- The paper demonstrates that only one in six LPs achieves non-negative PnL in CLMMs using detailed WETH/USD transaction data.

- It introduces a novel PnL reconstruction algorithm and the win-score metric to distinguish transient gains from persistent profitability.

- The study reveals that successful LPs center liquidity around current prices and trigger exits based on capital return thresholds.

Liquidity Provision in CLMMs: Empirical Evidence and Position Taxonomy

Context and Motivation

Concentrated Liquidity Market Makers (CLMMs), such as Uniswap V3 and its protocol derivatives, represent an evolution in decentralized exchange (DEX) design, enabling liquidity providers (LPs) to allocate capital within targeted price intervals, thus improving capital efficiency relative to prior AMM designs. This transition converts liquidity provision from a passive to a highly active, risk-managed endeavor, necessitating careful range management, frequent repositioning, and the adoption of more sophisticated trading strategies. Despite the elevated complexity and risk sensitivity, open questions persist regarding the standalone profitability of liquidity provision in CLMMs, the behavior and organization of LPs, and the structural components underlying LP profitability.

Figure 1: Decentralized exchanges occupy a central position within the blockchain application landscape, mediating liquidity flows across DeFi protocols.

Methodological Innovations

The paper leverages historical, transaction-level data from WETH/USD pools on the Base chain across Uniswap, Aerodrome, PancakeSwap, and SushiSwap. The analytic workflow involves reconstructing granular LP position paths within each pool by chronologically matching liquidity "mint," "burn," and "collect" operations and associating them with pool price movements derived from swap events.

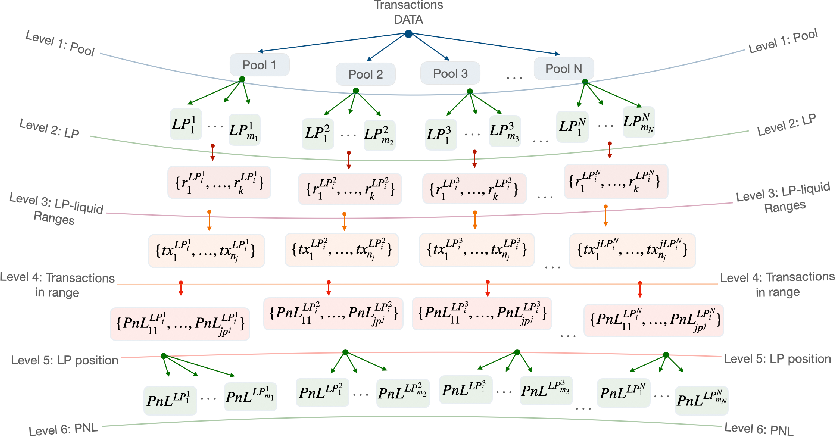

A pivotal contribution is the introduction of a novel LP PnL (profit and loss) reconstruction algorithm, which resolves the inherent frictions arising from the asynchronous realization of liquidity removal and fee withdrawal—effectively modeling the dynamic balance of each LP's active and closed positions over arbitrary sets of price intervals.

Figure 2: Schematic outlining LP PnL construction via chronological matching of mint and (burn+, collect) transaction pairs, incorporating pool price dynamics at each event.

In addition to PnL, the authors design the "win-score" metric ω, capturing the temporal consistency of an LP's profitability by integrating normalized positive and negative cumulative PnL over the active interval, rather than focusing purely on terminal profit. This allows for distinguishing LPs with transient positive PnL from those demonstrating persistent outperformance.

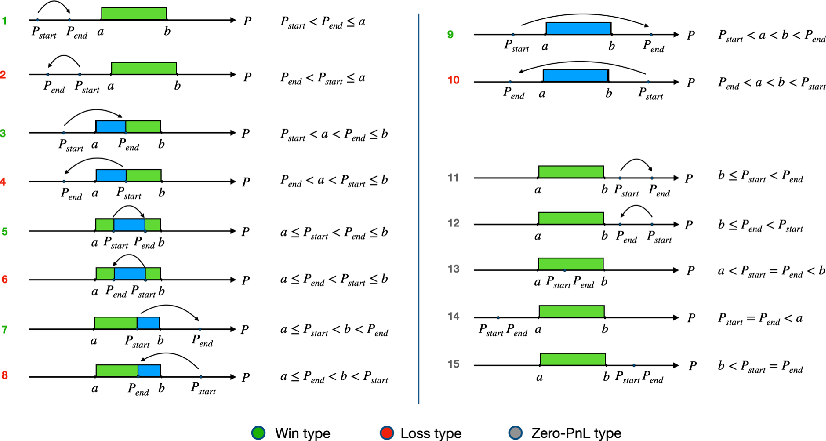

A comprehensive taxonomy of 15 position types is developed, classified by the opening and closing pool prices relative to the chosen liquidity range. This design enables fine-grained attribution of realized PnL to micro-structural trading behaviors.

Figure 3: Taxonomy of LP position types based on profitability and relation to range boundaries.

Key Empirical Results

Standalone Profitability and LP Segmentation

The study's most striking finding is that only approximately one in six LPs achieves non-negative PnL in the analyzed WETH/USD pools during the study period, and only one in seven displays persistent profit consistency as measured by ω>0.5. This pattern holds across major protocols (Uniswap, Aerodrome) and deteriorates for less liquid venues, directly contradicting the expectation that most LPs are meaningfully compensated for their capital exposure.

