- The paper presents AEGIS, a regime-agnostic framework that systematically generates asymmetric alpha while mitigating extreme tail risks.

- It integrates volatility-adjusted momentum, minimax correlation filtering, and Sortino-optimized convex allocation to ensure effective downside protection.

- Empirical results over 20 years show that AEGIS outperforms major benchmarks with higher CAGR and significantly reduced drawdowns.

Taming the Black Swan: A Hierarchical Framework for Asymmetric Alpha Generation

Introduction

The paper "Taming the Black Swan: A Momentum-Gated Hierarchical Optimisation Framework for Asymmetric Alpha Generation" (2604.09060) introduces the Adaptive Equity Generation and Immunisation System (AEGIS), a systematic, regime-agnostic portfolio optimisation architecture designed to mitigate the structural vulnerabilities exhibited by standard momentum and mean-variance strategies, particularly under extreme tail-risk events. The framework departs fundamentally from classical Modern Portfolio Theory (MPT) and mean-variance optimisation (MVO) by replacing arbitrary covariance-based diversification and indiscriminate volatility penalisation with a layered construct integrating volatility-adjusted momentum, minimax correlation filtering, and convex allocation focused on downside-specific penalisation. Empirical results demonstrate compound alpha generation with materially superior downside protection and crisis resilience over two decades, including multiple market shocks.

Data Acquisition and Preprocessing

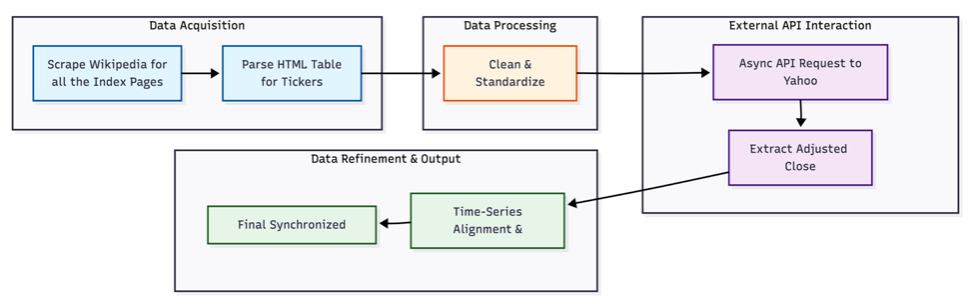

AEGIS incorporates an automated, scalable data pipeline for real-world portfolio construction.

Figure 1: Automated data pipeline scraping index constituents, synchronising historical price series, and generating a time-aligned dataset suitable for quantitative analysis and walk-forward simulation.

Constituent universes are aggregated from the S&P 500, S&P MidCap 400, S&P SmallCap 600, NASDAQ-100, and Dow Jones indices. Strict liquidity, market cap, and financial viability criteria are enforced (e.g., minimum Float-Adjusted Liquidity Ratio, earnings positives, and free-float constraints for S&P), aligning with institutional investability standards. Historical adjusted-close price series are extracted via concurrent API requests, followed by rigorous cleaning, forward-filling for alignment, and drop of insufficient-history or delisted assets to control for survivorship bias.

