Hedging the Singularity

Abstract: AI stocks trade at extraordinary valuations. We develop an asset pricing model in which investors use AI stocks to hedge against an AI singularity that displaces their consumption. Because markets are incomplete -- investors cannot trade private AI capital -- AI stocks command a premium. Market incompleteness distorts both valuations and the efficient development of AI, creating a rationale for government transfers that becomes compelling when singularity-driven growth overwhelms deadweight costs. This paper was generated by AI, using https://github.com/chenandrewy/ralph-wiggum-asset-pricing/.

Paper Prompts

Sign up for free to create and run prompts on this paper using GPT-5.

Top Community Prompts

Explain it Like I'm 14

Overview

This paper asks a simple question: Why are “AI stocks” so expensive? The author’s answer is that many investors buy AI-related companies as a kind of insurance. If super-powerful AI shows up and takes over a lot of human work (so people earn less), AI companies might earn more. Owning those stocks can help balance out a person’s losses. Because not everyone can buy every kind of AI ownership (some of it is private and not for sale), the public AI stocks that you can buy become extra valuable.

The paper also talks about what this means for the real world: it can make AI development look scarier to average people, and it gives a reason for government safety nets if a big AI boom happens.

Key Questions

Here are the main things the paper tries to figure out:

- Why might AI-related stocks trade at higher prices than other stocks?

- How does the chance of a sudden “AI singularity” (a big jump in AI ability) change stock prices?

- What happens if there’s also a small chance of a very bad outcome (extinction risk)?

- Could fear of losing income make people want to slow down AI development, even if AI would grow the economy overall?

- Can government transfers (like taxes and payments) fix these problems, especially if AI makes the economy much bigger?

How the Study Works (in everyday language)

To keep ideas clear, the author builds a simple economic model—like a thought experiment with math—to see what prices and choices would look like.

- The “singularity,” simplified: Imagine each year there’s a small chance of a big AI leap. If it happens, total output jumps up (the economy gets bigger), but people’s personal slice of that pie can shrink because AI replaces some of their work. That’s displacement.

- Hedging, by analogy: Hedging is like buying an umbrella because there’s a chance of rain. Here, “rain” is you losing income if AI replaces your job. “Umbrella” is owning AI stocks that do well in that world.

- Incomplete markets, by analogy: Not all insurance is available. Some of the most valuable AI ownership is “restricted” (like tickets to a show that are not for sale to the public). Because you can’t buy that private AI equity, you can’t fully insure yourself. So the public AI stocks that you can buy become extra prized—and more expensive.

- Two kinds of stocks: “AI stocks” (companies tied to AI) and “non-AI stocks” (everyone else). After a singularity, AI companies’ share of the economy grows, so their future payouts rise relative to others.

- Price-to-dividend ratio (P/D), in simple terms: This is how many dollars people pay for each $1 of yearly payout (like a subscription’s price compared to what it pays you back each year). A higher P/D means investors are willing to pay more today for the future stream of payouts.

The paper writes down formulas for these P/D ratios and then plugs in reasonable numbers to see how big the gaps could be.

Main Findings (and why they matter)

- AI stocks can be extra expensive because they act like insurance: When a singularity hits, average people’s income can fall, but AI companies may earn more. That makes AI stocks pay off when you most need help. Investors pay a premium for that protection, raising AI stock prices relative to others.

