- The paper introduces Lévy-Flow models that replace Gaussian bases with heavy-tailed VG and NIG distributions to effectively capture financial extreme events.

- It proves that asymptotically linear normalizing flows preserve the tail index, ensuring that risk metrics remain accurate in both central and tail regimes.

- Empirical results demonstrate significant improvements in negative log-likelihood and risk calibration, with robust performance even during crisis periods.

Lévy-Flow Models: Heavy-Tail-Aware Normalizing Flows for Financial Risk Management

Motivation and Theoretical Advances

Lévy-Flow models address the entrenched challenge in financial risk management: accurate modeling of return distributions with heavy tails, where standard Gaussian-based normalizing flows systematically underestimate the probability of extreme events. This underestimation leads to insufficient capital allocation and inadequate risk buffers. By replacing the Gaussian base distribution in normalizing flows with heavy-tailed Lévy process-based distributions—specifically Variance Gamma (VG) and Normal-Inverse Gaussian (NIG)—Lévy-Flows simultaneously capture peaked centers and heavy tails while preserving exact density computation and facilitating efficient, differentiable sampling.

The theoretical centerpiece is the proof that for any base with a regularly-varying (power-law) tail, the tail index is preserved under asymptotically linear normalizing flows. This result is highly nontrivial, as it ensures that expressiveness afforded by the invertible transformation does not distort tail risk, maintaining the essential characteristics needed for extreme value analysis. Additionally, it is shown that the identity-tail structure of Neural Spline Flows (NSF) preserves the tail behavior of any base exactly outside the spline region, a property that is influential in risk calibration as many financial events lie in extreme quantiles.