Walk-Forward Validation Architecture

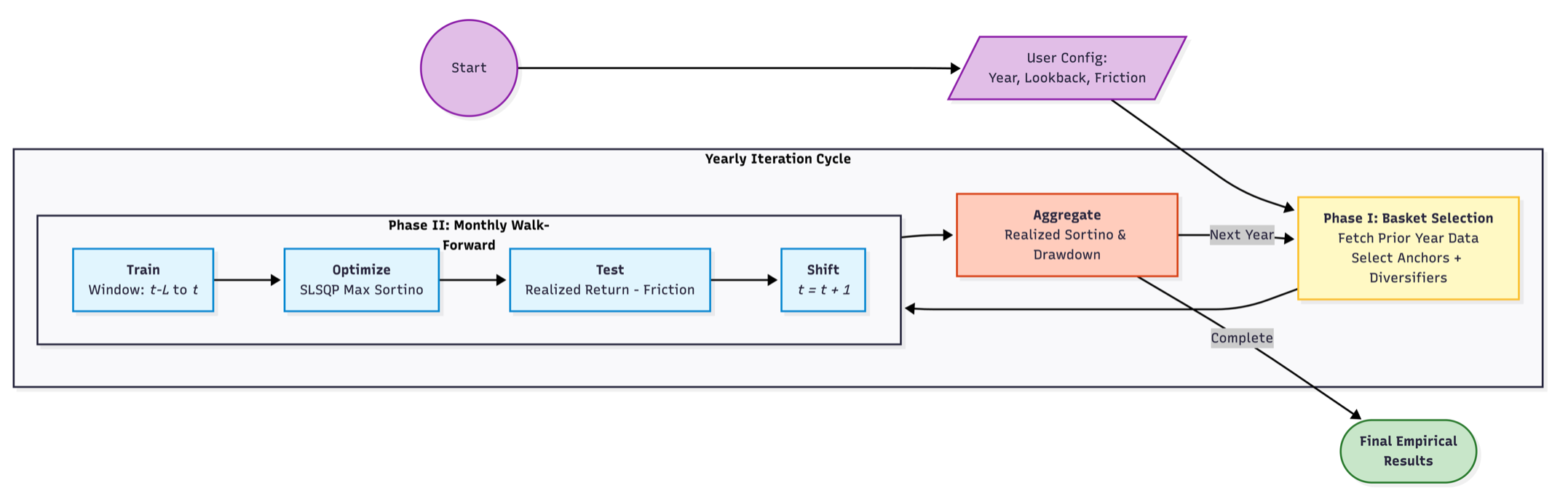

The framework employs a genuinely out-of-sample, multi-year walk-forward evaluation.

Figure 2: Nested-loop validation segregating rolling, non-overlapping training and testing windows, enforcing realistic lookahead constraints and net-of-friction performance calculations.

For each test period, basket selection and allocation are optimised based solely on prior window data, with transaction friction applied, thereby eliminating both overfitting to statistical artefacts and look-ahead bias. The simulation rigorously implements real-world constraints on rebalance frequency and transaction costs.

Hierarchical Portfolio Construction

AEGIS's three-stage pipeline decouples return generation from structural risk:

Signal Generation

Figure 3: Sector-wise ranking based on volatility-adjusted momentum selects robust trend leaders (“Anchor Triad”) as the core growth engine of the portfolio.

A hierarchical filtration identifies sector leaders via cumulative logarithmic returns and subsequently ranks them by realised volatility-normalised efficiency (VAM score), isolating assets exhibiting genuine trend strength rather than high-beta artefacts. The top three sector leaders (the Anchor Triad) are locked to form a long-term, structurally diversified offensive core.