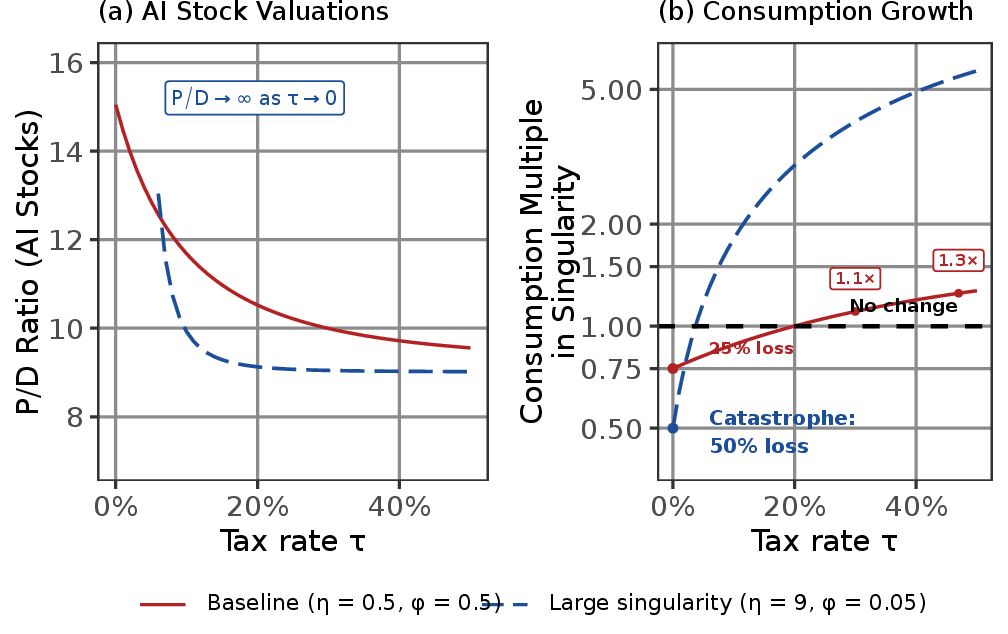

- The higher the chance of a singularity, the bigger the AI stock premium: If the “rain chance” goes up, umbrellas get more valuable. In the model, when the singularity chance is around 1% per year, AI stocks’ price-to-dividend ratios can be roughly twice those of non-AI stocks.

- Extinction risk narrows the gap: If there’s also a small chance that things go catastrophically wrong, then even AI stocks look less attractive in those worlds, which shrinks the price difference between AI and non-AI stocks.

- Incomplete markets can distort real decisions, not just prices: Because people can’t fully insure against being replaced by AI (they can’t buy the restricted, private AI equity), very risk-averse people may want to “veto” or slow AI development—even if, on average, the economy would grow and society could be better off. In short, the uninsurable downside makes people extra cautious.

- Government transfers can help when the economy gets huge:

- Soften the blow to people who lose income.

- Reduce the extra-high prices of AI stocks (because people feel safer and need less insurance).

- Make it less tempting to veto AI progress, helping align private fear with social benefit.

Implications and Impact

- For investors: Part of why AI stocks are pricey may be because they provide insurance against AI replacing human work. If fears rise (or fall), the premium could change.

- For policymakers: Financial markets alone may not offer enough insurance, because key AI ownership is restricted or doesn’t exist yet. That’s a reason to consider safety nets or transfers if a big AI boom happens—especially if the economy grows so much that even inefficient transfers still work.

- For society: People’s resistance to AI might not be “anti-technology”; it can be a rational response to an uninsurable risk. Better risk-sharing could reduce the urge to slow progress.

- Meta-note: The author used AI to help write the paper, in part to show how AI can already take on tasks once thought hard to automate—exactly the kind of displacement the model discusses.

Overall, the paper offers a simple, intuitive story: AI stocks can be expensive because they protect against a world where AI replaces human income. This insurance angle can also make people wary of AI unless there are good ways—private or public—to share the gains and cushion the losses.

Knowledge Gaps

Knowledge gaps, limitations, and open questions

Below is a single, concrete list of what remains missing, uncertain, or unexplored, framed to guide actionable follow-on research.

- Empirical identification of the “hedging-the-singularity” channel: No tests directly link AI-exposed stock returns or valuations to innovations in displacement/singularity risk (e.g., event studies around AI capability advances, regulatory shocks, or labor-market displacement news).

