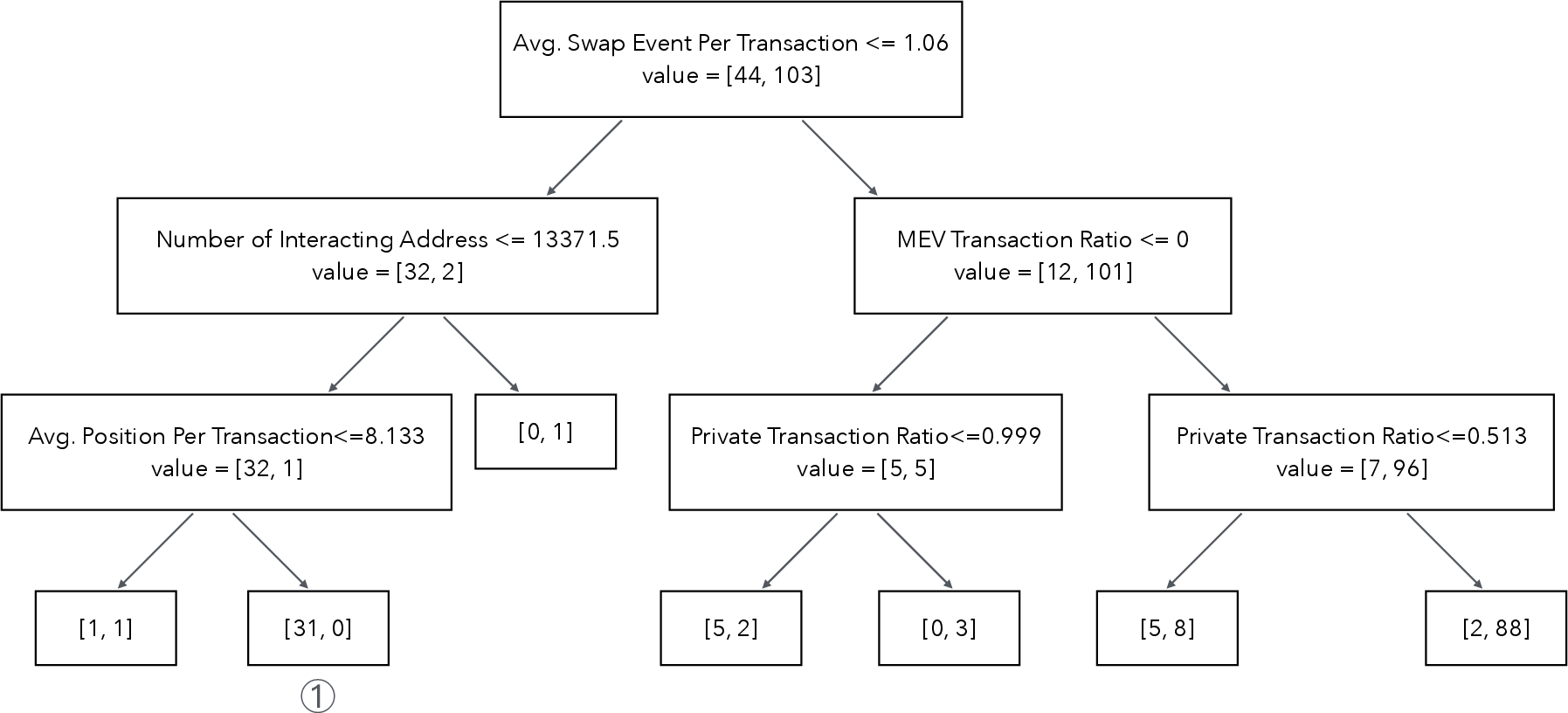

To classify non-atomic MEV flows, the authors curated manual labels for the top revenue-contributing contracts and developed a supervised Random Forest classifier operating over an expanded feature set that aggregates both transaction- and contract-level statistics (e.g., average swap events, unique sender counts, frequency of private transactions). This contract-level behavioral profiling enabled accurate separation between atomic, non-atomic, and protocol order flows.

Figure 3: Representative decision tree logic from the ensemble used for non-atomic MEV identification, with low swap event counts being a dominant early split for non-atomic MEV.

Empirical Findings: Quantifying Exclusivity and Non-Atomic MEV

Prevalence and Revenue of EOFs

Application of the exclusivity metric identified 75 EOFs, 68 of which are previously unreported, jointly accounting for over 70% of all builder revenue from trading activities. Notably, the metric's sensitivity reveals that prior literature systematically underestimated the prevalence and revenue concentration of EOFs.

Further, analysis of builder dependence on EOFs reveals heterogeneous operational modes. Dominant builders (e.g., Titan, Beaverbuild) initially accumulated market share through persistent access to high-value EOFs but subsequently decoupled continued dominance from ongoing EOF dependency, indicating a positive-feedback regime shift.

Figure 4: Distribution of EOF dependency ratios (EDR) across major builders, showing structural reliance among both dominant and specialized niche builders.

