- The paper introduces SA-BCP, which decouples temporal and spatial evidence using a density-based gating mechanism to retain near-oracle conditional coverage.

- SA-BCP leverages a single interpretable threshold to balance rapid temporal adaptation with stable spatial memory, achieving 10-37% narrower prediction intervals in volatile markets.

- Empirical validation across financial assets demonstrates SA-BCP's optimal bias-variance tradeoff, ensuring consistent coverage and improved predictive efficiency.

Introduction and Motivation

The manuscript titled "Optimal Spatio-Temporal Decoupling for Bayesian Conformal Prediction" (2605.00432) addresses the persistent issue of uncertainty quantification under non-stationarity in online time series. Classical Conformal Prediction (CP) delivers strong marginal coverage guarantees under exchangeability but fails during distribution shifts or regime changes—a reality in practical domains such as finance. Existing adaptations—feedback-driven (e.g., Adaptive Conformal Inference, ACI) and temporally-discounted Bayesian CP (BCP)—tend to overfit in stable periods or lag after shocks, respectively. The core innovation, State-Adaptive Bayesian Conformal Prediction (SA-BCP), fundamentally decouples temporal adaptability from structural stability by integrating spatio-temporal evidence through a density-based gating mechanism.

Methodological Architecture

SA-BCP decomposes the non-conformity score calibration into two principal axes: a temporal base density capturing recent volatility (as an exponentially discounted memory) and a local spatial state, extracted by kernel density estimation over a dynamic state vector constructed from lagged features. The interaction is mediated by a single interpretable hyperparameter, the matching threshold K, which determines the epistemic gate between temporal inertia and spatial pattern memory.

A critical mechanism is the computation of the spatial proportion πSt, defined by the normalized kernel density match of current state to history. When DSt≪K, coverage relies on the temporal component; as historical matches accrue, the system increasingly leverages the spatial empirical cumulative distribution. The final predictive interval margin is set by dynamically root-finding the appropriate quantile from the mixture empirical CDF, augmented by a vanishing prior for cold-start robustness.

Theoretical Guarantees

The theoretical backbone of SA-BCP is constructed with a logical progression of results:

- Asymptotic Marginal Validity: Under mild continuity and drift conditions on the evolving distribution of scores, the empirical coverage converges to the nominal target for any finite K. This ensures that hybrid gating does not violate foundational CP guarantees.

- Adversarial Regime Protection: When spatial evidence is absent (i.e., for unseen shocks), SA-BCP defaults to discounted BCP and inherits dynamic regret bounds analogous to FTRL-type algorithms, with regret scaling optimally with distributional path length and effective inertia.

- Oracle Conditional Coverage: In regimes where recurrence is present, and accumulating matches dominate (DSt→∞), coverage becomes conditional—eventually achieving near-oracle interval efficiency.

- Optimal Bias-Variance Tradeoff: The minimax optimal K∗ is formally shown to balance the ratio between irreducible (aleatoric) spatial variance V0 and the structural lag from the temporal baseline MT, with the risk measured by the Winkler score minimized at K∗=O(V0/MT).