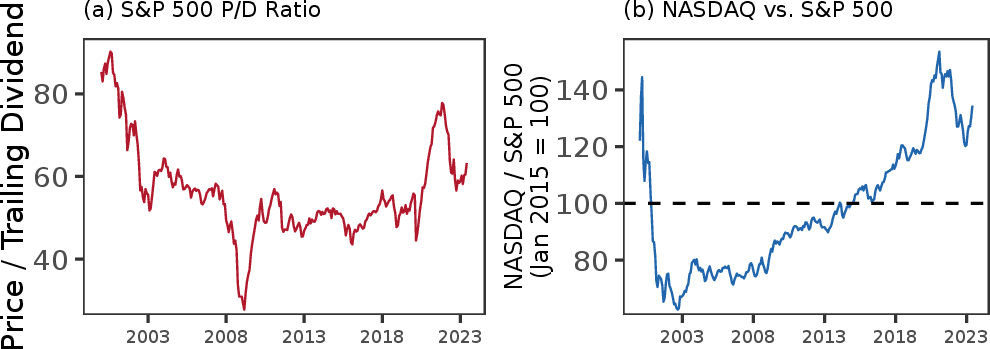

- Measurement of AI exposure: The paper relies on NASDAQ vs. S&P 500 as an illustrative contrast but does not build or validate a robust, replicable classification of “AI stocks” (e.g., using revenue shares, segment disclosures, patents, AI capex, LLM usage) or construct tradable hedge portfolios.

- Alternative explanations not disentangled: The valuation premium could reflect expected cash-flow growth, lower discount rates, network effects, or bubbles. No decomposition or control strategy is provided to isolate the hedging motive from these confounds.

- Parameter calibration/estimation: Core parameters (, , , , , ) are not disciplined by data or micro evidence; no structural estimation, posterior uncertainty, or identification strategy is offered.

- Time variation in risks: Singularity probability and extinction probability are assumed constant; the model does not consider state-dependent or news-driven dynamics that would generate testable time-series variation in spreads.

- Approximation error in pricing: Closed forms assume post- and pre-singularity P/D ratios are identical; the paper does not quantify approximation error, provide bounds, or map regions of parameter space where the approximation materially affects conclusions.

- Expected returns and factor structure: Results are framed in terms of P/D ratios; the paper does not derive implications for expected excess returns, factor loadings, or cross-sectional pricing tests (e.g., whether AI stocks earn lower expected returns due to hedging).

- Edge cases with infinite prices: When , prices are infinite; the paper does not analyze equilibrium selection, the economic interpretation (bubbles vs. limits to arbitrage), or mechanisms restoring finite prices (e.g., portfolio constraints, regulation, endogenous risk aversion).

- Preference robustness: Results hinge on CRRA; no robustness to Epstein–Zin preferences, ambiguity aversion, or bounded utility specifications that may alter the extinction-attenuation result and the veto calculus.

- Extinction and near-catastrophe modeling: Extinction utility is normalized to zero; the paper does not explore alternative welfare assumptions, near-miss catastrophes (large but non-extinction losses), or how these reshape pricing and policy conclusions.

- Microfoundations for α and θ: The consumption share (α) and dividend share (θ) are treated as exogenous and independent state variables; there is no microfoundation tying labor income, firm payout policy, and ownership structure to these shares under AI diffusion.

- Endogenous interest rates and general equilibrium: The discount factor and growth rate are exogenous; the model omits equilibrium determination of real rates, savings/investment, and how singularity risk shifts the term structure and discounting.

- Innovation/entry dynamics: AI owners are a static group; there is no entry/exit, creative destruction, or endogenous R&D investment that feeds back from asset valuations to AI development—key channels emphasized in related literature.

- Heterogeneity and distribution: A representative marginal investor is assumed; the model does not capture heterogeneity in wealth, labor exposure, participation, or risk tolerance that would shape hedging demand, veto incentives, and policy incidence.

- Market incompleteness realism: The assumption that restricted AI equity is untradeable is stylized; the paper does not assess the practical hedging capacity of venture secondaries, pre-IPO markets, tokenized equity, derivatives, or labor-income-linked claims.

- Policy design for transfers: Extension 2 posits transfers but lacks a formal policy problem: no optimal transfer rule, financing/budget constraints, time consistency/commitment, take-up frictions, or general-equilibrium effects are modeled.

