- The paper demonstrates that the joint asset pricing of bonds and stocks is best explained by a dense stochastic discount factor constructed via Bayesian Model Averaging.

- It employs continuous spike-and-slab priors and latent binary variables to robustly infer factor inclusion probabilities, leading to superior out-of-sample portfolio performance.

- Empirical results show that once Treasury risks are controlled, many bond-specific factors become redundant, highlighting common macro and equity risk exposures.

Bayesian Model Averaging and the Joint Asset Pricing of Bonds and Stocks: An Essay on "The Co-Pricing Factor Zoo" (2604.04430)

Introduction

"The Co-Pricing Factor Zoo" undertakes a comprehensive Bayesian analysis of the factor zoo in empirical asset pricing, with a focus on understanding the joint compensation for risk in U.S. corporate bonds and equities. The authors systematically investigate the pricing kernel (stochastic discount factor, SDF) implied by more than 254∼18 quadrillion combinations of 54 observable factors, both tradable and nontradable. Utilizing Bayesian Model Averaging (BMA) combined with robust hierarchical priors, the study evaluates whether the joint cross-section of bonds and stocks can be rationalized by a sparse set of robust factors or whether the latent SDF is necessarily high-dimensional in the space of observable risk proxies.

Methodology

At the methodological core lies a Bayesian framework that simultaneously addresses weak identification, model uncertainty, and dense misspecification—issues endemic in frequentist approaches to asset pricing factor testing when confronted with large candidate sets. The key technical advances include:

- Continuous spike-and-slab priors for market prices of risk, regularizing inferences even when numerous factors are weak or useless proxies and enabling robust credible set computation for dimensionality and risk premium attribution.

- Latent binary variables dictating factor inclusion, paired with flexible prior settings (including asset-class tilting and sparsity constraints) to probe model robustness.

- BMA SDF construction, wherein posterior-weighted aggregation of all possible factor model SDFs yields an optimal predictor of risk premia and outperforms selection-based approaches.

- Large-sample and simulation evidence demonstrating BMA's superior recovery of latent SDF risk compensation even when true factors are unobservable, with negligible performance degradation compared to infeasible omniscient baselines.