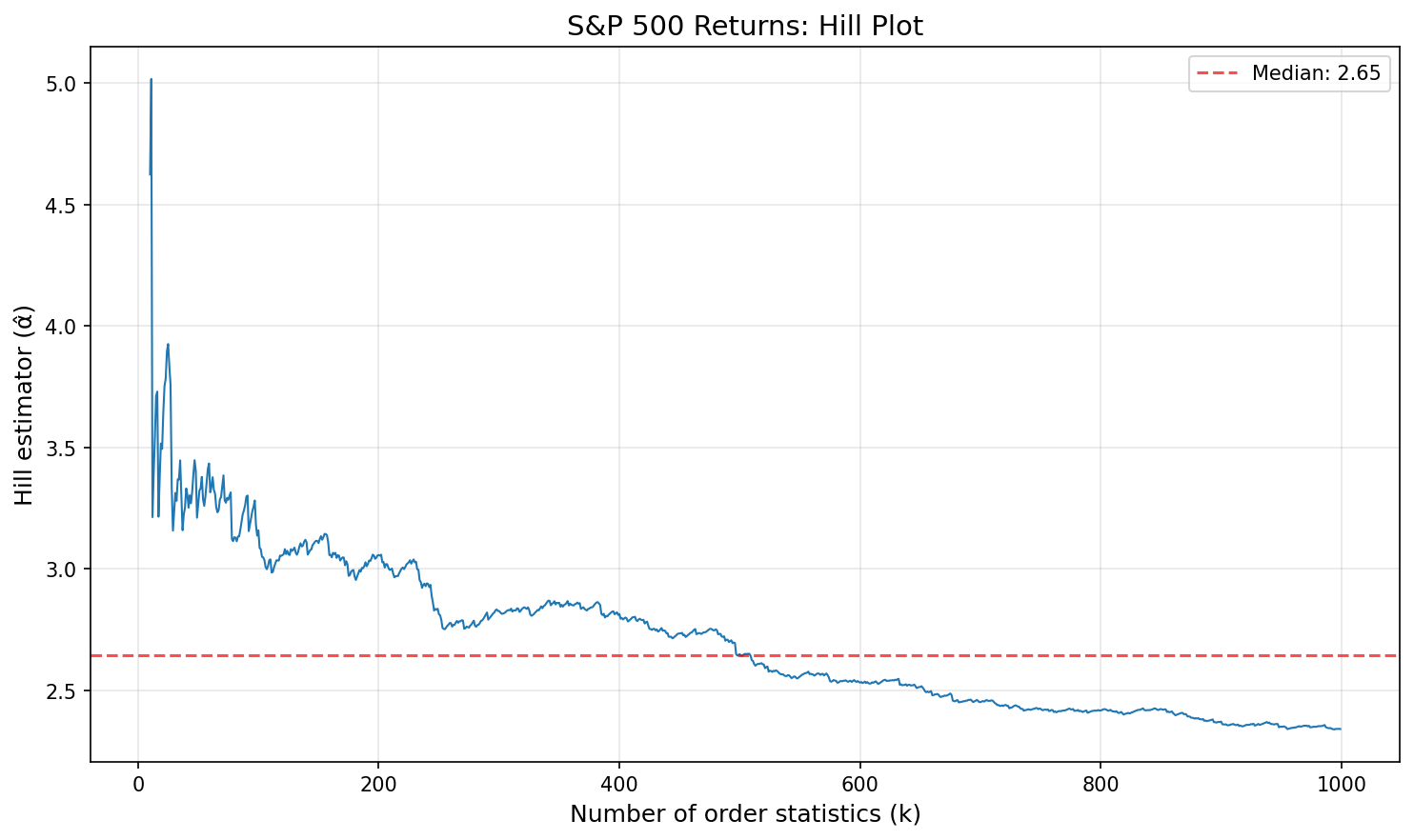

Figure 1: A Hill estimator applied to S&P 500 returns estimates a tail index near 2.5, empirically rejecting Gaussianity and motivating the use of heavy-tailed Lévy bases.

Lévy-Flow Model Construction and Properties

Lévy-Flows are defined by mapping a Lévy base (VG or NIG) through an expressive invertible transformation parameterized as a NSF. The critical architectural detail is the tail-bounded NSF: outside a predetermined threshold (e.g., ∣x∣>5 in standardized units), the transformation is exactly the identity, ensuring that the outer tails of the transformed distribution match the base without distortion.

This construction enables precise control over tail behavior. For power-law bases (e.g., Student-t), the regular variation is provably preserved asymptotically; for semi-heavy-tailed bases (VG, NIG), tail preservation holds by construction due to the identity mapping outside the spline region. Both VG and NIG have additional parametric structure not present in power-law tails: VG arises via Gamma subordination of Brownian motion and enables semi-heavy tails with closed-form density, while NIG admits flexible skewness and kurtosis via subordination by an inverse Gaussian process.

Implementation Regimen

Efficient training requires differentiable, reparameterized sampling from the VG and NIG bases. The VG is sampled by combining Gamma and Gaussian variates, while NIG uses an Inverse Gaussian and Gaussian. Careful implementation of special functions, notably the modified Bessel function for VG and NIG, is required for stability—log-domain calculations and exponentially scaled representations are employed to prevent overflow.

Data are standardized prior to modeling, and likelihood corrections reflect the Jacobian of normalization. All model evaluations—density estimation and risk metrics—are performed on identically processed data for comparability.