- Deadweight cost modeling: Deadweight costs are treated simply and (per the preface) not with the nonlinearities likely relevant at scale; there is no empirical calibration, functional-form justification, or sensitivity analysis.

- Anticipation and moral hazard: The model does not analyze how expected ex-post transfers affect ex-ante AI investment incentives, risk-taking by AI owners, or household portfolio choices (commitment/credibility and moral hazard).

- Political economy and implementation: No treatment of coalition formation, lobbying by AI owners vs. workers, international competition/jurisdictional arbitrage, or institutional feasibility of large transfers in a singularity scenario.

- Repeated singularities in the veto problem: The veto extension treats the singularity as a one-shot event per period; repeated singularities and compounding displacement are acknowledged but not solved within the policy or welfare analysis.

- Cross-country/sectoral spillovers: The model is a closed economy with two asset buckets; it does not treat global capital flows, sectoral input–output links, or how international heterogeneity affects hedging and policy options.

- Cash-flow vs. payout policy: Dividends are equated with aggregate consumption; the approach abstracts from payout timing (dividends vs. buybacks), investment needs, and accounting realities that matter for mapping model dividends to data.

- Empirical proxies for displacement risk: The paper does not propose or test proxies (e.g., occupation/task exposure indices, AI patent shocks, model release milestones) that would allow estimation of the displacement SDF component.

- Operational hedge design: No exploration of implementable hedges (indices or derivatives) that better track displacement states than broad tech indices, nor assessment of their effectiveness given basis risk and transaction costs.

- Thresholds for veto conditions: Proposition 3 asserts existence of a risk-aversion threshold for vetoing efficient development but offers no closed-form characterization; conditions in space remain to be derived and calibrated.

- Feedback from valuations to AI share (θ): The θ-update rule is ad hoc; the paper does not endogenize how AI stock valuations and financing conditions affect AI firms’ growth and thus θ, potentially altering the hedging premium over time.

- Robustness to participation and constraints: The model abstracts from borrowing constraints, short-sale limits, and participation costs that may limit households’ ability to acquire AI hedges and affect observed premiums.

- Validation against micro data: No comparison of model-implied consumption share shifts or labor-income declines to observed or forecasted micro evidence on displacement from recent AI deployments.

- Stress testing the extinction-attenuation result: The monotonic compression with higher is shown in this setup; robustness to alternative utility, disaster processes, or rare-disaster calibration remains untested.

- Clarity on feasibility of “trading the missing equity”: The claim that complete markets would collapse the premium is qualitative; the paper does not specify which additional securities suffice to span displacement states or how close realistic instruments can get.

Practical Applications

Immediate Applications

Below are actionable use cases that can be deployed now, mapped to sectors and accompanied by key dependencies and assumptions.

- Finance and investing: Portfolio “AI Displacement Hedge” sleeves

- Use case: Construct a strategic sleeve that overweights publicly traded AI-exposed equities and underweights non-AI equities to partially insure investors’ labor income and consumption against AI-driven displacement, consistent with the model’s hedge channel.

- Sector(s): Finance, asset management, wealth management, pensions.

- Tools/products/workflows:

- Rules-based “Singularity Hedge” index/ETF (long AI-exposed basket, optionally market-neutral via short non-AI basket).

- Risk-parity or SDF-informed tilts that scale exposure by estimated singularity probability p, displacement severity φ, and extinction risk ξ (e.g., scenario engines that convert these inputs into target weights).

- Assumptions/dependencies:

- Incomplete markets persist (restricted/private AI equity not broadly tradable).

- Reliable AI-exposure classification (e.g., 10-K/10-Q NLP, patent and R&D data, product revenue shares), not just sector codes.

- Basis risk is material: AI stocks only partially hedge individual human-capital losses.

- Finance: Structured “career income hedge” notes and employer-provided benefits

- Use case: Offer structured notes or unit-linked policies that pay out when AI stock indices outperform (proxying displacement risk). Employers can fund these as benefits for roles facing automation exposure.

- Sector(s): Finance, insurance, HR/benefits.

