- The paper formalizes a revenue maximization problem under unreliable, AI-generated side information, establishing a Pareto frontier for consistency and robustness.

- It introduces a consistency–robustness mechanism design that exploits the buyer's higher-order information asymmetry using randomized posted pricing.

- The study demonstrates strong guarantees with perfect consistency and nontrivial robustness, informing pricing strategies in AI-driven marketplaces.

Optimal Pricing with Unreliable Signals: Consistency–Robustness Mechanism Design

This work formalizes a revenue maximization problem in the presence of unreliable, AI-generated side information. The seller aims to price a single item for a single buyer, where the buyer’s valuation v is unknown and drawn from a commonly known distribution F. The seller observes a private signal s which is either:

- Accurate (s=v): coincident with the buyer’s value, or

- Hallucinatory (s∼F): a sample drawn independently from the prior, conveying no information about the buyer.

The critical informational asymmetry arises because the seller does not observe the regime (accurate or hallucinatory), but the buyer knows the regime (even though the observed s remains hidden from her).

This setup reflects the increasing use of AI (notably, LLMs) for price discrimination using user-level predictions of value that may be unreliable. Mechanistically, the model adopts a consistency-robustness framework: the mechanism’s revenue performance is measured both when the signal is reliable (consistency, fraction C of value v can be extracted) and when the signal is unreliable (robustness, fraction R of OPT(F) can be extracted, where F0 is the revenue-optimal posted price for the prior).