Empirical Analysis

Density Estimation

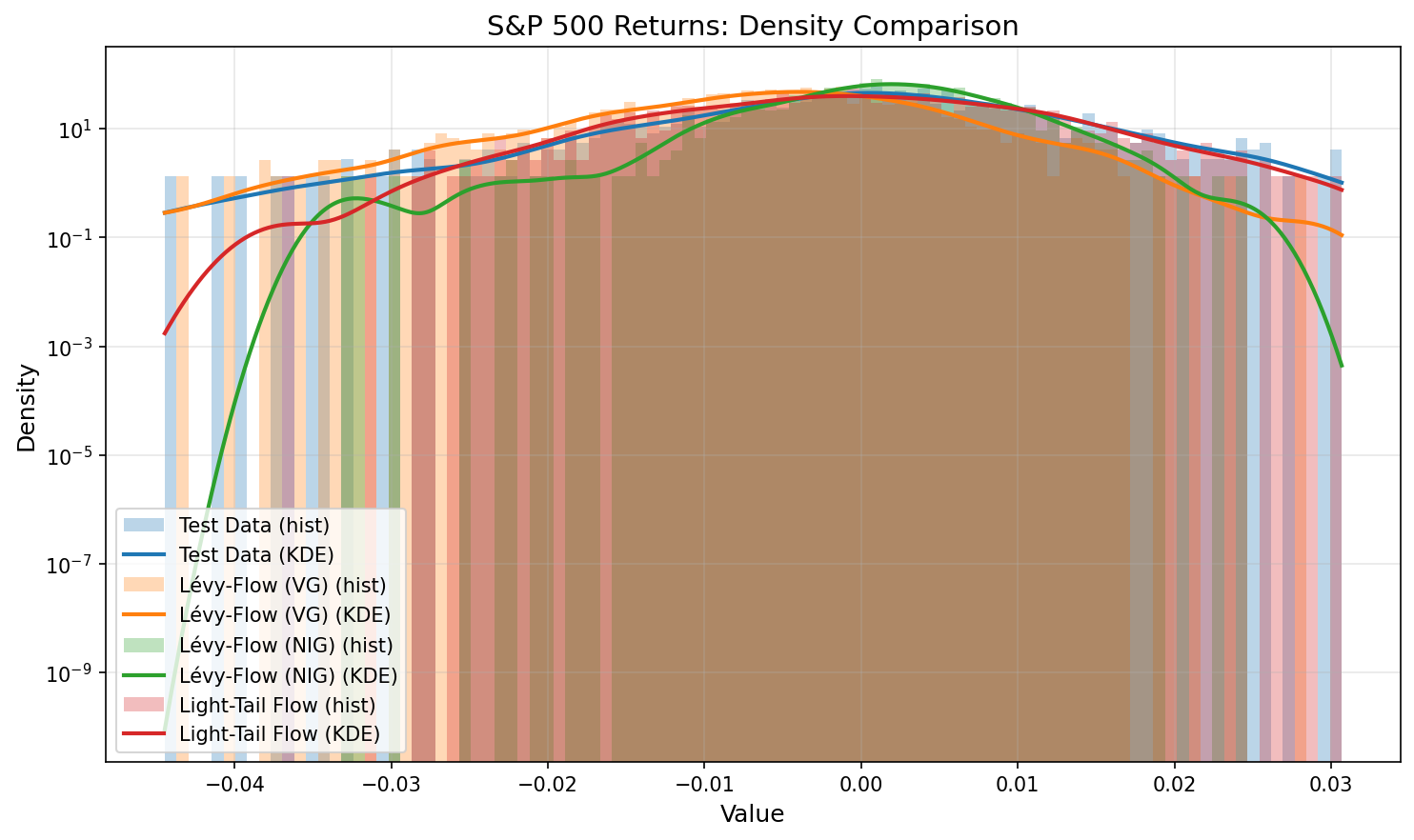

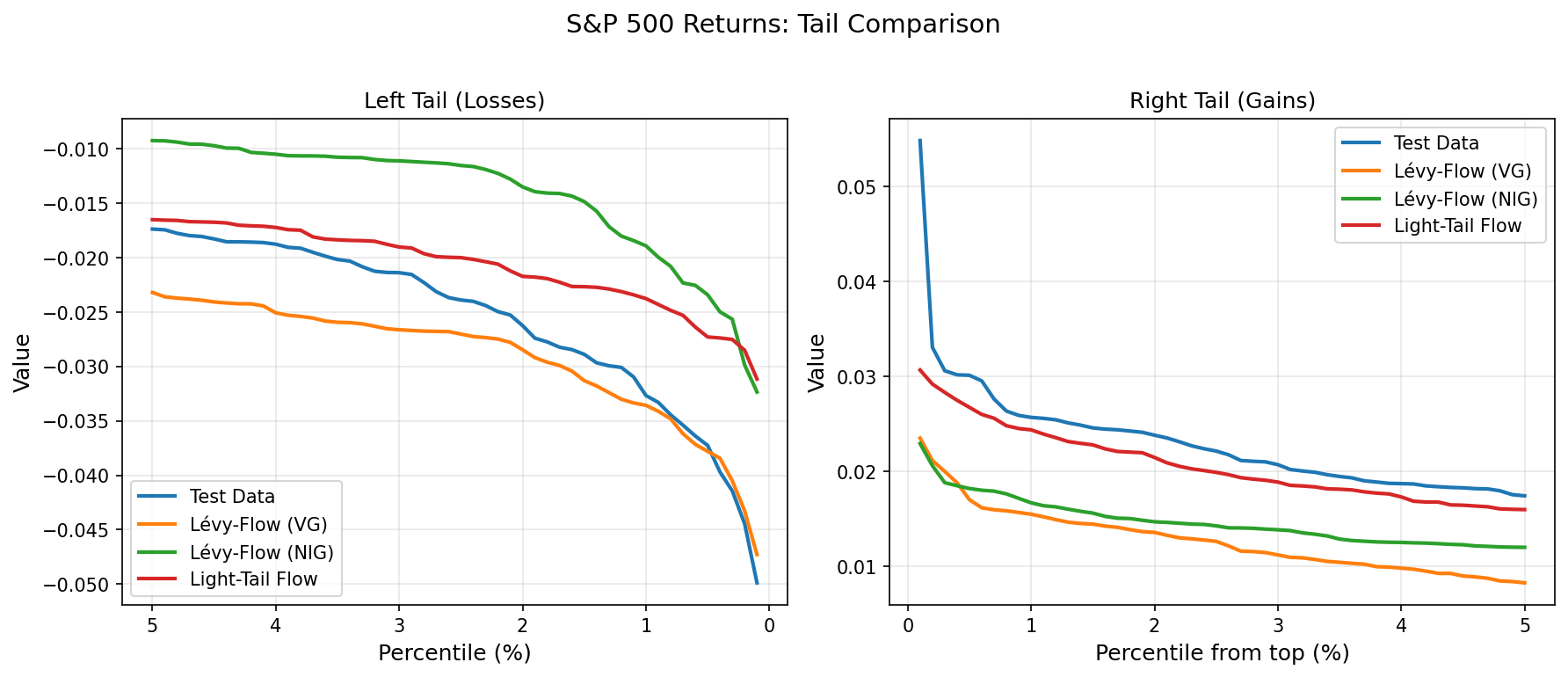

On S&P 500 daily log-returns (2000–2025, 6,514 points), Lévy-Flows (VG, NIG) match empirical data in both central and tail regimes more accurately than Gaussian- or Student-t-base flows.

Figure 2: VG/NIG-based Lévy-Flows capture the peak and tails of the empirical S&P 500 distribution, surpassing Gaussian flows.

Figure 3: On a logarithmic scale, Lévy-Flows maintain meaningful probability mass in the tails, whereas Gaussian flows systematically underestimate extreme-event probabilities.

The negative log-likelihood (NLL) comparison on held-out data demonstrates a pronounced advantage:

- Lévy-Flow (VG): 69% lower NLL than Gaussian-Flow

- Lévy-Flow (NIG): 53% lower NLL

- Student-t Flow yields negligible improvement, challenging the notion that mere tail heaviness suffices.

Tail Calibration and Risk Metrics

Risk calibration is examined via rolling-window backtests for regulatory measures: Value-at-Risk (VaR) and Expected Shortfall (ES) at 95% and 99% thresholds.

Lévy-Flow (VG) achieves exact 95% VaR calibration (Kupiec p=1.00), and NIG-based flows achieve the most accurate ES (99% ES underestimation only 1.6% versus empirical, compared to 10.4% underestimation for Gaussian). At extreme levels, all Lévy-based models exhibit conservative coverage—a preferred trait for financial risk applications—without the overconservatism of low-degree Student-t bases.