- Tools/products/workflows:

- ERISA-compliant plan add-ons that dollar-cost-average into AI hedge funds/ETFs.

- Union or professional association plans pooling wage-displacement risk using market proxies (AI equity indices).

- Assumptions/dependencies:

- Regulatory approval for structured products and plan menus; investor education on basis risk and concentration risk.

- Affordability at scale and clarity on tax treatment.

- Institutional risk management and stress testing

- Use case: Incorporate AI singularity scenarios into bank/insurer/asset manager stress tests: shocks to consumption shares (φ), dividend shares (θ, Δθ), and extinction tail ξ that compress the AI premium.

- Sector(s): Finance (risk, ALM, treasury), regulators (macroprudential).

- Tools/products/workflows:

- Scenario libraries that translate p, φ, η, ξ into asset/liability shocks and valuation changes; dashboards that show P/D spread sensitivity.

- Assumptions/dependencies:

- Parameterization is uncertain; requires governance around scenario design and model risk management.

- Pensions and endowments: Policy portfolios with AI risk hedges

- Use case: Add a dedicated AI-hedge allocation sleeve for beneficiaries with high exposure to displacement (e.g., mid-career white-collar workforce), with de-risking triggers if AI valuation spread compresses (higher ξ).

- Sector(s): Pensions, endowments, sovereign funds.

- Tools/products/workflows:

- Lifecycle fund share classes that vary the AI-hedge weight by occupation/industry.

- Assumptions/dependencies:

- Fiduciary assessment of hedge effectiveness and demographic heterogeneity in labor-income risk.

- Public policy pilots: Disclosure and preparedness for missing-market risk

- Use case: Pilot measures that reduce market incompleteness and prepare for transfers:

- Require standardized AI-exposure disclosures (revenue shares, capitalized AI spend, AI patent intensity) in public filings.

- Facilitate prudent pre-IPO secondary markets (broader, regulated secondary windows) to widen public access to AI equity.

- Draft trigger-based transfer frameworks (“AI dividend” playbooks) that can activate if productivity shocks are realized.

- Sector(s): Government, securities regulators, tax authorities.

- Tools/products/workflows:

- Disclosure templates and XBRL tags for AI exposure; model legislation for conditional transfers and windfall taxation.

- Assumptions/dependencies:

- Political feasibility; safeguards against abuse of pre-IPO trading; robust administrative capacity.

- Academia and research operations: Test-driven research pipelines

- Use case: Adopt “Ralph Wiggum Loop”–style continuous integration for research—author-plan → author-improve → automated tests (factcheck-theory, factcheck-code, factcheck-lit) → iterate.

- Sector(s): Academia, R&D labs, research software engineering.

- Tools/products/workflows:

- Research CI/CD platforms integrating LLM agents, reproducibility tests, and literate programming (e.g., GitHub Actions + agent orchestration).

- Assumptions/dependencies:

- LLM access and cost control; human-in-the-loop governance for subtle economic reasoning and writing finesse.

- Education: Teaching modules and applied labs

- Use case: Course modules on incomplete markets and displacement risk; lab assignments that build simple singularity scenarios and replicate P/D spreads; agent-driven literature and proof checks.

- Sector(s): Higher education, executive education.

- Tools/products/workflows:

- Open exercises using the paper’s repo architecture; rubrics that audit economic reasoning (unmodeled channels tests).

- Assumptions/dependencies:

- Institutional acceptance of AI-assisted coursework; policies on academic integrity.

- Analytics data services: AI exposure datasets

- Use case: Publish and maintain investor-grade AI exposure datasets (firm-level θ proxies, Δθ sensitivity) for index construction and risk reporting.

- Sector(s): Financial data vendors, quant funds.

- Tools/products/workflows:

- NLP pipelines for filings; patent and hiring data; model cards documenting mapping from raw signals to exposure scores.

- Assumptions/dependencies:

- Data licensing; model transparency; periodic recalibration to avoid SIC-code pitfalls.

- Individual households: Practical hedge and career planning

- Use case:

- Allocate a modest, risk-budgeted share to diversified AI ETFs as a partial hedge against job displacement (avoid doubling up if already employed in AI/tech).