Immunisation Layer

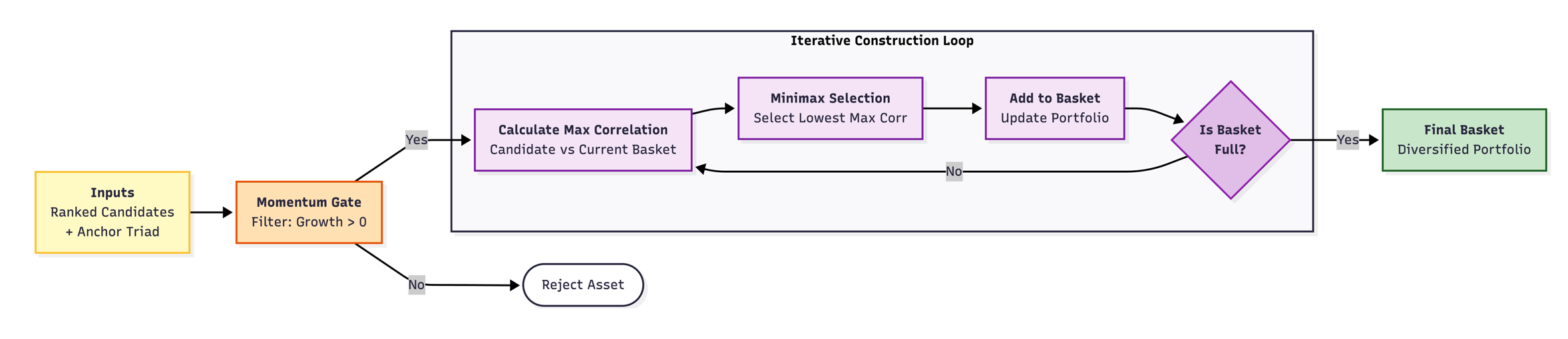

Figure 4: Iterative selection process ensures new basket inclusions minimise maximum correlation to extant portfolio, enforcing true structural diversification beyond mean-variance orthodoxy.

Diversification is not a function of naive covariance reduction or equal-weighting. The immunisation filter applies a minimax correlation criterion: only those assets whose maximum pairwise correlation with current basket constituents is lowest are added, ensuring maximal orthogonality and risk-factor independence. Critically, a “momentum gate” prohibits inclusion of assets with negative returns, counteracting the conventional value-trap risk of low-correlation selection.

Allocation Engine

Figure 5: Allocation via SLSQP optimisation, maximising Sortino ratio subject to long-only, budget, and strict per-asset cap constraints to prevent concentration and enforce institutional capital discipline.

Portfolio weights are determined by solving a constrained convex optimisation problem maximising the Sortino ratio—targeting downside-risk-adjusted returns rather than raw volatility suppression. Single-asset exposure is capped (≤5%), enforcing real-world liquidity and diversification standards.