Key Empirical Results

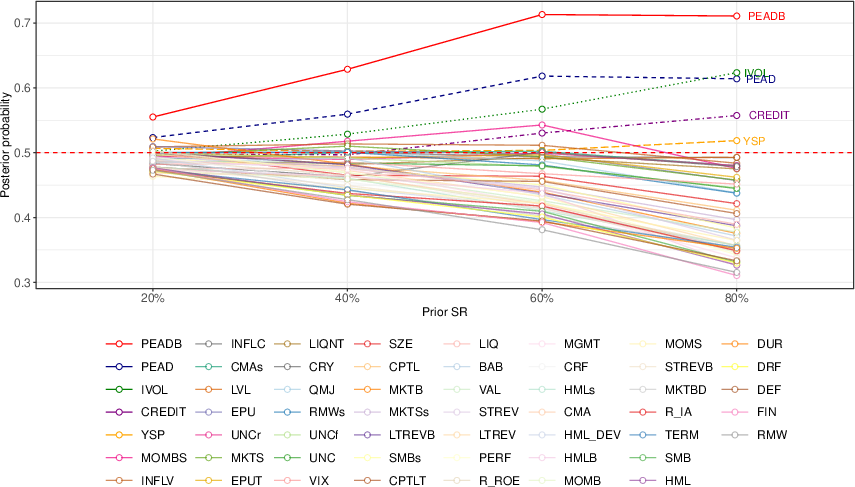

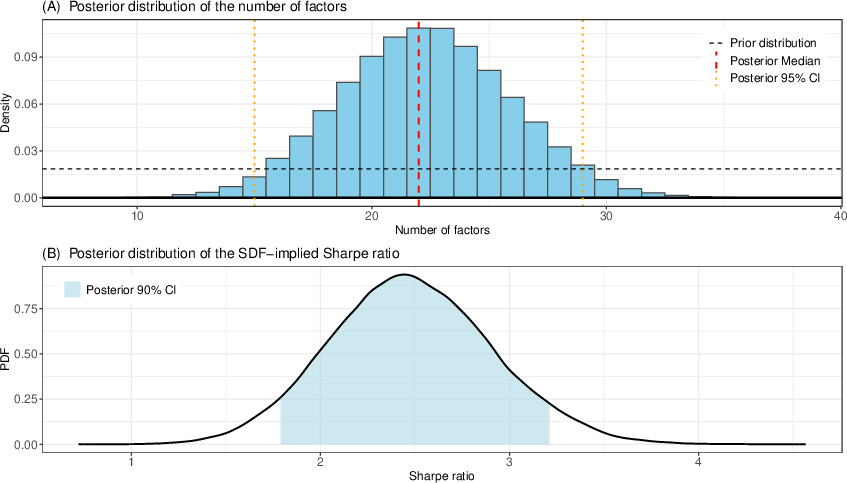

1. Posterior Inclusion Probabilities, Model Dimension, and SDF Density

The Bayesian analysis overwhelmingly challenges the view of a sparse, low-dimensional SDF as appropriate for the joint pricing of bonds and stocks. The posterior distribution assigns non-negligible probability weight to models with 15–29 factors. The most probable sources of priced risk include (i) post-earnings announcement drift (PEAD) factors in both bonds (PEADB) and equities (PEAD), (ii) nontradable macro-financial variables such as the yield curve slope (YSP), the AAA/BAA credit spread (CREDIT), and idiosyncratic equity volatility (IVOL).

Figure 1: Posterior inclusion probabilities for all candidate factors, highlighting the behavioral (PEAD, PEADB) and a handful of nontradable macro-financial factors as robust risk sources.

Despite the density of the SDF in observable space, the maximum achievable Sharpe ratio remains moderate (∼2.5), reflecting that much spanning is duplicative: observable factors—particularly among the "zoo"—act as noisy, collinear proxies for a small set of true fundamental risks. Consequently, specification search procedures limited to a handful of factors are, with high probability, subject to severe omitted-variables-induced misspecification.

Figure 2: Posterior on SDF model dimensionality and implied Sharpe ratio, decisively rejecting sparse SDFs in favor of dense, commonly spanned configurations.

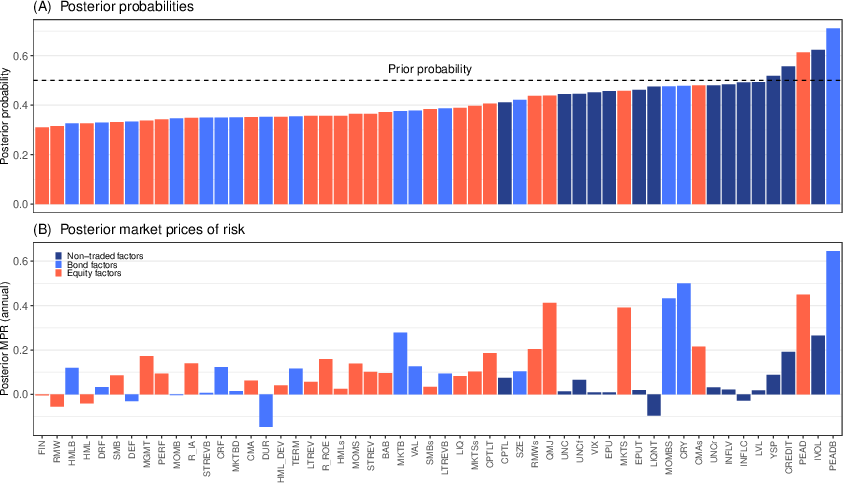

2. Factor Risk Price Attribution and Optimal Portfolio Construction

BMA allows for the optimal aggregation of signals from many collinear proxies, guarding against overfitting and spurious factor risk prices, and clarifies the distinction between:

- Factor inclusion probability (posterior, theoretical relevance to the SDF), and

- Posterior market price of risk (economic contribution to spanning the SDF via BMA-aggregate portfolio weights).