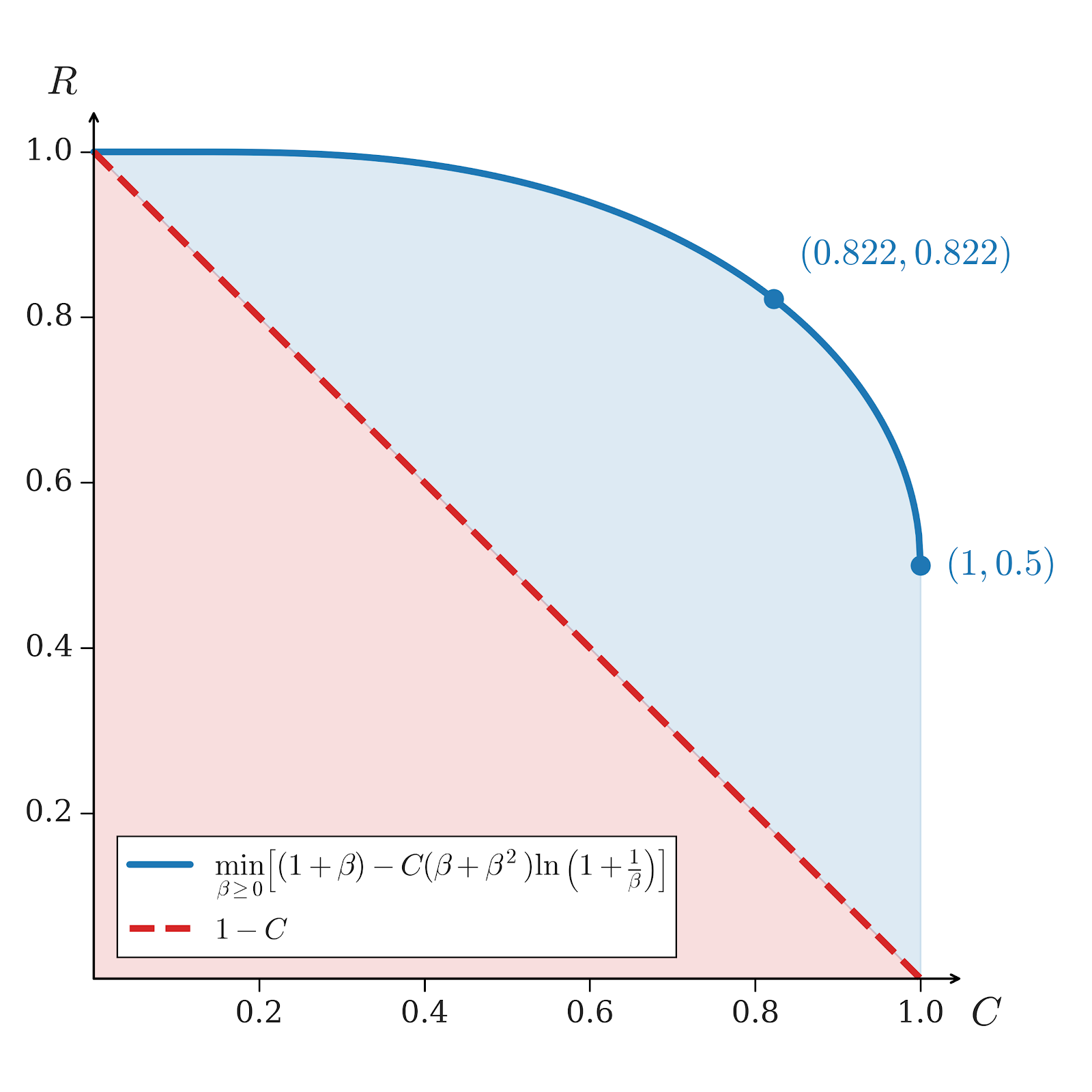

Main Contributions: Pareto Frontier of Consistency–Robustness Tradeoff

The paper gives a sharp, distribution-agnostic characterization of the achievable pairs F1, fully describing the Pareto frontier of possible tradeoffs.

Mathematically, for every F2, the maximum achievable robustness F3 is

F4

The result is both achievability (there exist mechanisms for every F5) and optimality (for every F6, there exists a prior where this F7 is infeasible).

The frontier strictly dominates the baseline “public-signal” randomized strategy (where F8), which mixes between posting the signal and posting the monopoly price but fails to exploit the informational asymmetry of private signals.

Figure 1: The blue line represents the F9 frontier, strictly dominating the s0 public-signal benchmark (dotted red).

For the symmetric guarantee (s1), the optimal ratio is approximately s2, which is superior to the s3 attained by public-signal randomization.

The analysis demonstrates that keeping the signal private introduces leverage: because the buyer knows the reliability regime while the seller does not, pricing schemes can be designed to exploit this higher-order asymmetry, achieving outcomes unattainable via public signal revelation.

Key technical reductions transform the high-dimensional mechanism design LP into a one-dimensional program using the structure of the consistency constraint:

- Consistency in the accurate regime translates to utility upper bounds in the hallucinatory regime.

- The optimal mechanism, under general constraints, is shown to be implementable via randomized posted pricing.

- The worst-case robustness is then captured by duality, yielding a low-dimensional optimization over step-function dual variables.

The piecewise nature of the worst-case distribution surfaces triangular or step-like forms in value space, distinct from standard triangular forms in quantile space prominent in prior-independent/prior-free models.

Strong Guarantees: Perfect Consistency, Robustness, and Best-of-Both-Worlds

The paper provides several strong results:

- Perfect Consistency with Nontrivial Robustness: For every prior, there exists a mechanism that is 1-consistent (full value extraction in the accurate regime) and s4-robust:

- This is achieved via a “guess-for-discount” mechanism: the seller posts a hidden price based on s5, allows the buyer to guess s6, and gives a discount for a correct guess. If s7 is accurate (the buyer knows its value), she gets the discount, otherwise, in the hallucinatory regime, the expected revenue can be analytically lower bounded.

- Best-of-Both-Worlds: For distributions where the mean is at most the monopoly price (e.g., uniform s8, exponential), it is possible to achieve both s9 and s=v0 simultaneously.

- Heavy-Tailed (Infinite Mean) Distributions: For priors with infinite mean, for every s=v1, there exists a mechanism "almost" attaining s=v2.

These results reveal that private unreliable signals, when their reliability is known to the buyer, are a robust source of informational leverage. The contrast with public-signal models is especially apparent: in the public-signal baseline, perfect consistency and nontrivial robustness are mutually exclusive.

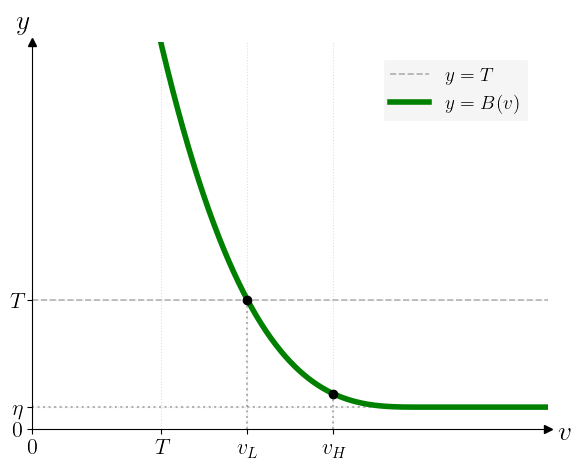

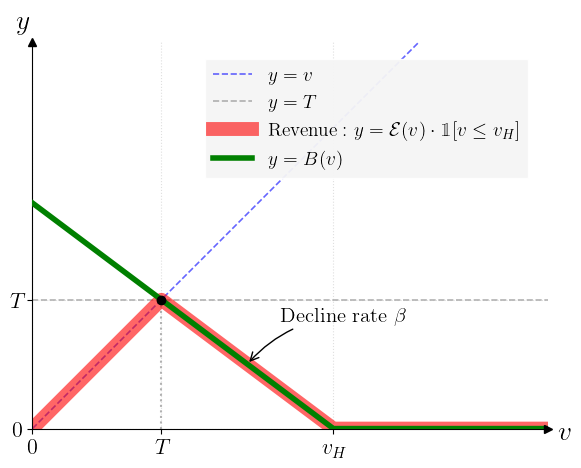

The technical characterization of the worst-case distribution for robustness (given a dual variable s=v3 and benchmark s=v4) uses a three-threshold envelope, leading to the following piecewise construction:

- Below threshold s=v5: all probability on zero values.