Crisis-period analyses (e.g., 2008 crash, 2022 correction) show that Lévy-Flows extrapolate sensibly to levels beyond observed data, providing plausible VaR estimates where Gaussian-based flows are far too optimistic and Student-t flows become excessively conservative. This supports the central claim that Lévy parametric structure, which includes features beyond tails such as skewness and subordination, is responsible for performance.

Multi-Asset Evaluation

The strong outperformance of Lévy-Flows generalizes to other assets with higher kurtosis and non-Gaussian characteristics (AAPL, EEM, Gold futures), though the largest gains arise in assets with the most pronounced heavy tails.

Implications and Future Directions

From a practical perspective, Lévy-Flows present a methodology for density estimation and risk calibration that outperforms existing Gaussian and Student-t-based approaches, meeting both regulatory and economic standards. Theoretically, the preserved tail index under asymptotically linear flows and identity-tail guarantee for semi-heavy bases offer a blueprint for developing generative models where tail extrapolation is controlled—a crucial property lacking in generic likelihood-based flows and neural generative models.

These results motivate several extensions:

- Full multivariate generalization: extending Lévy-Flows to high-dimensional portfolios with proper copula or Lévy subordinator structures.

- Conditional Lévy-Flow architectures: adapting base parameters across market regimes, potentially integrating volatility modeling.

- Broader study of Student-t parameter space: to precisely quantify the additional benefits (beyond power-law tails) of the richer Lévy base structure.

- Extending formal risk backtesting: applying ES backtesting and rolling evaluations to a wider range of assets and timeframes.