Expansion of Non-Atomic MEV Discovery

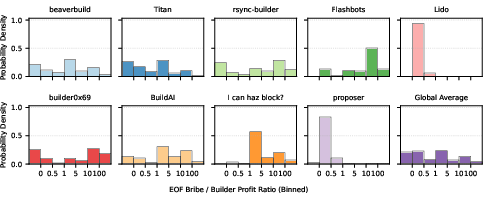

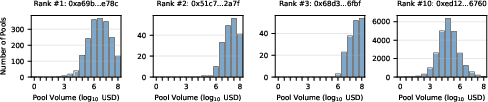

The supervised detection framework identifies 322 non-atomic MEV flows, uncovering a substantial long tail that had eluded previous heuristic methods. These flows account for nearly 23% of the total builder revenue, with the top nine responsible for over 70% of non-atomic bribes—indicating both head concentration and tail resilience. The power-law fit (α=1.47) confirms infinite-variance characteristics, relevant for modeling systemic risk and competitive barriers.

Figure 5: Distribution of trading pool volumes targeted by top non-atomic MEV order flows, illustrating diverse strategies between head and tail actors.

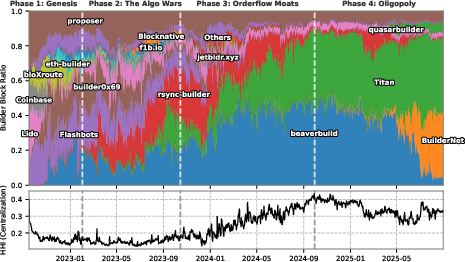

Temporal Dynamics: Market Centralization Trajectory

A longitudinal market share and Herfindahl-Hirschman Index (HHI) analysis uncovers four distinct eras: Genesis, Algorithm Wars, EOF Moats, and Oligopoly. Market concentration increased monotonically, with consolidation accelerating during periods where EOF access became the dominant strategic edge.

Figure 6: Builder market share evolution and HHI index, demarcating competitive eras and the ascent to oligopoly.

Significant findings include the fact that non-atomic MEV revenue share increased across all eras, and by the study's end period matched atomic MEV profitability, implying escalating capital/inventory risk barriers and deepening economic moats for new market entrants.

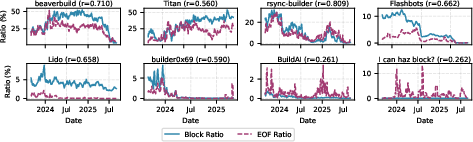

Dynamic analysis of builder market share-EOF revenue correlation demonstrates a regime change: EOFs were a prerequisite for initial dominance, but in the oligopoly regime, incumbent builders maintained market share even as EOF dependency fell, sustained by network effects and established economic alliances.

Figure 7: Daily time series of block share (blue) versus EOF ratio (red) for top builders, indicating the decoupling of EOF reliance from dominance in the Oligopoly era.

Discussion: Implications for Protocol Design and Market Structure

The empirical data supports several central contentions:

- EOFs and non-atomic MEV are not exclusive inventions of the top builders; niche and mid-tier builders maintain operational viability via highly selective, exclusive order flows.

- Builder centralization is not solely driven by superior algorithms or hardware, but by compounding barriers: information asymmetry (private routing and off-chain data), increasing returns to scale, and lock-in from positive feedback loops between market share and order flow exclusivity.

- PBS, as currently realized, structurally violates critical conditions for competitive markets: (i) fails diminishing returns to scale, (ii) undermines information symmetry, (iii) increases entry barriers via social and capital moats. The ordinal, winner-takes-all auction structure of PBS compounds these effects.

These observations raise significant concerns regarding Ethereum's decentralization and censorship resistance guarantees, especially under adversarial conditions or protocol shocks. The emergence of cartel-like sharing arrangements (e.g., BuilderNet) introduces additional complexity: while aiming to reduce centralization, such structures may reinforce oligopoly by internalizing competition and raising further technical (TEE-based) entry requirements.

Theoretical and Practical Implications

The findings suggest that superficial mitigations—such as rotating builder addresses or modest transparency initiatives—are inadequate. Addressing protocol-level flaws in PBS or rethinking the incentives for decentralized block construction are required for genuine rebalancing of economic power. Research may need to focus on mechanisms restoring (a) information symmetry or access parity, (b) reduced returns to builder scale, or (c) stronger alignment of consensus and execution layers.

Conclusion

This analysis demonstrates, with strong quantitative backing, that order flow exclusivity and non-atomic MEV extraction jointly act as both markers and accelerants of a wider centralization process embedded in Ethereum's PBS-based architecture. While EOFs created the initial moat for dominant builders, entrenched positions are now sustained by large-scale network effects and capital-intensive non-atomic MEV. The paper argues that, absent architectural intervention, builder centralization is an inevitable outcome, with direct ramifications for protocol security, stability, and censorship resistance. The study thus provides both a framework for rigorous future measurement and a challenge to the Ethereum research community to reimagine block construction models that genuinely resist centralization.

- (Figure 1): Distribution of order flow exclusivity scores

- (Figure 2): EOF threshold optimization via F1-score

- (Figure 4): Builder dependency ratios on EOFs

- (Figure 5): Trading pool volume distribution exploited by non-atomic flows

- (Figure 3): Representative decision tree from the Random Forest classifier

- (Figure 6): Market share/HHI evolution by era

- (Figure 7): Correlation of builder block share with EOF revenue over time

Conclusion

The systemic analysis presented in this paper clarifies the causal mechanisms underlying market centralization within Ethereum's PBS framework and provides robust methodological innovations for order flow classification. While the results reinforce the notion that order flow exclusivity is necessary but no longer sufficient for top-tier dominance, they emphasize that only fundamental architectural mitigation in PBS can arrest trend toward builder oligopoly. Future research should explore protocol-level reforms, empirical modeling of alternative incentive mechanisms, and more granular detection/simulation frameworks for ongoing market monitoring.