Many low-inclusion-probability factors still carry high posterior risk prices, underlining their joint role as proxies for underlying SDF components, even if not fundamental in isolation.

Figure 3: Posterior factor probabilities and posterior market price of risk, quantifying the contribution and practical salience of each factor in BMA SDF construction.

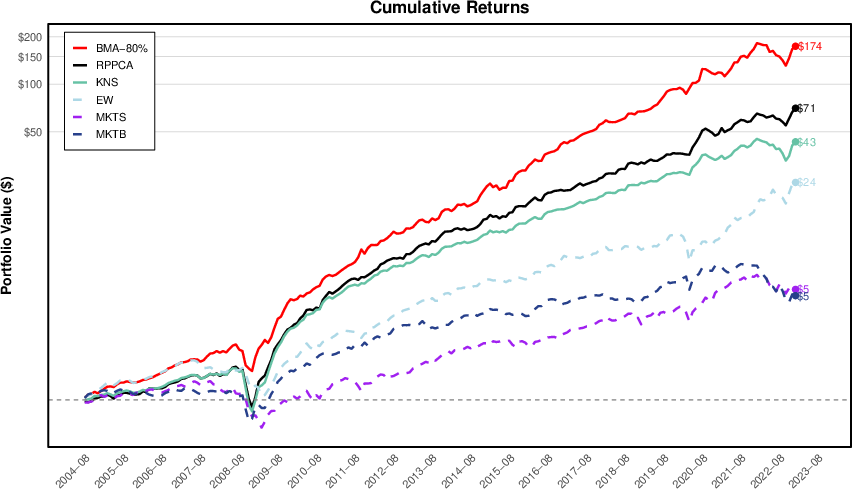

Out-of-sample tests based on large cross-sections of bond and stock portfolios demonstrate outperformance of the BMA-SDF relative to canonical sparse models (e.g., Fama-French, intermediary SDFs, PCAs), both in terms of pricing errors (RMSE, R2) and achievable Sharpe ratios for BMA-constructed portfolios. Out-of-sample tradable portfolios constructed using BMA-implied weights attain annualized Sharpe ratios in the 1.5–1.8 range, with only annual rebalancing, over horizons that include major financial crises.

Figure 4: Cumulative returns to the BMA-SDF tradable strategy, demonstrating high, persistent Sharpe ratios unattainable by classic benchmarks or simple factor averages.

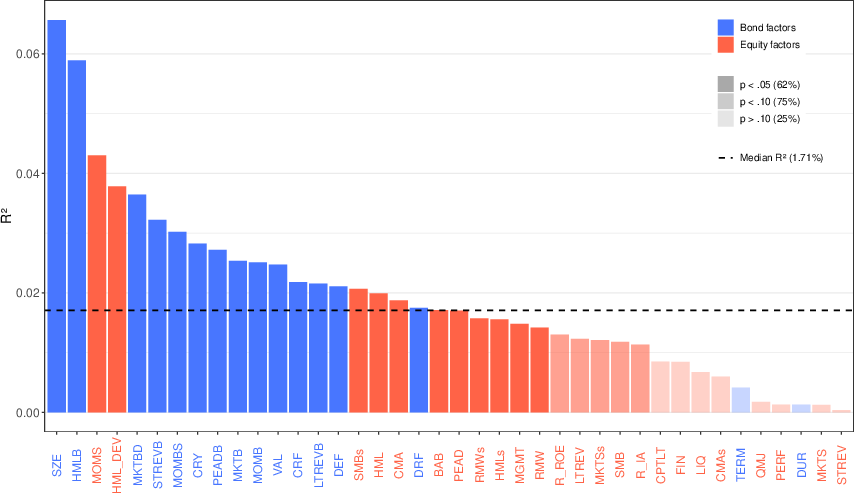

4. Theoretical and Practical Redundancy of Large Sections of the Bond Factor Zoo

A crucial, contradictory empirical result is that, once the Treasury term structure component is stripped from corporate bond returns (i.e., by duration-matching), the explanatory power of bond-specific, tradable factors for the joint SDF becomes negligible. The cross-section of bond credit risk is largely rationalized by equity and global macro factors, rendering most of the bond factor zoo redundant for co-pricing purposes. Tradable bond factors mainly capture variation linked to Treasury yield risks, not true corporate bond-specific premia.