Empirical Results

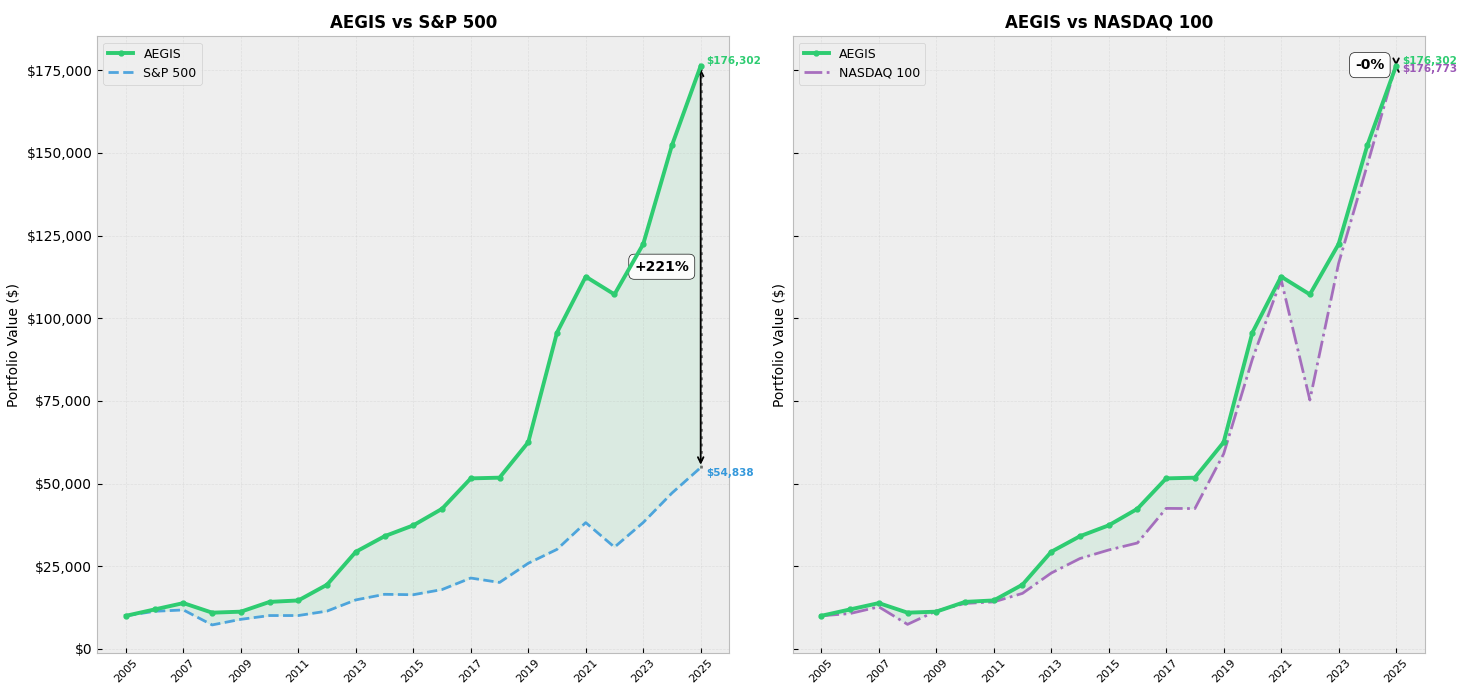

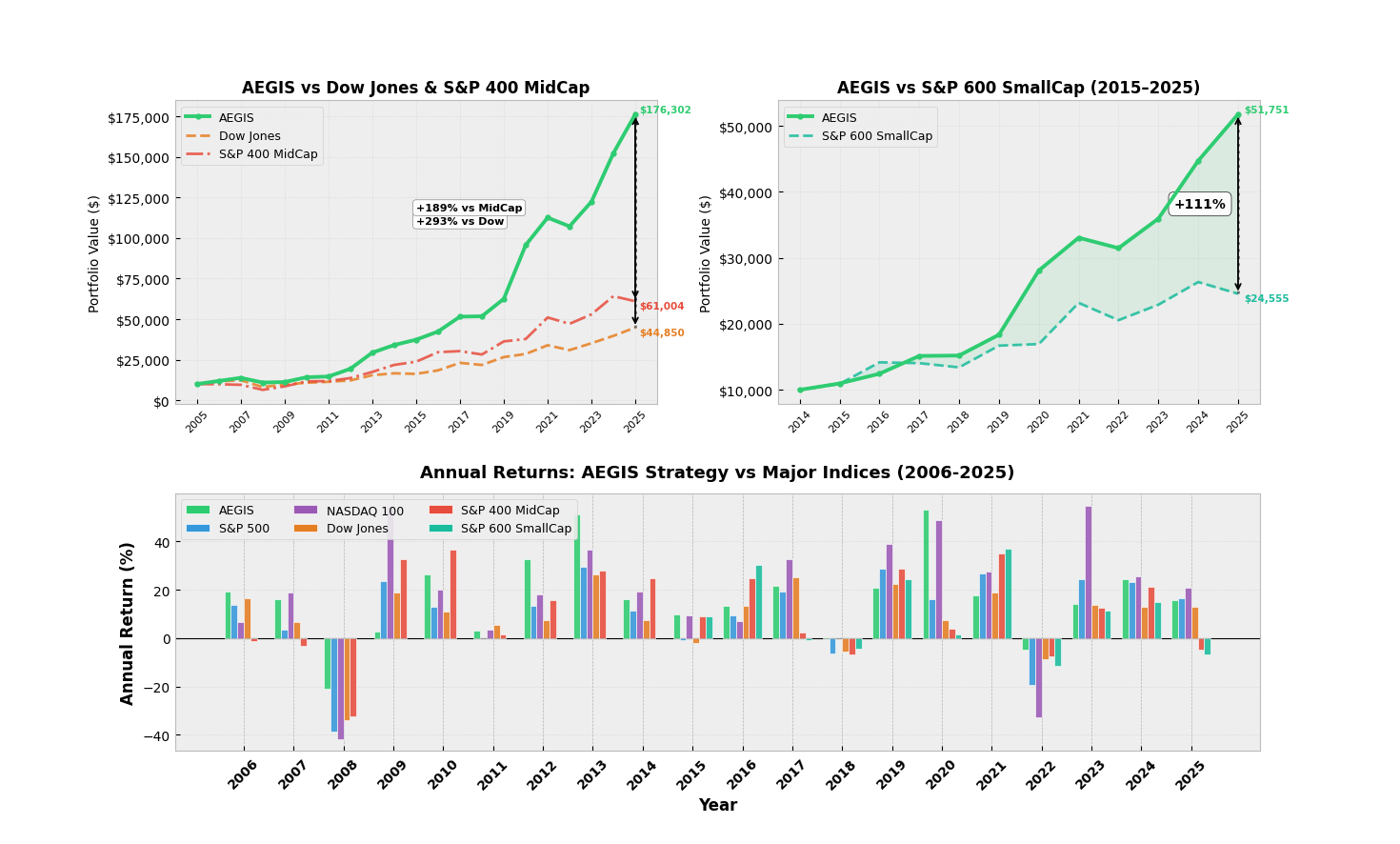

Figure 6: 20-year wealth trajectory: AEGIS outperforms S&P 500, matches NASDAQ in growth with drastically smoother compounding.

Over a 20-year period (2006–2025 including the 2008 GFC and 2022 tightening), AEGIS delivers a CAGR of 15.41% net-of-friction versus 8.88% for the S&P 500 and 15.44% for the NASDAQ-100. Terminal wealth for an initial $10,000 allocation is$176,302, a +221% relative gain over the S&P 500. This is achieved with less than half the worst drawdown seen in tech indices.

Figure 7: AEGIS demonstrates robust outperformance versus Dow, MidCap, and SmallCap indices, with return decoupling from small-cap size factor.

Performance is independent of size-factor exposure, refuting the hypothesis that alpha results merely from persistent small-cap bias.