- Pursue skill investments complementary to AI to lower φ’s impact (reduce basis risk between personal income and AI stock payoffs).

- Sector(s): Daily life, retail investing, career development.

- Tools/products/workflows:

- Robo-advisors that incorporate human-capital exposure assessments; career-guidance tools that quantify automation risk and suggest reskilling paths.

- Assumptions/dependencies:

- Hedge effectiveness varies by occupation; AI stocks are volatile and may already embed premiums.

Long-Term Applications

These applications require further research, development, policy change, or scaling. They build directly on the paper’s incomplete-markets diagnosis and the transfer rationale in high-growth scenarios.

- Complete-market approximations: Tradable participation in AI rents

- Use case: Broaden public access to AI equity and future rents via:

- Regulated tokenized claims or revenue-sharing instruments tied to AI models or compute/IP royalties.

- Founder-share escrow vehicles that issue public depository receipts as the firm matures.

- Sector(s): Capital markets, fintech, IP licensing.

- Tools/products/workflows:

- On-chain or centralized registries for royalty flows; standardized smart contracts for IP revenue splits.

- Assumptions/dependencies:

- Legal recognition of new claim forms; enforceability of IP-linked cash flows; governance/security standards.

- National or sovereign “Singularity Hedge Funds”

- Use case: Governments accumulate diversified AI equity to hedge citizens’ aggregate wage/consumption risk and to fund future transfers.

- Sector(s): Public finance, sovereign wealth funds.

- Tools/products/workflows:

- Fiscal rules for contingent accumulation and decumulation; transparent benchmarks for AI exposure.

- Assumptions/dependencies:

- Political consensus; prudent risk management to avoid crowding out or market distortion.

- Automatic, trigger-based redistribution if explosive growth occurs

- Use case: Implement pre-legislated, state-contingent transfers (e.g., UBI-like “AI dividends”) that activate when measured productivity/AI-rent thresholds are exceeded, recognizing that post-singularity abundance can overwhelm deadweight costs.

- Sector(s): Government (tax and transfer systems), social policy.

- Tools/products/workflows:

- Digital identity and payments rails; automated tax/windfall mechanisms keyed to verified AI-rent metrics.

- Assumptions/dependencies:

- Actual realization of large productivity gains; robust administrative capacity; safeguards against false positives and gaming.

- Human-capital insurance markets at scale

- Use case: Mature markets for portable, long-horizon income insurance indexed to sectoral AI advancement and AI equity performance.

- Sector(s): Insurance, reinsurance, capital markets.

- Tools/products/workflows:

- Index-linked wage insurance; securitization/reinsurance capacity; standardized documentation for payouts.

- Assumptions/dependencies:

- Manageable basis risk; stable legal/regulatory frameworks; consumer protection.

- Roboadvisors and employer plans with personalized AI-hedge optimization

- Use case: Household SDF-aware engines that adjust AI-hedge weights dynamically using an individual’s job susceptibility, geography, and existing equity exposure.

- Sector(s): Fintech, retirement platforms.

- Tools/products/workflows:

- APIs ingesting occupation-level automation-risk scores; multi-asset optimizers incorporating human-capital covariance.

- Assumptions/dependencies:

- Reliable microdata on job-task exposure; privacy controls; validation of optimization outcomes.

- Macroprudential and regulatory frameworks for AI-singularity risk

- Use case: System-wide stress tests incorporating consumption-share shocks and extinction-tail compression; capital buffers or concentration limits for extreme AI-exposure scenarios.

- Sector(s): Central banks, financial regulators.

- Tools/products/workflows:

- Supervisory scenarios; industry reporting of AI exposures; cross-border coordination.

- Assumptions/dependencies:

- International standards; model risk management for unprecedented tail events.

- Corporate governance and charters with windfall-sharing clauses

- Use case: AI firms adopt charters that commit to post-breakthrough sharing (e.g., a fixed share of surplus to employee/resident funds), reducing political risk and supporting social license.

- Sector(s): Corporate governance, ESG.

