- The paper introduces CLVAE, a variational autoencoder that integrates process-based likelihoods with deep representation learning to forecast long-term customer revenue.

- It employs an encoder-decoder framework with Gamma-distributed latent variables to model customer attrition, transaction timing, and spending from sparse data.

- Empirical results across retail datasets show that CLVAE reduces RMSE compared to classical Pareto/NBD and deep learning baselines, ensuring robust long-horizon predictions.

CLVAE: Variational Autoencoder for Long-Term Customer Revenue Forecasting

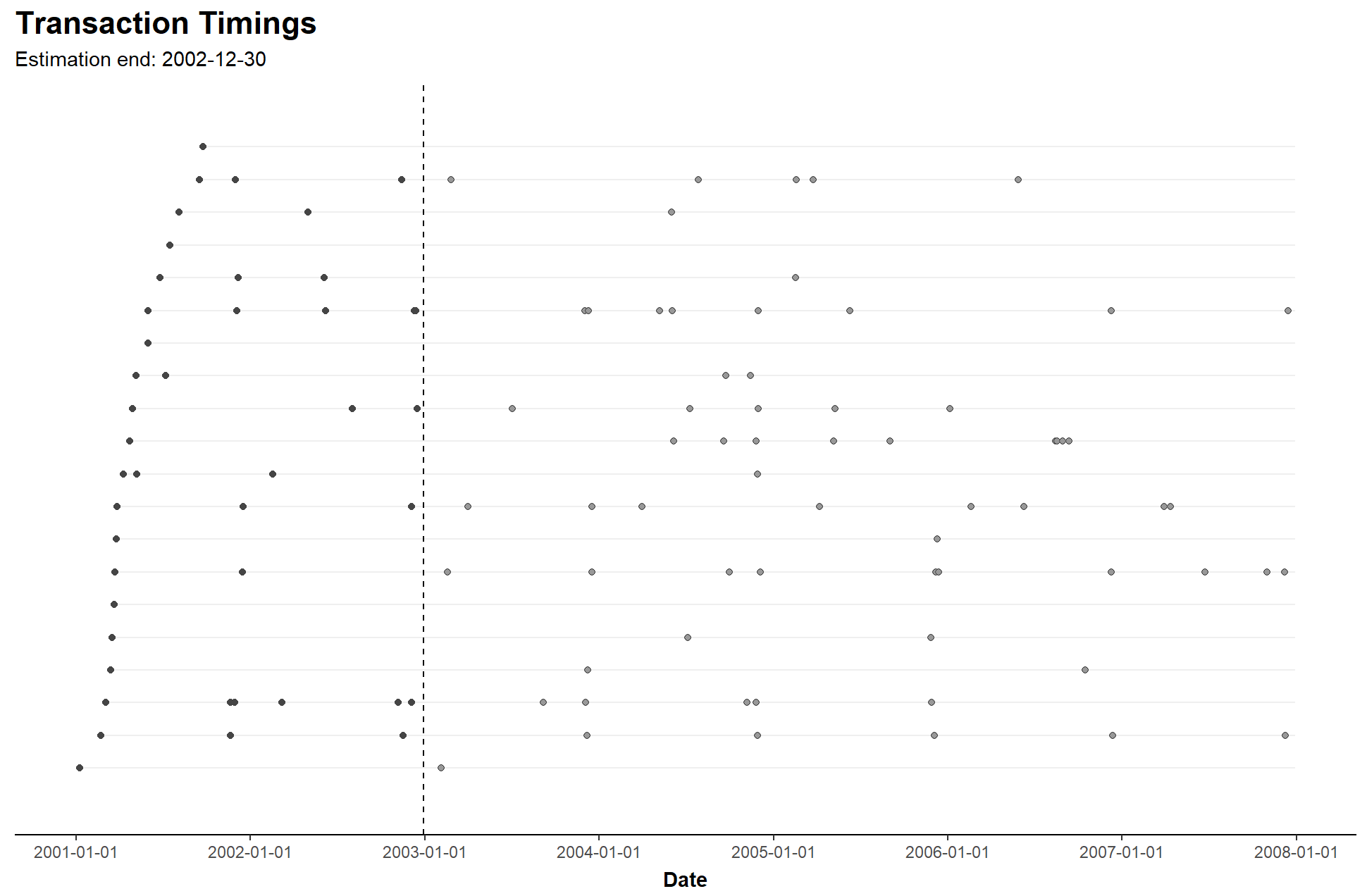

Long-term customer revenue forecasting from sparse and irregular transaction histories is a central task in non-contractual settings, underpinning resource allocation and campaign targeting. The problem is exacerbated by extensive customer heterogeneity, ambiguity in attrition (unobserved dropout versus temporary inactivity), and the typical sparsity and unevenness of purchase histories (as illustrated in real-world data in Figure 1).

Figure 1: Real-world transaction data for 20 customers, demonstrating sparsity and irregularity in purchase events across a retailer’s customer base.

Traditional solutions—probabilistic customer base models such as Pareto/NBD for attrition and transaction timing, and Gamma-Gamma (GG) for spend estimation—offer robustness and interpretable likelihoods but are inherently limited by rigid parametric assumptions about latent customer heterogeneity. Although machine-learning approaches like LSTM-based sequence models increase flexibility, they require substantial data and do not directly model spend, constraining their utility in revenue prediction. The paper addresses the tension between structural discipline and flexibility, proposing an overview that leverages the strengths of process-based likelihood modeling and representation learning via deep latent-variable architectures.