Volatility and Drawdown Analysis

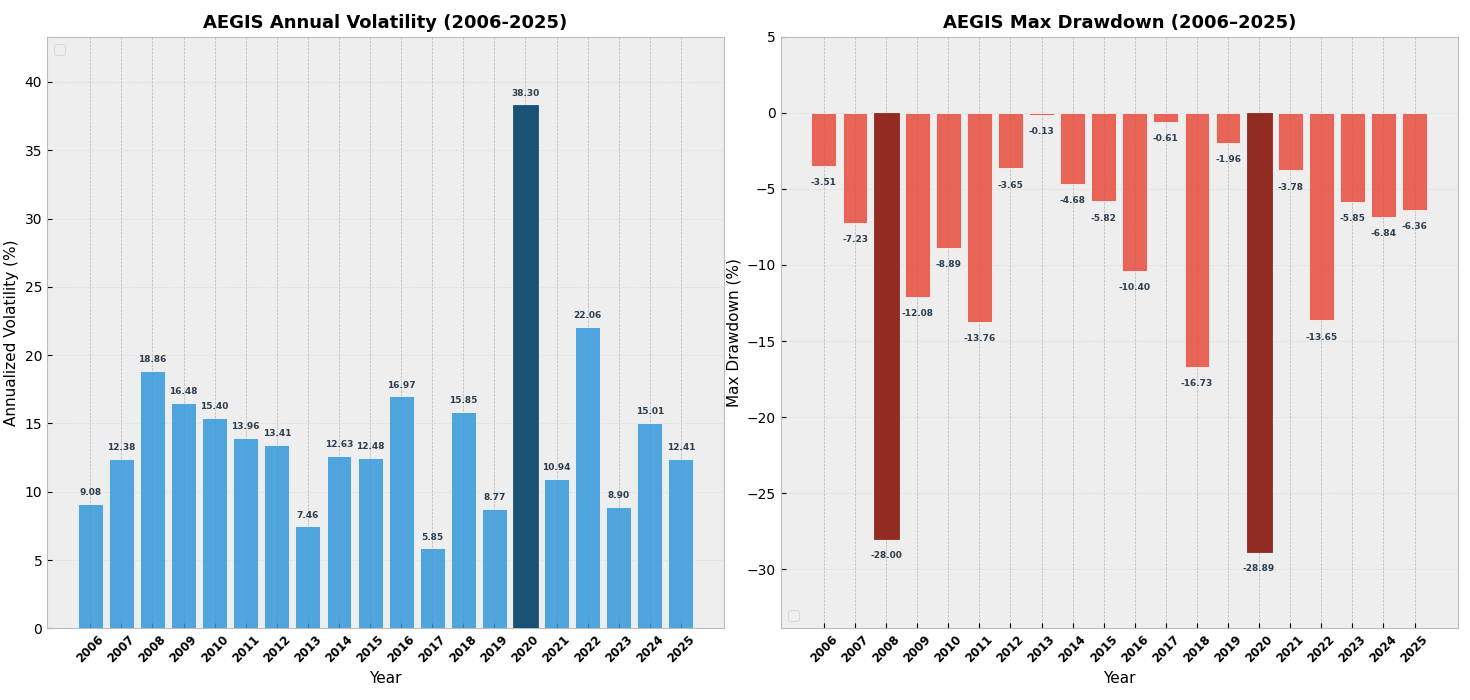

Figure 8: Annualised volatility and drawdown trends; AEGIS consistently constrains downside, maintaining stable performance across diverse market regimes.

The AEGIS equity curve is marked by low average volatility (16.44%), moderate max drawdown (–28.89%), and exceptional Sortino ratios (average 6.47; outlier-adjusted 1.72). Notably, major drawdowns are materially suppressed even relative to low-volatility benchmarks.

