- The paper introduces a three-dimensional model that combines Goodwin wage–employment dynamics with Minsky debt feedback to establish explicit bifurcation conditions for business cycle selection.

- The paper employs center manifold theory and Hopf bifurcation analysis to derive parameter-dependent criteria, showing the transition from stable equilibrium to sustained oscillations at small positive interest rates.

- The paper validates its analytical findings with numerical simulations that track limit cycle amplitudes and periods, underscoring the influential role of investment sensitivity and credit conditions in macroeconomic dynamics.

Endogenous Business Cycle Selection in the Keen–Goodwin–Minsky Model with Debt Dynamics

Introduction

This paper presents a rigorous dynamical systems analysis of a three-dimensional Keen–Goodwin model augmented with Minsky-style debt accumulation mechanisms. The framework explicitly integrates wage–employment (Goodwin) dynamics with private sector debt feedbacks (Minsky/Keen). The investigation addresses the structure, selection, and stability of endogenous business cycles arising from intrinsic macro-financial interactions, focusing on the roles of investment responsiveness and real interest rates in the selection of cyclical or equilibrium behavior.

The model extends the classical Goodwin wage–employment cycle by including private sector debt as a state variable d, yielding a three-dimensional nonlinear continuous-time system for (ω,λ,d), where ω is the wage share, λ is the employment rate, and d is the private debt-to-output ratio. The system's structural parameters encompass productivity growth (α), labor force growth (β), depreciation (δ), and the capital–output ratio (ν), with firms borrowing at real interest rate r.

The wage share follows a Phillips-type wage bargaining law, employment is determined by capital accumulation adjusted with investment as a function of profits, and debt dynamics are governed by the gap between investment needs and retained profits, plus interest payments. Profit share incorporates the debt cost term (ω,λ,d)0, which acts as a coupling parameter. The investment function (ω,λ,d)1 is an increasing function of profit share, embedding accelerator effects.

Bifurcation Analysis: Center Manifold and Hopf Transition

A principal focus is the local bifurcation structure around the "good" interior equilibrium associated with positive economic variables. For (ω,λ,d)2, the equilibrium is non-hyperbolic with two purely imaginary eigenvalues in the wage–employment block, resulting in a two-dimensional center manifold organizing a continuum of neutral cycles of Goodwin type. The debt variable is slaved to (ω,λ,d)3 through a forced linear equation, creating a foliation of periodic orbits in the phase space.

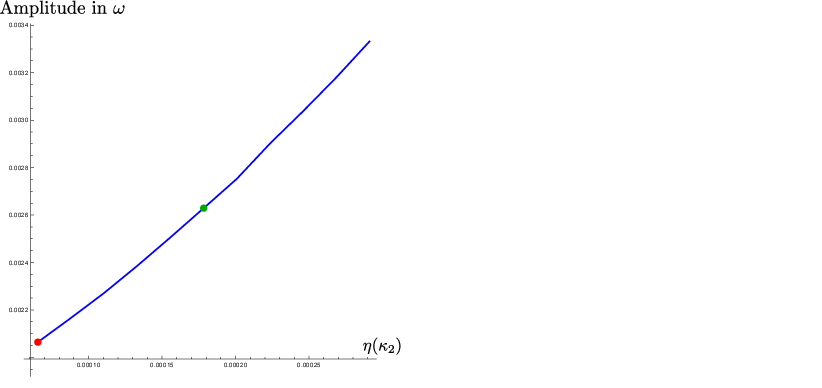

Figure 1: Amplitude of the periodic orbits in (ω,λ,d)4 as a function of (ω,λ,d)5. Each point corresponds to a periodic orbit. The red and green markers indicate the two representative periodic orbits used for comparison.

When (ω,λ,d)6, the debt feedback modifies the stability of the equilibrium through the debt cost in profits ((ω,λ,d)7), breaking the spectral degeneracy. An explicit Hopf bifurcation condition is derived, depending on (ω,λ,d)8, where (ω,λ,d)9 quantifies the sensitivity of investment to profitability and aggregate leverage. For small ω0, the degeneracy at ω1 is unfolded, and a unique limit cycle emerges through a Hopf bifurcation as the analytically computed critical value is crossed. The sign of ω2 determines whether the equilibrium is stable or gives rise to sustained endogenous oscillations. This is an exact, parameter-dependent codimension-one bifurcation criterion.

Center Manifold and Invariant Manifold Persistence

The existence and structure of the center manifold at ω3 is constructed explicitly, including its nonlinear embedding in the full ω4 state space. Applying persistence theorems, notably Fenichel's normal hyperbolicity theory, the two-dimensional center manifold is shown to persist as an invariant manifold for sufficiently small ω5. The flow on this slow manifold can be reduced to planar slow–fast amplitude–phase equations by coordinate projection and phase reduction, justified by strict spectral separation.

Phase–Amplitude Reduction and Analytical Corrections

The global reduced dynamics for small ω6 are formalized using phase–amplitude reduction. By constructing adjoint modes and projecting the system's perturbations, the authors obtain leading-order corrections to both the frequency and amplitude of the emergent limit cycle. These corrections are explicitly computed as integrals over the periodic orbits of the unperturbed system, providing quantitative, computable links from macroeconomic parameters (especially investment elasticity, capital–output ratio, and interest rate) to observable business cycle features (amplitude, period, stability).