Model Architecture and Methodology

The proposed Customer Lifetime Value Variational Autoencoder (CLVAE) is a likelihood-based VAE embedding the tripartite structure of customer attrition, transaction timing, and spending—the canonical process components of traditional models—while learning a nonparametric mixing distribution for latent customer propensities through encoder-decoder neural networks (see Figure 2).

Figure 2: Conceptual visualization of the CLVAE model, combining process-based likelihoods with learned flexible heterogeneity.

Formally, observed customer features (x, tx, T, zˉ)—recency, frequency, tenure, and mean spend—are compressed via an encoder network into a latent representation (λ, μ, ν) describing propensities for transaction, attrition, and spending. The decoder reconstructs the likelihood of observed transaction histories, retaining the structural form of Pareto/NBD and GG models but allowing the latent variables to interact in nonlinear, nonparametric ways. The posterior and prior over latent variables are modeled as independent Gamma distributions, facilitating efficient amortized variational inference.

A key methodological contribution is the preservation of process-based likelihoods, supporting robust inference in sparse regimes, alongside learned latent-variable distributions that adaptively capture heterogeneity. Covariate incorporation is realized through the encoder, allowing contextual factors to flexibly modulate latent parameters beyond conventional proportional hazard formulations or cohort-based modeling. Extensions include the use of LSTM or Transformer-based encoders to exploit full transaction histories where richer temporal or contextual structures justify increased model complexity.

Estimation and Prediction

Training is conducted via maximization of the Evidence Lower Bound (ELBO), balancing data reconstruction (log-likelihood) with regularization (KL divergence to prior), supported by stochastic gradient descent and reparameterizable Gamma sampling. The architecture is designed for scalability: the encoder/decoder are compact feedforward networks, and prediction is performed by Monte Carlo simulation over latent variables for each customer, with dropout and inter-purchase times sampled conditioned on the estimated latent parameters.

The model is parsimonious—requiring only RFM summary statistics—yet generalizes to richer input data and covariate structures. The simulation-based prediction routine efficiently generates full distributions of future customer revenue, supporting both point prediction and uncertainty quantification suitable for operational deployment.

Empirical Evaluation

Empirical validation is conducted across three public retail datasets embodying the diversity and difficulty of real-world customer base forecasting: high heterogeneity, substantial zero-repeat rates, and widely varying transaction values and frequencies. CLVAE is benchmarked against (i) canonical Pareto/NBD + GG baselines, (ii) autoregressive LSTM + GG deep learning models, and (iii) joint likelihood models with increased structural flexibility.

Results across out-of-sample horizons (52–208 weeks) consistently show that CLVAE improves prediction accuracy (RMSE) compared to all baselines, particularly as forecast horizon lengthens and uncertainty compounds. For example, in Retailer A, CLVAE yields a mean RMSE of 352.4 at 208 weeks versus 459.58 for the classical baseline. The improvement is robust to the absence of contextual covariates and persists across datasets with varied revenue dispersion.

In practical case studies where cohort information (acquisition month) is available, CLVAE’s approach to covariate incorporation delivers prediction gains equivalent to (or better than) cohort-specific modeling, without operational overhead or vulnerability in low-data cohorts. The model flexibly propagates cohort effects through all latent process parameters, outperforming not only standard covariate-enhanced baselines but also deep learning models with engineered features, especially on long-term horizons.

Theoretical and Practical Implications

CLVAE represents a formal template for integrating econometric process models into deep generative frameworks. By embedding the structural likelihoods of classical customer base analysis within the VAE, the approach achieves both stability in sparse transactional regimes and systematic improvements in latent heterogeneity modeling via end-to-end representation learning.

Practically, the single-model deployment workflow increases operational efficiency, reduces technical debt relative to maintaining multiple cohort-specific models, and supports scaling to large customer bases. The flexible covariate handling positions the model for broad applicability, including privacy-constrained regimes where only transactional data are available, as well as contexts with rich customer descriptors.

Theoretically, CLVAE bridges the divide between parametric process modeling and nonparametric latent-variable inference, preserving economically meaningful primitives while enabling latent space discovery and nonlinear dependence structures. The approach sets the stage for further extensions: incorporation of time-varying covariates, modeling intra-customer correlations, and integration with advanced sequence encoders as data richness warrants.

Future Directions

Promising future developments include:

- Time-varying covariates: Extension to handle seasonality and calendar effects via dynamic latent variables, enhancing calendar-specific forecasting.

- Combinatorial process extensions: Modeling purchase regularity, intra-customer correlation, or high-dimensional spend via more complex decoder likelihoods.

- Enhanced encoder architectures: Adoption of transformer-based or attention-driven encoders for full transaction history modeling in regimes with strong temporal structure.

- Operational scaling: Algorithmic refinement for real-time inference, integration with A/B testing platforms, and automated hyperparameter tuning to minimize manual intervention.

These directions leverage the core premise that VAEs can house domain-specific process structure without sacrificing flexibility, supporting advances in AI-driven revenue management.

Conclusion

The CLVAE delivers improved, robust, and scalable customer revenue forecasting by generalizing the longstanding Pareto/NBD + GG paradigm within a variational autoencoder framework. It systematically outperforms both traditional econometric and deep learning baselines, maintains operational parsimony, and offers a pathway for embedding representation learning in econometrically meaningful contexts. The approach expands the toolkit for researchers and practitioners, facilitating long-horizon forecasting under irregular and heterogeneous conditions with theoretical rigor and practical utility.