- In s=v6: mass so that s=v7.

- In s=v8: dictated by the dual variable s=v9, saturating convex dual constraints.

- Above s∼F0: all mass above, capturing the adversarial nature.

Figure 2: Illustration of the thresholds s∼F1 and s∼F2 which control where the revenue curve constraints become binding.

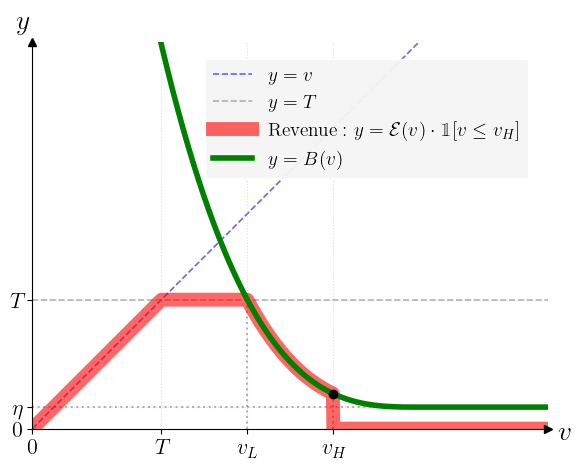

Figure 3: The revenue-curve constraints creating a tight envelope, determining the extremal (worst-case) distribution.

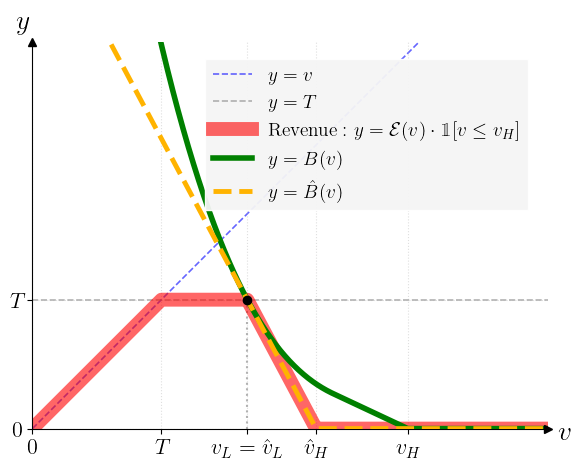

The analysis further reduces the dual optimization to step-functions, noting that extremal worst-case mechanisms are elicited by low-dimensional parameterizations.

Figure 4: Conversion of general s∼F3 dual variable to a step-function, reducing the problem's complexity.

Figure 5: Revenue curve for the extremal worst-case distribution s∼F4, illustrating piecewise construction in value space.

Practical and Theoretical Implications

The results establish a new paradigm where mechanism design explicitly leverages agents’ knowledge about the reliability of the designer’s information, rather than only the information directly available to the designer. The framework presents a compelling argument for the utility of secrecy about the reliability of AI-generated or third-party side information in economic design.

Practical implications include:

- Strategies for vendors in marketplaces with AI-driven buyer profiling; optimal use of incomplete or noisy side information.

- Design principles: mechanisms should not always “faithfully” reveal or act on side information, but instead optimally integrate both the signal and meta-information about its reliability.

Theoretical implications:

- Novel LP reductions suggest deeper connections between higher-order information asymmetry and mechanism smoothness.

- Reveals a distinct separation between public information frameworks and private, higher-order knowledge settings.

- Suggests similar approaches could extend to multi-agent, multi-item, or more general stochastic environments and broader classes of side information (mixtures between accurate and hallucinatory).

The results also open avenues in the learning-augmented algorithms literature, highlighting the tension and complementarity between robustness and adaptivity in stochastic, AI-driven environments.

Conclusion

This paper presents a comprehensive analysis of optimal pricing under unreliable, private side information, with a formal Pareto frontier for consistency and robustness, strong mechanism characterizations, and new conceptual insights into the role of higher-order information. The work marks a significant advancement in the study of mechanism design with AI-generated or unreliable predictions and opens several directions for extending these ideas to more general and dynamic market environments.

Reference: "Optimal Pricing with Unreliable Signals" (2604.02758)