Numerical Continuation and Validation

Comprehensive numerical simulations complement the theoretical results. By varying the parameter ω7, which tunes the slope of the investment function (i.e., investment's sensitivity to profit share), the authors track the bifurcation curve and numerically locate the Hopf threshold, confirming close agreement with the analytical condition ω8. The amplitude and period of the limit cycles following bifurcation are calculated and shown to scale smoothly with the bifurcation parameter, consistent with supercritical Hopf behavior. Detailed Floquet multiplier computations demonstrate that periodic orbits are transversely attracting for parameters near the threshold, confirming their dynamical relevance.

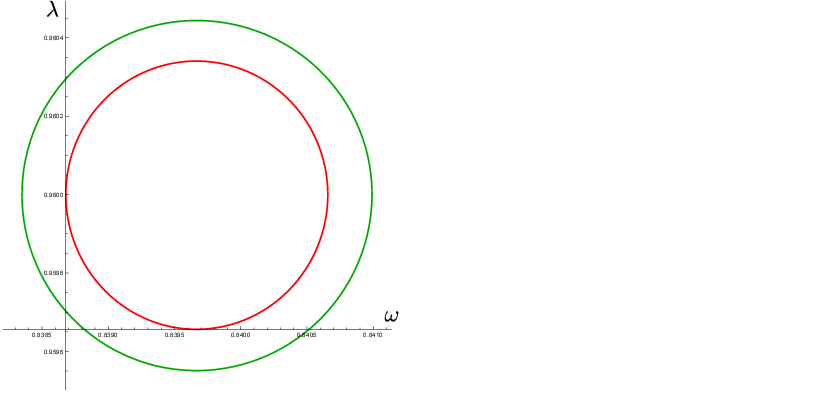

Figure 2: Comparison of two representative periodic orbits in the phase plane ω9. The red orbit corresponds to λ0, the green to λ1.

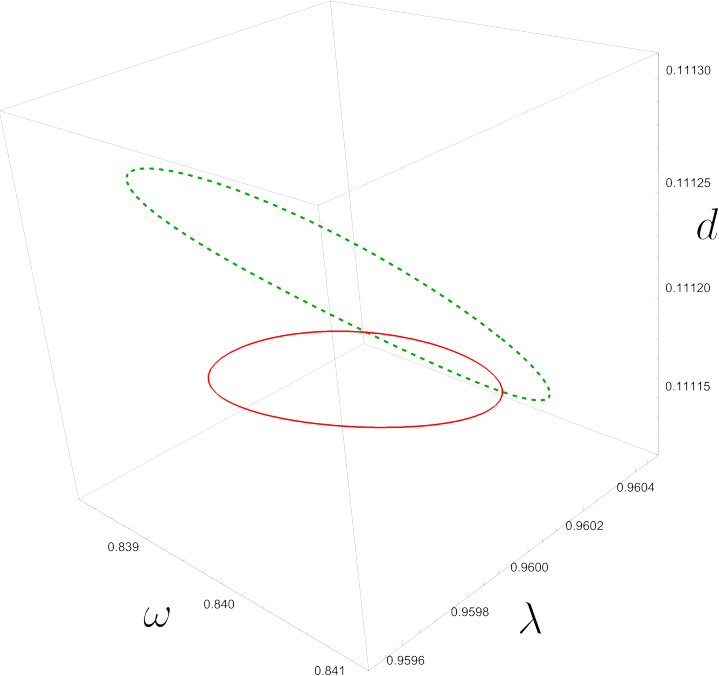

Figure 3: Comparison of the two representative periodic orbits (red and green) in the full state space λ2, illustrating how the debt variable embeds the planar dynamics into a three-dimensional invariant manifold.

The figures illustrate the relationship between bifurcation parameter values, oscillation amplitude, and the embedding of wage–employment cycles within the three-dimensional state space shaped by debt feedback.

Economic and Theoretical Implications

This study establishes that endogenous cycles in the Keen–Goodwin–Minsky system are robust, locally selected phenomena, not mere numerical artifacts. The explicit bifurcation conditions verify that for economically plausible parameter values, even small positive interest rates are sufficient for the transition from stable equilibria to persistent business cycles. The main bifurcation parameter, a function of leverage and investment elasticity, provides a rigorous channel by which monetary and credit conditions—through interest rate policies or financial regulation—shape macroeconomic cycle selection and stability.

Contrary to narratives attributing business cycles primarily to exogenous shocks, the results here show that intrinsic financial–real interactions create robust, structurally selected oscillatory regimes without recourse to stochastic forcing. From a theoretical perspective, the application of center manifold theory, Hopf bifurcation analysis, and modern geometric perturbation provides a mathematically rigorous basis for the emergence, selection, and modulation of business cycles in integrated macro–financial models.

Conclusion

The paper delivers a comprehensive bifurcation-theoretic account of endogenous cycle selection driven by debt accumulation in the Keen–Goodwin–Minsky framework. The combined use of center manifold reduction, normal hyperbolicity theory, phase–amplitude analysis, and numerical continuation establishes a detailed, quantitative mapping from model primitives to business cycle characteristics. The explicit dependence of cycle selection on financial parameters such as interest rate and investment responsiveness affirms the critical role of credit frictions in macroeconomic dynamics and provides actionable foundations for further calibration, empirical study, and extension to higher-dimensional or policy-augmented macro–financial systems.