There is a discernible dichotomy between platform attractiveness (Uniswap draws a higher share of unique LPs) and intensity of liquidity operations (Aerodrome receives the majority of transaction volume). These differences likely reflect varying participant sophistication and strategy design.

LP Behavior: Mono-LPs vs. Multi-LPs

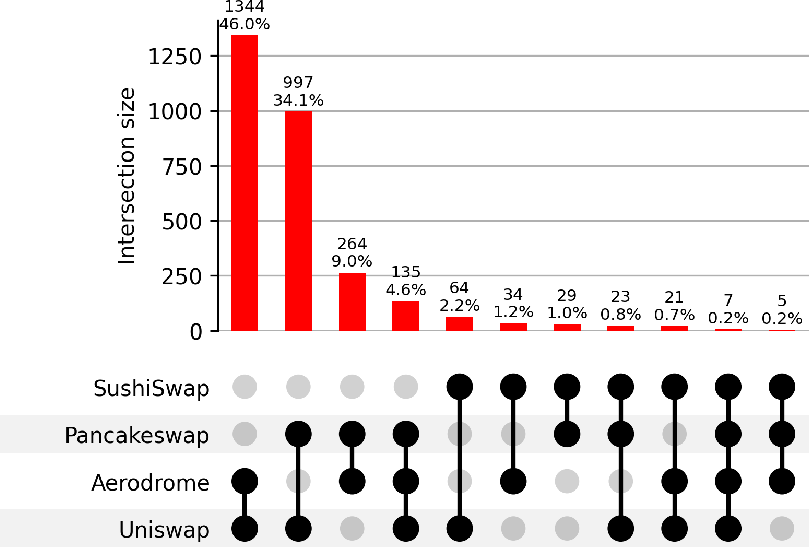

Approximately 10% of active LPs provide liquidity across multiple pools ("multi-LPs"). However, increasing cross-pool participation does not equate to greater success. Only 29.5% of multi-LPs are consistently profitable in at least one pool, with the fraction falling precipitously as more pools are simultaneously targeted.

Figure 4: Distribution and connectivity patterns of multi-LPs across major WETH/USD pools, highlighting predominant cross-pool migration.

Position Taxonomy and Dominant Strategies

Analysis of position types reveals over 90% of LP transactions and minted capital are concentrated in Type 5–6 positions—i.e., where both entry and exit prices remain within the originally selected range. Notably, successful LPs typically center their liquidity range on the current price, with the price at minting close to the midpoint of the chosen interval.

The empirical delta metrics indicate that positions are usually closed well before the price traverses the entire range. In Type 5 (in-range) positions, successful LPs generally close after the price moves just 8% of the range width, suggesting a practical deviation from classical τ-reset boundary-based strategies. Rather, position closure tends to be triggered by achieving a capital return threshold, closer to a τ+η-style strategy as opposed to waiting for adverse events or full range traversal.

A secondary observation is the capital allocation pattern: while successful LPs (in Types 3, 5, and 7) prefer relatively wide liquidity ranges (100–1000 USDC), the majority of transaction count and TVL is concentrated in narrow intervals (<10 USDC), especially for dominant in-range profitable positions.

Implications for DeFi Microstructure

The rigorous data-driven refutation of the view that LPs, as a class, are systematically rewarded highlights significant friction, including inventory risk and impermanent loss, that cannot be adequately counteracted by pool fees alone in current CLMM design. The results imply that sustainable LP participation on major DEXs is likely motivated by external portfolio considerations, off-chain hedging, optimized cross-pool/CEFI–DeFi arbitrage, or non-economic factors (e.g., governance incentives).

The identification of a substantial multi-LP class, alongside their limited aggregate success, points towards the proliferation of more sophisticated or automated strategies, but also underscores the systemic challenges in attaining profitability via simple liquidity provision in isolation.

On the microstructural plane, the evidence that position closure is generally decoupled from range boundary events suggests that successful LPs increasingly operate in a regime where dynamic management and risk-adjusted exit criteria are critical. This trend aligns the practice of liquidity provision more closely with traditional active trading and market making, necessitating real-time analytics, inventory control, and potentially ML-driven or algorithmic strategies to remain competitive.

Future Outlook and Research Directions

Given the persistent unprofitability for the majority of standalone LPs under analyzed conditions, future research should interrogate the drivers behind continued capital inflow to CLMMs. Key questions include quantifying the role of hedging, evaluating the effectiveness of programmatic repositioning strategies, and modeling the equilibrium liquidity profile using Nash/game-theoretic approaches that reflect interaction among increasingly sophisticated agent classes.

The observed divergence between transaction-based LP activity and realized PnL also motivates investigation into protocol-level incentives, alternative fee designs, and the impact of endogenous market volatility and external liquidity mining programs on market microstructure efficacy.

Conclusion

By reconstructing PnL and granular position histories from comprehensive on-chain data, this study delivers a robust empirical foundation for understanding the microeconomics of liquidity provision in CLMMs. Standalone liquidity provision is persistently unprofitable for the majority of participants, with consistently successful outcomes restricted to a small minority utilizing dynamic, target-driven exit strategies, often in ranges centered on the spot price. The results call for a reevaluation of LP incentives, point towards increased market sophistication, and highlight the centrality of active strategy design—inviting both protocol designers and researchers to revisit the presuppositions underpinning current AMM architectures.