Conclusion

Lévy-Flow models, coupling heavy-tailed, infinitely divisible Lévy bases with modern invertible transformations, furnish a robust framework for modeling financial returns and associated risks. Theoretical guarantees of tail preservation through the flow, coupled with strong empirical improvements in likelihood and risk calibration, position Lévy-Flows as a preferred approach in applications where tail accuracy is paramount. The parametric sophistication of VG and NIG bases, as opposed to simple power-law alternatives, underpins these advances and should inform future directions in risk-sensitive generative modeling.

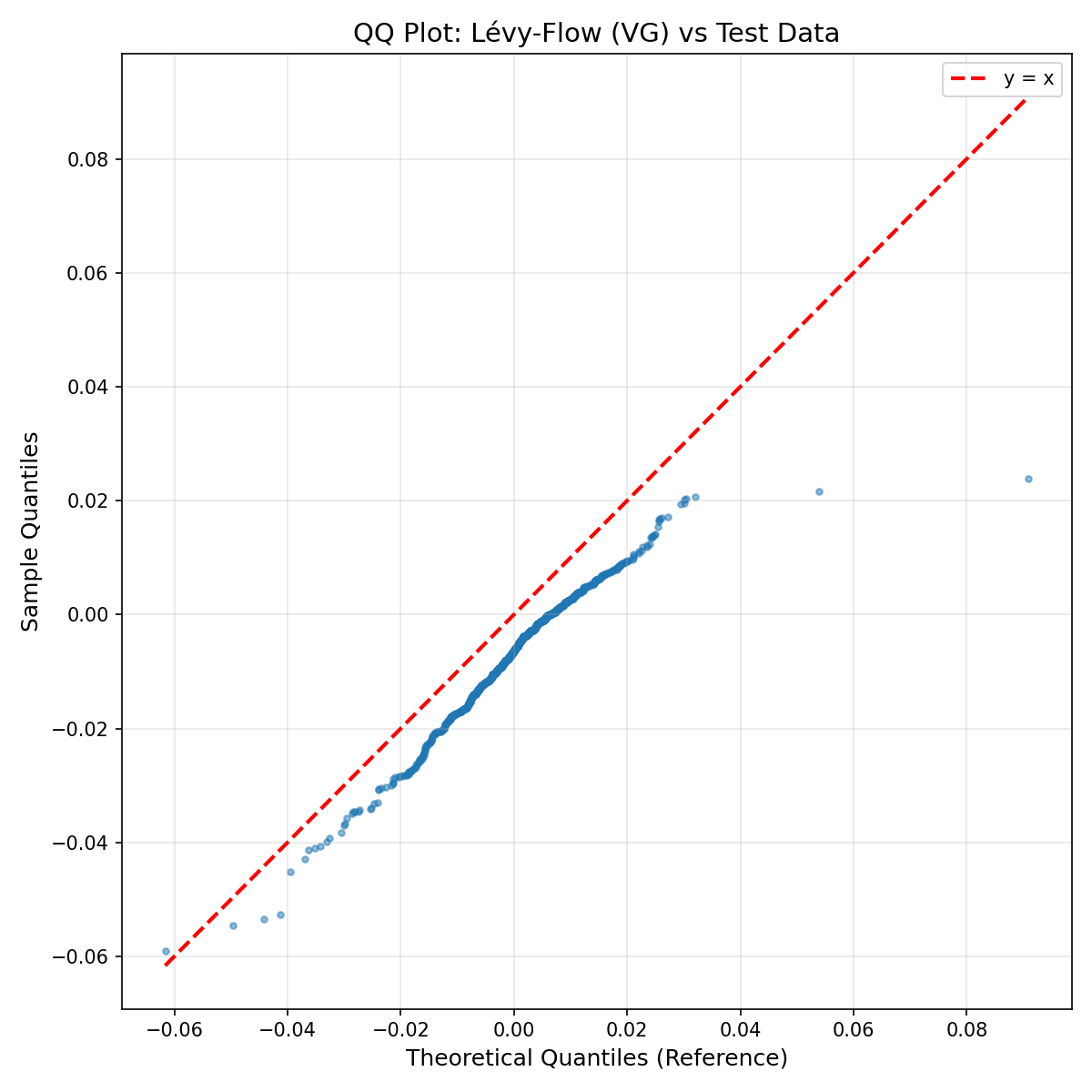

Figure 4: Illustration of the Lévy-Flow (VG) transformation architecture, combining a heavy-tailed Variance Gamma base with invertible spline flows.