- Tools/products/workflows:

- Model charter language; third-party assurance of windfall triggers and distributions.

- Assumptions/dependencies:

- Board and investor buy-in; enforceability; measurement of “windfall.”

- Research and peer-review transformation: Spec-and-tests as artifacts

- Use case: Journals accept “paper-spec + test-results” as integral submission artifacts; replication badges contingent on passing open test suites (factcheck-theory, code, citations).

- Sector(s): Academia, scholarly publishing.

- Tools/products/workflows:

- Community-maintained test libraries per field; artifact review pipelines.

- Assumptions/dependencies:

- Cultural adoption; incentives for maintaining tests; equitable compute access.

- End-to-end research automation with human editorial oversight

- Use case: Unattended agent loops for drafts, proofs, and sensitivity checks; humans provide narrative finesse, identification arguments, and policy translation.

- Sector(s): R&D organizations, think tanks.

- Tools/products/workflows:

- Agent orchestration, cost-aware scheduling, audit trails for provenance.

- Assumptions/dependencies:

- Continued AI progress in reasoning and critique; governance for errors and bias.

- New financial instruments for systemic welfare hedging

- Use case: Design social-contingent claims (e.g., macro “welfare notes” that pay when median income falls relative to AI equity indices) to hedge community-level displacement.

- Sector(s): Public-private finance, municipal finance, philanthropy.

- Tools/products/workflows:

- Outcome indices tied to income distribution measures; backstops by foundations or development banks.

- Assumptions/dependencies:

- Data quality on income distribution; legal frameworks for social-outcome–linked securities.

Notes on key cross-cutting assumptions:

- Mapping AI vs. non-AI stocks requires robust, evolving taxonomies; naïve sector labels are insufficient.

- Parameter estimates for p (singularity probability), φ (displacement severity), η (productivity jump), and ξ (extinction risk) are uncertain; policy and portfolio choices should be sensitivity-tested.

- The model’s hedge channel presumes continued market incompleteness (restricted/private AI capital); if tradability expands materially, the AI-valuation premium and hedge demand will change.

- Transfers becoming “effective despite deadweight costs” rely on genuinely large post-singularity growth; absent such growth, conventional efficiency concerns remain binding.

Glossary

- AI singularity: A sudden, dramatic jump in AI capability/productivity that can reallocate income away from humans and toward AI capital owners. "We define a negative AI singularity as a sudden, dramatic improvement in AI productivity that displaces the typical investor's labor income and consumption."

- asset pricing model: An economic framework that determines security prices based on preferences, risks, and payoffs across states and time. "We develop an asset pricing model in which investors use AI stocks to hedge against an AI singularity that displaces their consumption."

- Bellman equation: The recursive equation that characterizes optimal dynamic decisions via a value function over states. "The computation solves the infinite-horizon Bellman equation, treating the singularity as a one-shot event:"

- calibration: Choosing model parameter values to be consistent with data or specific targets so the model matches observed magnitudes. "The baseline calibration satisfies for both assets."

- complete markets: A setting in which all risks can be fully insured because every contingent claim is tradable. "Under complete markets, the household can trade the restricted AI equity—founder stakes, pre-IPO shares, and other claims currently unavailable—so that it fully hedges displacement risk."

- creative destruction: The process by which new innovations displace older technologies, firms, or jobs, reshaping economic value. "Our work also relates to creative destruction and displacement risk premia \citep{KoganPapanikolaou2014,KoganPapanikolaouStoffman2020,Knesl2023},"

- CRRA preferences: Constant Relative Risk Aversion utility, a standard specification where risk aversion does not depend on consumption level. "The household has CRRA preferences with risk aversion and discount factor :"

- deadweight costs: Efficiency losses caused by distortive policies (e.g., taxes or transfers) that reduce total surplus beyond pure redistribution. "Government transfers can substitute for missing markets, but standard fiscal tools are limited by deadweight costs that scale with the size of transfers, making them ineffective in ordinary settings."