Figure 5: Out-of-sample fit for duration-adjusted bond and stock returns showing the irrelevance of bond factors once Treasury risk is removed.

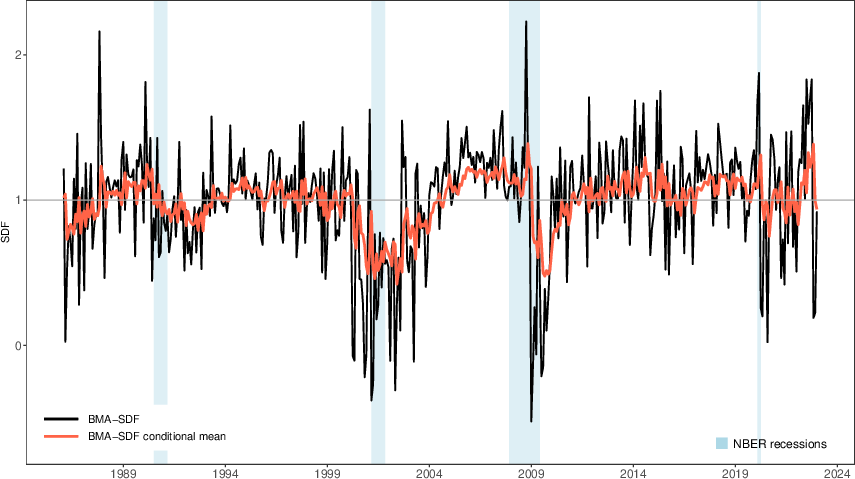

5. SDF Dynamic Properties and Macro-Predictability

The conditional mean and volatility of the BMA-SDF exhibit clear business cycle dependence, with spikes in conditional volatility (implied Sharpe ratio) coinciding with major recessions and stress episodes, as expected from an intertemporal MRS. Both first- and second-moment dynamics of the SDF are highly persistent and statistically significant predictors of future returns across assets, in line with models featuring time-varying risk premia and economic mechanisms for macro-state-dependent pricing kernels.

Figure 6: Estimated BMA-SDF and its conditional mean exhibiting clear business cycle and recession-linked variation.

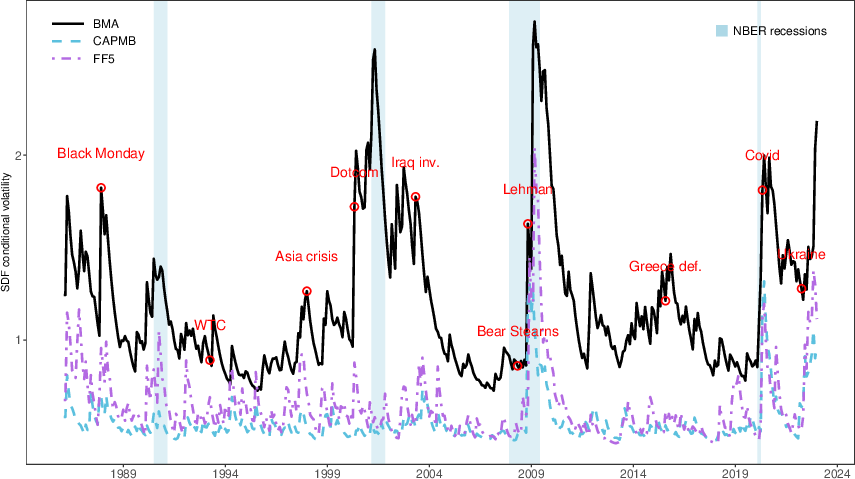

Figure 7: Conditional volatility of the BMA-SDF, showing spikes aligned with episodes of macro-financial turbulence.