Empirical Analysis

Progressive Anomaly Recognition

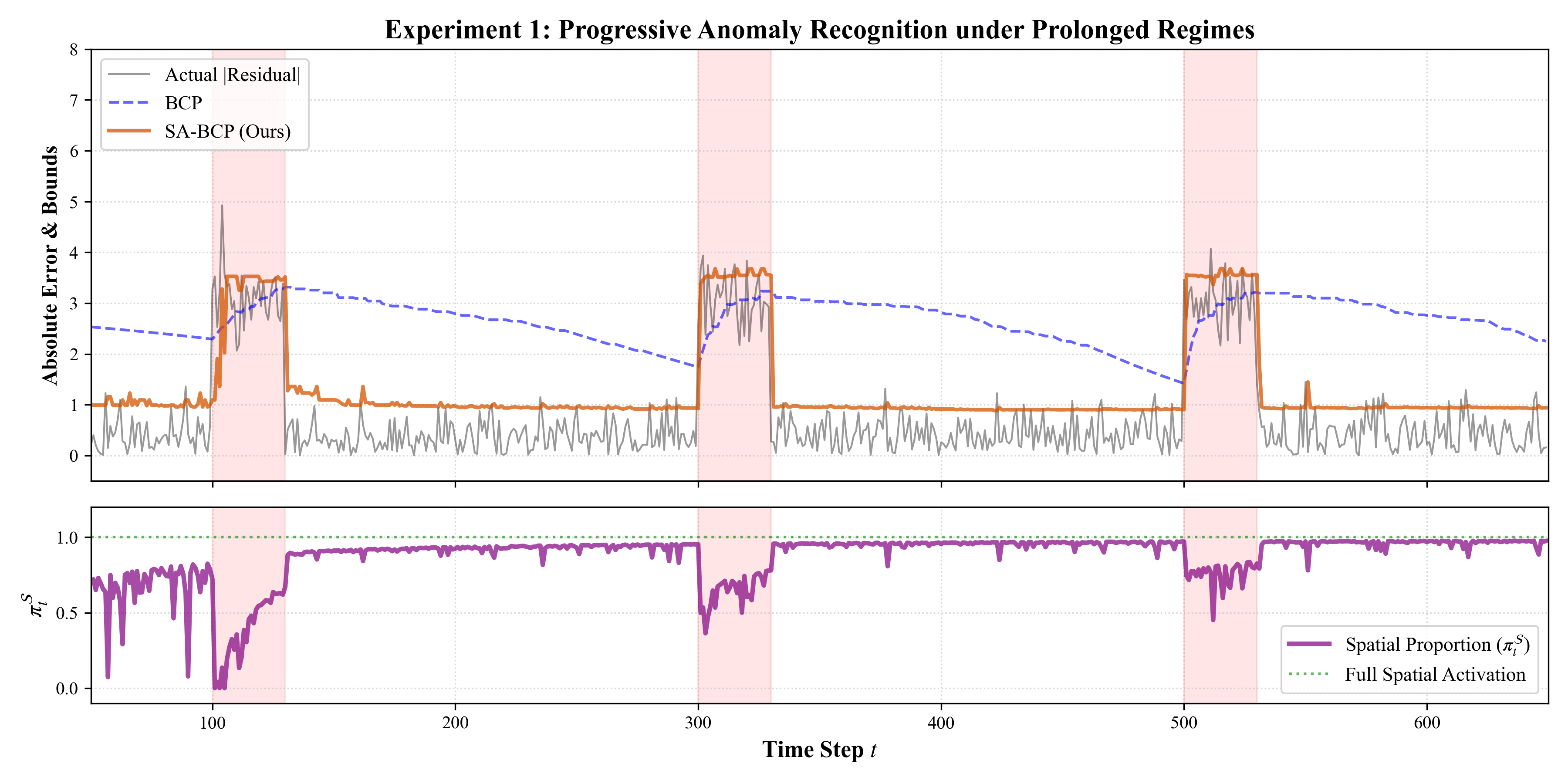

The ability to adapt and "memorize" rare shocks is empirically showcased in synthetic switching environments with alternating regimes. SA-BCP dynamically suppresses its spatial gating during unprecedented shocks, behaving conservatively. On subsequent repetitions, the spatial density increases, and the gating preemptively adjusts interval width prior to pure temporal adaptation, in contrast to BCP's lagging response.

Figure 1: SA-BCP's spatial proportion πSt exhibits rapid recovery and increasingly shallow troughs as rare shocks recur, highlighting proactive interval optimization.