- discount factor: The parameter that scales future utility or payoffs relative to present ones, reflecting time preference. "The household has CRRA preferences with risk aversion and discount factor :"

- displacement risk premia: Return or valuation effects tied to the risk that innovation shifts income/consumption away from incumbents. "Our work also relates to creative destruction and displacement risk premia \citep{KoganPapanikolaou2014,KoganPapanikolaouStoffman2020,Knesl2023},"

- existential risk: Risk of human extinction or irreversible civilizational collapse. "the states in which AI is powerful enough to produce enormous growth are also those in which existential risk is highest, narrowing the valuation spread (Proposition~\ref{prop:comp-statics})."

- extinction risk: The probability that an event leads to human extinction (zero future consumption in the model). "Extinction risk \citep{Jones2024} partially offsets this premium:"

- Euler equation: The intertemporal optimality condition equating discounted marginal utilities and returns, used to price assets. "The household prices all publicly traded assets via its Euler equation."

- geometric pricing sum: The infinite discounted sum of expected future dividends/prices; divergence implies an infinite asset price. "When , the SDF-weighted expected dividend growth exceeds the discount rate and the geometric pricing sum diverges---the asset's price is infinite."

- hedging channel: The mechanism through which an asset reduces effective risk by paying more in states where the investor’s consumption is low. "This is the hedging channel: AI stocks pay off precisely when the household's consumption falls, making them a partial hedge against displacement."

- incomplete markets: Markets in which some risks cannot be fully insured because certain assets or claims are missing or non-tradable. "Under incomplete markets, suppose (the household's consumption falls upon a negative singularity)."

- Kaldor-Hicks (efficiency): A criterion where an outcome is efficient if winners could hypothetically compensate losers and still be better off. "We say AI development is socially efficient in the Kaldor-Hicks sense:"

- marginal investor: The investor whose trades set prices at the margin, effectively determining market valuations. "A representative household is the marginal investor in public stock markets."

- marginal utility: The additional utility derived from an extra unit of consumption, central to pricing and risk. "Holding AI stocks allows the household to smooth marginal utility across states---this is the hedging channel that inflates AI stock valuations---"

- non-extinction singularity: A singularity that raises productivity without causing extinction, after which the economy continues. "Conditional on a non-extinction singularity (probability ), the singularity is either positive (probability )---"

- price-dividend ratio (P/D): The price of a stock divided by its dividends; a valuation multiple reflecting discounting and growth/risk. "In the stationary equilibrium where the household holds both public assets, the price-dividend ratios are:"

- pricing kernel: Another name for the stochastic discount factor; it maps state-contingent payoffs to prices. "This discontinuity---from finite to infinite hedging demand---cannot arise under GKP's gradual displacement, where the pricing kernel remains well-behaved."

- pro-rata claim: A proportional entitlement to a total based on ownership share. "the household's share can differ from its pro-rata claim on public dividends."

- rare disasters literature: A body of asset-pricing research on low-probability, high-impact macro shocks and their pricing effects. "the rare disasters literature \citep{Barro2006,Wachter2013},"

- representative household: A modeling device that aggregates all consumers into a single agent whose choices mirror the aggregate. "A representative household is the marginal investor in public stock markets."

- restricted equity: Ownership stakes (e.g., founder or pre-IPO shares) that are not publicly tradable, limiting hedging. "AI owners also hold restricted equity---founder stakes, pre-IPO shares, and other claims on AI firms that are not available for public trading."

- stationary equilibrium: An equilibrium in which key ratios or distributions remain constant over time. "In the stationary equilibrium where the household holds both public assets, the price-dividend ratios are:"

- stochastic discount factor (SDF): A random variable that discounts state-contingent payoffs to present values, reflecting marginal utility across states. "Because markets are incomplete, the household's stochastic discount factor (SDF) reflects its own consumption growth, not aggregate consumption growth."

- veto: The option to block a development or policy at a cost, used here for halting AI progress. "The household can veto AI development at a cost , representing a permanent fraction of consumption lost to the deadweight costs of intense government intervention needed to halt AI progress."

Collections

Sign up for free to add this paper to one or more collections.