- The paper introduces a regulator-leader-follower game model that integrates incentive compatibility and individual rationality for optimal regulation under herding.

- It employs stochastic control and closed-form solutions to derive optimal policies and compensation schemes based on risk and herding parameters.

- The findings reveal a threshold-based intervention, where regulation is activated only when follower risk-taking and herding exceed set critical levels, improving social welfare.

Mechanism Design for Investment Regulation under Herding

Introduction

The paper "Mechanism Design for Investment Regulation under Herding" (2604.11100) addresses the quantitative regulation of herding phenomena in financial markets, an area where classical regulatory interventions such as information disclosure and transaction restrictions lack theoretical guarantees and precision. The authors construct a regulator-leader-follower trilateral game using optimal control and mechanism design theory, with the regulator seeking to maximize social welfare given asymmetric information regarding investor herding propensities. The proposed framework integrates incentive compatibility and individual rationality constraints into dynamic regulatory mechanism design for investment decisions under herding, yielding tractable optimal policies and compensation constructs.

The trading environment is composed of a risk-free asset and a risky asset, with a single leader and a single follower investor, in addition to a regulator. The leader’s decision process follows a rational, risk-averse stochastic control strategy, where their terminal utility adopts the exponential form parameterized by the risk coefficient α~. The follower’s decision, in contrast, reflects both risk aversion and a herding tendency towards the leader, weighted by a private ‘herd coefficient’ η. The regulator’s objective is to maximize the expected terminal wealth of the follower (interpreted as aggregate social welfare), net regulatory costs incurred by interventions q(η), while knowing the follower’s risk aversion but not the herding parameter.

Compensation is used to guarantee IR and IC: policies that force behavioral adjustments must include appropriate transfer mechanisms to make participation attractive and truth-telling optimal. The follower reports a possibly distorted herding level η^ and solves a combined portfolio-deviation optimization where their objective penalizes deviation from the leader as well as monetary risk.

The Stackelberg game structure emerges clearly here: the mechanism is designed as a policy-compensation pair γ=(q,c), published by the regulator, to which the follower responds with (possibly misreported) herding and investment.

Analytical Results

Follower Optimal Response

The follower’s optimal allocation process is explicitly characterized in closed form, depending on the mechanism γ(η), the risk coefficients, and the herding parameter, and modulates the leader's strategy via weighted tracking, with weights optimally adapted to regulatory distortions. Expected terminal wealth (ExT(η)) and investment trajectories are derived from the exponential utility and the coupled SDE system.

Regulator’s Mechanism Design

Under the revelation principle, the mechanism designer can restrict attention to truthful herding reports, conditioning mechanisms on η directly, with IC and IR manifesting as functional constraints on q(η) and c(η). The mechanism design reduces to finding the policy/compensation pair that trades off regulatory cost against achievable increases in social welfare over the unregulated equilibrium.

If regulatory cost η0 is negligible, the paper finds a sharp switching structure: when the follower is more risk-taking than the leader (η1), and herding is substantial, the regulator optimally imposes the strictest possible policy, fully correcting herding, and the optimal compensation is determined to exactly cover the associated utility loss for the follower.

When regulatory cost is significant, the policy is only enacted if the induced economic gain (“the improvement in expected terminal welfare”) exceeds a computable threshold. This leads to a discontinuous threshold policy: regulation is triggered only above some critical herding intensity, which itself increases with η2.

The compensation scheme is endogenized and must cover the utility decrement imposed by the intervention, with closed-form expressions for the constant and η3-dependent components, both required to ensure IR and IC.

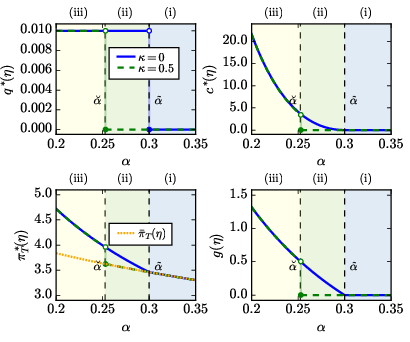

Figure 1: The regulator's optimal policy, required compensation, the follower's optimal decision, and the realized economic gain, varying with the risk coefficient when the follower's herd coefficient is fixed at η4.