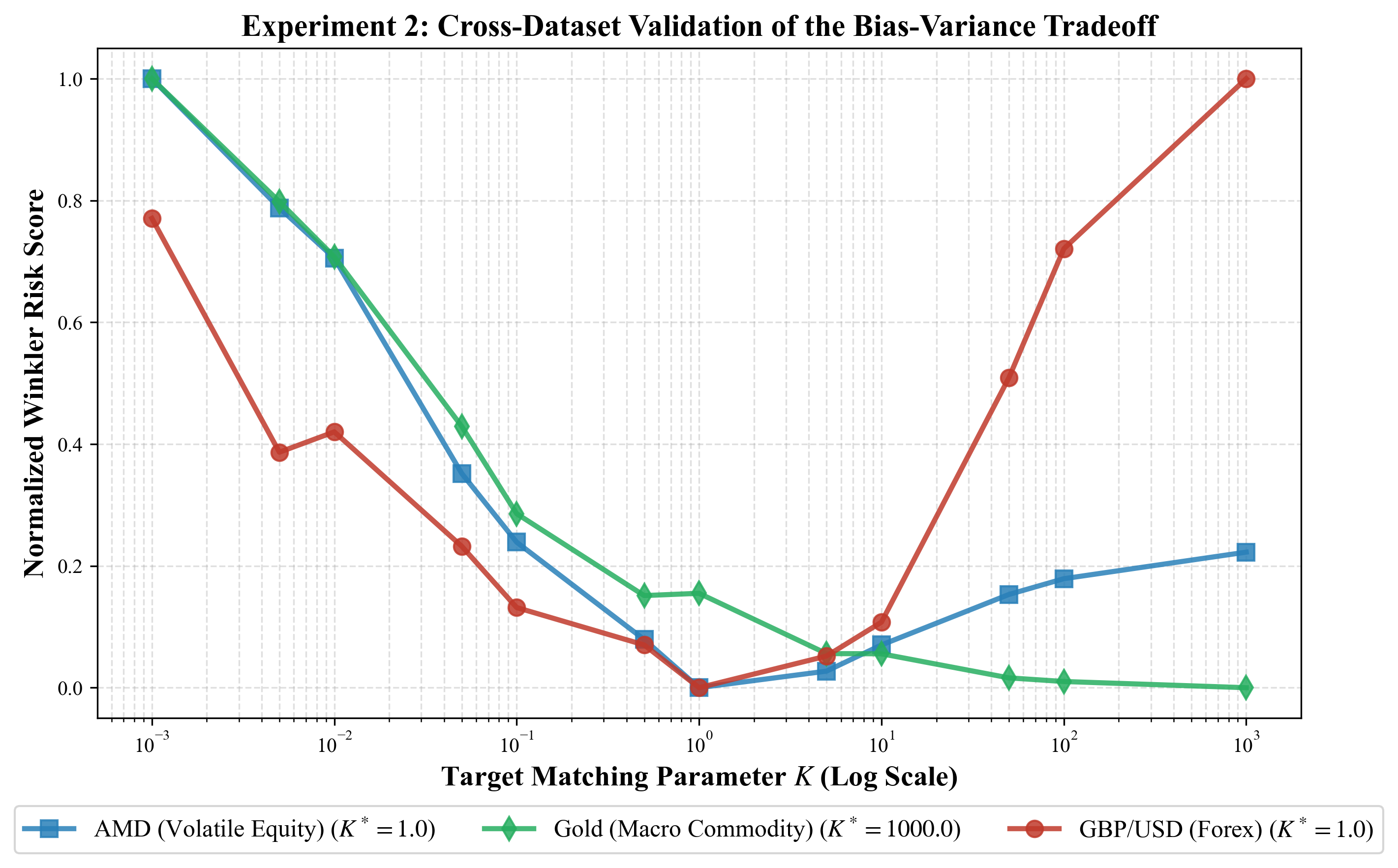

Cross-Dataset Bias-Variance Validation

Varying πSt0 across asset classes (GBP/USD, AMD, Gold) reveals asset-specific bias-variance optima:

Figure 2: Normalized Winkler scores across πSt1 showcase dataset-dependent risk curves; sharp minima for assets with frequent shocks, and monotonic curves for assets with high inertia.

- For GBP/USD, characterized by abrupt, infrequent interventions, a narrow πSt2 yields the best tradeoff.

- For AMD (high-beta equity), optima are similar, with rapid performance declines when overfitting to noise.

- For Gold, the risk continues to decrease with πSt3, indicating that temporal memory dominates and spatial intervention is rarely optimal.

Real-World Benchmarking

SA-BCP is benchmarked against leading adaptive and Bayesian CP variants over a decade of financial data. Two core claims are substantiated:

- SA-BCP achieves consistent target coverage: ACI-based feedback-driven methods exhibit chronic under-coverage during high volatility, whereas SA-BCP maintains coverage close to the nominal level even during market stress, thanks to its spatial activation.

- Predictive efficiency: Intervals produced by BCP are consistently wider—by 10-37%—than SA-BCP at high confidence levels. The reduction in interval width, while preserving (or improving) coverage, translates to actionable gains in real-world settings. SA-BCP minimizes the Winkler score in the majority of test cases, often outperforming baselines under stringent risk constraints.

Practical Implications and Future Outlook

The introduction of spatio-temporal decoupling via statistical evidence gating demonstrates a statistically principled solution to the adaptivity-stability schism prevalent in CP for non-stationary streaming. The principled selection of πSt4—now grounded in minimax theory—provides practitioners with an interpretable and data-driven lever, reflecting the physical drift and recurrence properties of the target process. Notably, the parameter-free degeneracy of SA-BCP in pure spatial or temporal extremes guarantees no pathological failures, independent of asset class or data period.

A prominent avenue for further development is online adaptation of πSt5 itself—effectively a higher-order meta-learning procedure that would allow real-time tuning of bias-variance tradeoff in dynamic environments. Additional extensions include joint decoupling across multi-horizon and multi-output scenarios, where the spatio-temporal recurrence structure is complex yet potentially exploitable for further efficiency.

Conclusion

This work rigorously formalizes and empirically validates the optimal decoupling of temporal and spatial evidence in Bayesian Conformal Prediction, yielding substantial improvements in both marginal calibration and predictive efficiency in volatile online regimes. SA-BCP provides a unified, interpretable, and computationally efficient framework for actionable uncertainty quantification in non-stationary, high-stakes settings, with direct applicability to finance, operational forecasting, and beyond. The proposed methodology establishes a new baseline paradigm for addressing recurring regime shifts and structural shocks within the conformal prediction ecosystem.