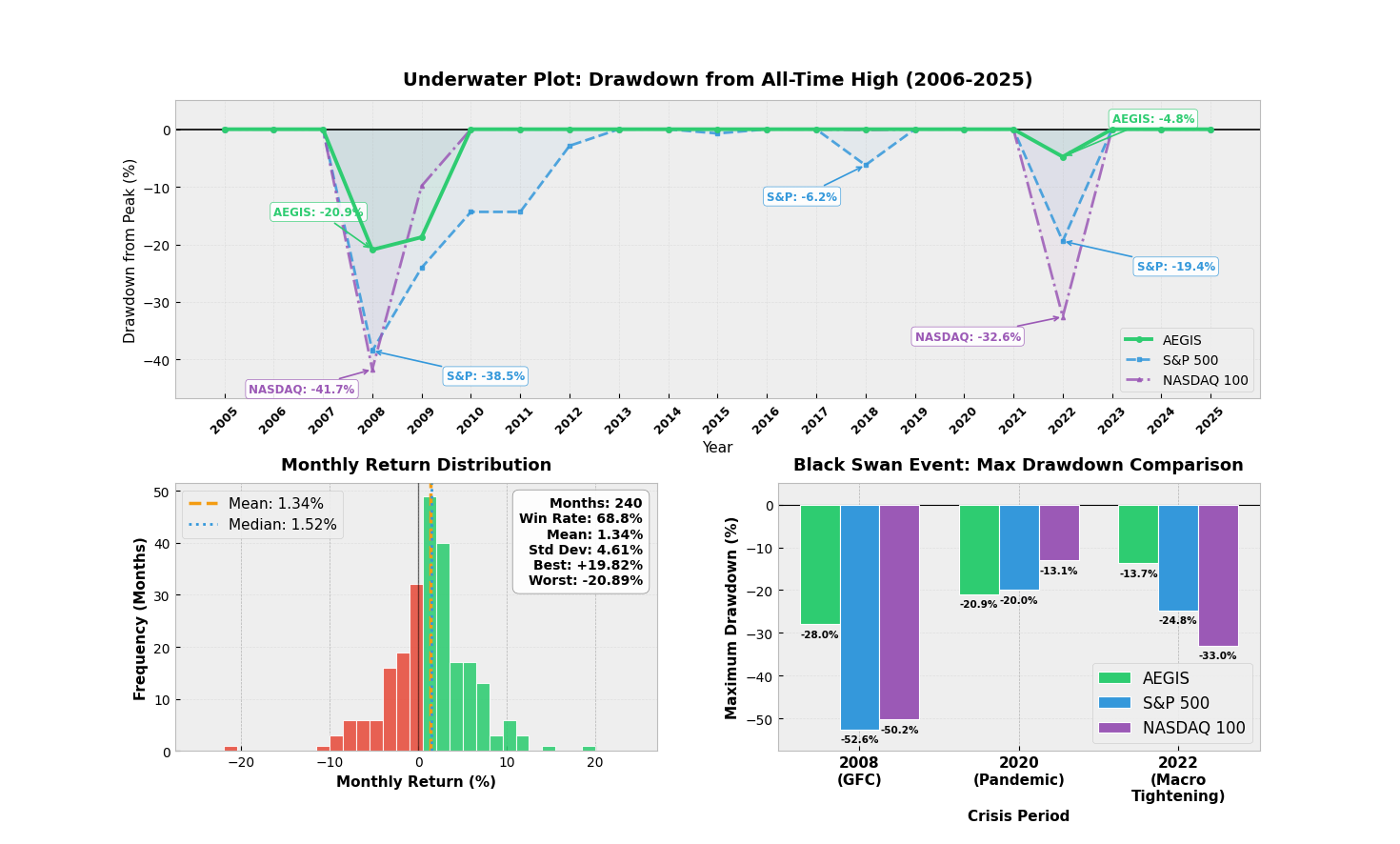

Figure 9: Subsurface drawdown plot and return distribution skew confirm pronounced left-tail truncation and persistent right-skew (asymmetry), with superior drawdown resilience across systemic crises.

AEGIS exhibits shorter and shallower recoveries post drawdown, confirming effective risk truncation.