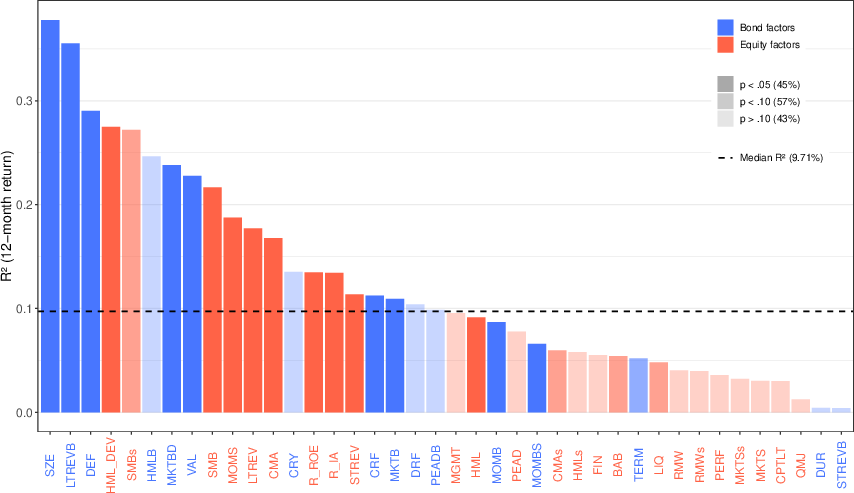

Figure 8: Lagged SDF information strongly predicts future monthly and annual returns for tradable factors.

Practical and Theoretical Implications

- Factor Selection: The SDF that rationalizes the cross-section of bonds and equities is dense. Factor selection procedures aimed at finding a small canonical set for the SDF are generally misspecified and will not recover correct compensation for risk.

- Redundancy and Integration: Once accounting for Treasury risk, bond-specific factors are not necessary for co-pricing, and equities and bonds share common, macro-linked, priced risk exposures. This aligns with segmented-markets and integration models in asset pricing.

- Behavioral Anomaly Pricing: Both the post-earnings announcement drifts in bonds and stocks are robustly priced risks, supporting models where limits of arbitrage and agent heterogeneity persist across asset classes.

- Tradable Aggregation: The BMA-SDF provides a robust method for constructing tradable portfolios that efficiently span latent priced risks, outperforming portfolios designed from selection- or PCA-based approaches.

- Macroeconomic Dynamics: The conditional mean and variance processes of the SDF, as estimated, strongly relate to business cycle conditions, supporting the distributional predictions of structural (e.g., long-run risks, intermediary asset pricing) models, and providing a tool for risk management and dynamic asset allocation conditioned on aggregate states.

Future Directions

- Extending the BMA-SDF methodology to international or alternative asset classes could further elaborate on the extent and structure of global-priced risks and the scope of cross-market factor redundancy.

- Real-time implementation and active trading applications, particularly in the context of stress test and macro risk management, given the strong predictive validity of the estimated SDF moments.

Conclusion

This study decisively demonstrates that the joint pricing of bonds and stocks requires a dense, BMA-aggregated SDF, not a sparse selection based solely on "robust" factors. The practical contribution is both a method and an empirical finding: Bayesian aggregation is essential for recovering correct risk compensation in the presence of a large, collinear factor zoo, and portfolios constructed using BMA SDFs attain superior Sharpe ratios even out of sample. Moreover, much of the factor literature specific to corporate bonds is rendered redundant by the explanatory power of equities and macro factors, once Treasury risk is controlled for. The behavior and predictability of the BMA-SDF link asset pricing directly to the macroeconomic state, providing insight into the temporal dynamics of risk premia and practical tools for asset management.