Structural Properties

Key analytical results include:

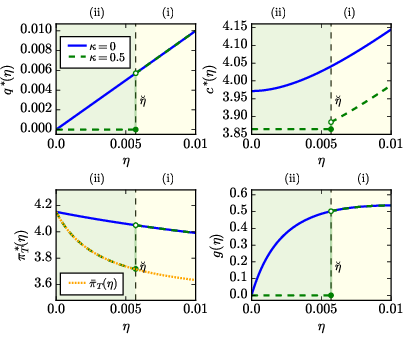

- Switching Structure: The optimal intervention is either maximal or none, depending on relative risk aversion and the economic trade-off with cost.

- Monotonicity with Herd Coefficient: Both the required policy strength and the compensation increase with η5, for η6.

- Thresholding via Regulatory Cost: The herd coefficient threshold η7 is an increasing function of regulatory cost, supporting selective intervention only for high herding intensity.

- IC and IR Constraints Lead to Truthful Reporting: The design guarantees truthful revelation of herding, even under information asymmetry.

Figure 2: The regulator's optimal policy, compensation, follower's decision, and economic gain as a function of the herd coefficient for a risk-taking follower (η8).

Implications for Social Welfare

The degree to which social welfare improves under regulation is proved to be zero unless the follower is both more risk-taking than the leader and herding is above the regulatory threshold; in that regime, the gain is monotonic with η9. This formalizes when regulation is both effective and necessary, and predicts null effects for markets where investor risk aversion exceeds that of observed leaders.

Numerical Results

The paper includes extensive numerical validation of the theoretical findings. Under a representative parametrization, the optimal policy and compensation can be seen to sharply switch as investor risk aversion and herding cross critical values. For fixed q(η)0, as the follower becomes more risk-averse, both regulation and compensation vanish; as the follower becomes more risk-taking, the magnitude of regulation and compensation increases, as does the improvement in social welfare (the economic gain). Analogous patterns are observed with q(η)1 as the control variable.

Theoretical and Practical Implications

This work quantitatively characterizes the previously informal intuition that regulatory interventions against herding should be both selective and intensive, depending on relative risk attitudes and actual herding propensity. The formalism bridges rational dynamic portfolio control with modern mechanism design under asymmetric information—a nontrivial extension of classical mean-variance and Merton-style portfolio problems to behavioral finance settings. Notably, the endogenous compensation schemes provide a rigorous foundation for incentive-aligned subsidy and intervention design.

Practically, these results suggest that blanket regulation or naive intervention schedules are suboptimal: instead, mechanisms must be dynamically and individually targeted, and cost-benefit calculus must incorporate heterogeneity in herding and risk preferences. The reliance on observable risk metrics (risk coefficient) and theoretically justified, thresholded actions grounds policy proposals for electronic markets and algorithmic trading environments, where replication of this trilateral structure (platform—leader—followers) is increasingly manifest.

On the theoretical front, the explicit construction of IR/IC-satisfying mechanisms for continuous-time investment under herding may be extended to richer multi-agent and time-varying settings, especially once transfers are no longer costless or leaders are strategic.

Future Research Directions

Several avenues for extension are clear:

- Market Generalization: Extending to multiple leaders and heterogeneous followers, and incorporating market impact or time-varying model coefficients.

- Learning and Estimation: Incorporating Bayesian mechanism design to deal with incomplete information on both risk and herding coefficients.

- Strategic Leaders: Analyzing games where leaders may anticipate regulation, or where strategic manipulation by leaders is endogenous.

- Transfer Costs and Institutional Constraints: Relaxing the assumption of costless compensation to accommodate budget constraints and inter-market frictions.

Conclusion

This work provides a rigorous, dynamical framework for the regulatory mechanism design problem in investment environments characterized by herding. The derived exact policies, threshold structures, and incentive-aligned compensation rules offer both theoretical insight and guidance for robust, cost-effective financial regulation. These results underpin future research into scalable, adaptive, and information-sensitive regulatory architectures under investor behavioral biases.