Crisis Regime Robustness

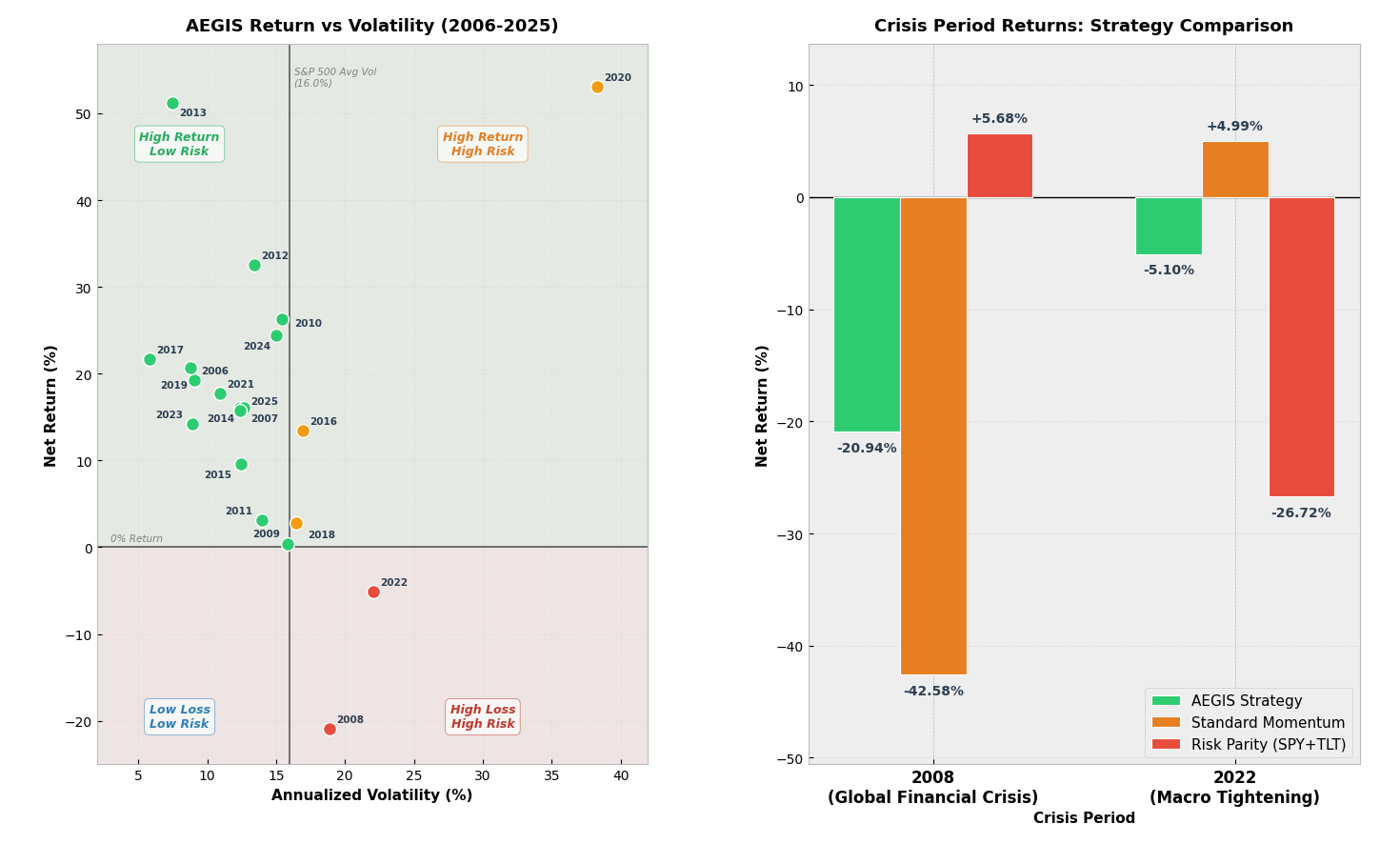

Figure 10: Return versus volatility scatter and comparative crisis returns: AEGIS systematically outperforms both classic momentum (CSM) and risk parity in both deflationary (2008) and inflationary (2022) shocks.

AEGIS strictly dominates standard momentum (which incurs momentum crashes and catastrophic losses in events like 2008) and risk parity (which collapses under correlation breakdown in 2022), achieving bounded drawdown and fast recovery. For example, AEGIS drawdown in 2008 = –20.94% (CSM: –42.58%, RP: +5.68%), and in 2022 = –5.10% (CSM: +4.99%, RP: –26.72%).

Theoretical Implications and Practical Impact

The formal departure from mean-variance paradigms towards explicit downside-centric convex optimisation and minimax-diversified basket construction enables dynamic regime-adaptive risk management, surpassing Markowitz-style assumptions. The minimax criterion moves the diversification objective from average- to maximum-correlation minimization, ensuring drawdown immunisation in crisis co-movement regimes. The strict exclusion of negative-momentum assets resolves the “value trap” and survivorship bias (validated by deliberate dead-stock injection in the experiment).

The combined VAM/minimax/Sortino pipeline effectively constructs an anti-fragile asset allocation methodology capable of engineering synthetic beta—matching concentrated benchmarks’ growth but exhibiting utility-like downside resilience.

Parameter Stability and Survivorship Bias

Grid sweep experiments demonstrate performance robustness to changes in diversifier count and allocation lookback. Only the simultaneous enforcement of a ~50-asset basket and short allocation lookback (3 months) yields optimal tradeoff between alpha capture and variance suppression, and this persists over all sub-periods. Manual re-injection of historically delisted or bankrupted stocks establishes true survivorship bias control.

Future Prospects

AEGIS's architecture generalises to any investable asset-class universe, and its reliance on dynamic covariance/statistics, rather than fixed historical regime assumptions, suggests suitability for cross-asset, multi-factor, and tactical allocation. Potential extensions include L1- or L2-regularisation for additional robustness, integration with alternative risk premia or non-linear (e.g., copula or tail-dependence) risk filters, and application to intraday or multi-frequency data for high-frequency risk management. Translation to constrained multi-currency or non-U.S. universes is immediate.

Conclusion

The AEGIS framework, as validated by rigorous, bias-controlled 20-year simulation, evidences that synthetic asymmetric alpha can be systematically engineered via a mathematically layered approach: sector-wise VAM filtration, minimax correlation basket immunisation, and Sortino-optimised convex allocation. The model outperforms major U.S. benchmarks in both return and drawdown, survives multiple black swan events without regime dependency, and is robust to bias, overfitting, and parameter misspecification. Theoretical advances in the paper reorient the field of quantitative portfolio management towards adaptive, structurally anti-fragile design, offering a formal blueprint for high-growth, crisis-resilient investment frameworks.