- The paper proposes an EVT-based diagnostic test to assess the thin-tailed error assumption in binary choice models using the behavior of extreme order statistics.

- It demonstrates that the right tail behavior of heavy-tailed covariates can reveal latent error structures, with significant applications in areas like trade, innovation, and labor participation.

- Monte Carlo simulations and empirical examples validate the test’s robustness, invariance to scale/location changes, and its utility in addressing model misspecifications.

A Simple and Powerful Diagnostic Test for Binary Choice Models

Introduction and Motivation

The paper "A Simple and Powerful Diagnostic Test for Binary Choice Models" (2603.27881) addresses a fundamental yet under-examined aspect of binary response econometrics: the appropriateness of the thin-tailed error assumption underlying conventional logit and probit specifications. While these models possess wide empirical ubiquity due to tractable index structures and efficient estimation, their default imposition of thin-tailed (normal or logistic) latent errors can be substantively restrictive in contexts where rare, large shocks are empirically salient. The authors develop a practical, theoretically grounded diagnostic to test the validity of the thin-tail assumption by exploiting extreme value theory (EVT) and the information carried by the most extreme values of heavy-tailed covariates.

Theoretical Framework

The central innovation of the paper is to establish that in the canonical threshold-crossing binary choice model,

Yi=I(Xi−εi≥0),

with I denoting the indicator function, Xi a heavy-tailed covariate, and εi the latent error, the tail behavior of εi imposes observable restrictions on the conditional extremes of Xi given Yi. Specifically, among Yi=0, the largest observed Xi are coupled with extreme values of εi, and thus the right tail of I0 asymptotically reflects the right tail structure of I1.

Employing EVT, the tail index I2 of the error is mapped to the tail index I3 of I4 via a functional relationship,

I5

where I6 is the tail index of I7. Thus, testing for the thin-tailed case I8 is equivalent to testing whether I9, i.e., whether the observed conditional tail is also thin.

This mapping holds generally under mild regularity—domain of attraction and von Mises conditions, satisfied by nearly all common distributions. Dominance conditions are formulated for multiple regressors, requiring only one observable covariate with a regularly varying (heavy) tail for identification.

Test Construction and Invariance Properties

The proposed test operationalizes the above equivalence by comparing the empirical spacings of the largest Xi0 order statistics of Xi1 to their predicted distribution under thin-tailed errors, exploiting maximum-invariance. No model parameter estimation is required, and no particular parametric form for the link function is imposed.

Under the null, normalized top-Xi2 spacings have a limiting Gumbel law; departures from this (captured via a fixed-Xi3 likelihood ratio test integrating over alternatives for Xi4) indicate heavier tails. The test is complemented by a Bonferroni correction for joint left and right tail tests due to symmetry under standard nulls.

Notably, the test is invariant to scale and location transformations of the covariate, can operate purely via order statistics, and is agnostic about the parametric form of the remaining index in multivariate contexts so long as at least one heavy-tailed covariate dominates.

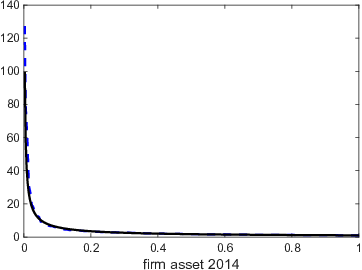

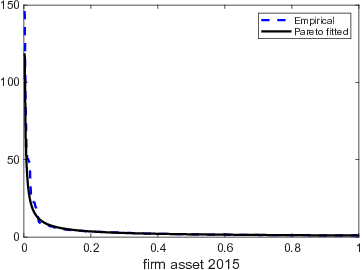

Figure 1: Pareto fit of firm assets among non-exporters (Xi5); the empirical distribution closely aligns with the fitted Pareto in the upper tail.

Extensions: Multivariate and Panel Models

The methodology generalizes straightforwardly to regimes with multiple covariates—one need only identify a tail-dominating regressor, typically one observable and heavy-tailed (e.g., firm assets, income). The asymptotic justification is robust to the inclusion of additional, discrete or thin-tailed regressors, which are asymptotically dominated in the tail behavior of the index.

For static and dynamic short-Xi6 panel data with fixed individual effects, including predetermined regressors and initial condition problems, the test remains valid. Under maintained conditions, it obviates the need for challenging bias corrections (contrasted with conventional panel probit models) and avoids the incidental parameters problem, since it requires no coefficient or effect estimation.

Monte Carlo Evidence

The test demonstrates strong finite-sample performance in extensive simulations. It achieves correct size under the null for both normal and logistic errors and displays high power against heavy-tailed alternatives (Student-Xi7 errors), with power rising in Xi8 (number of tail observations) and tail index magnitude, particularly when covariate tails are sufficiently heavy. Sensitivity is robust to sample size, though the fixed-Xi9 asymptotics guard against size distortions that would arise with excessive inclusion of mid-distribution observations.

Empirical Applications

The empirical relevance of the approach is established through three high-stakes economic instances:

- Firm Export Participation and Innovation:

- The method is deployed on Chinese administrative data where firm asset size is empirically heavy-tailed. For both export and innovation decisions, the right tails of the asset distribution among non-exporters/non-innovators align with Pareto approximations and are demonstrably inconsistent with the thin-tail null (see Figure 1). Rejection εi0-values rapidly decline with εi1, indicating that large unobserved shocks—possibly reflecting policy, strategic, or market access frictions—play critical roles in such extreme discrete outcomes.

- Female Labor Force Participation:

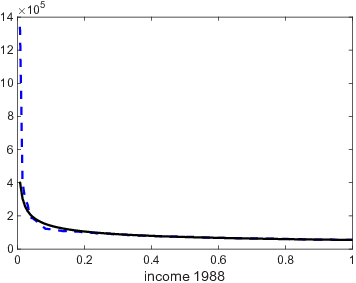

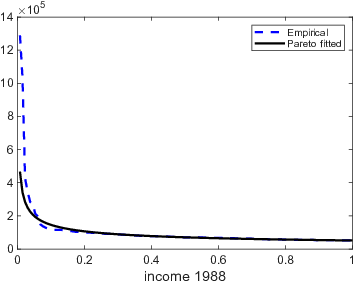

- Using PSID data, the test is applied to the conditional distribution of husband's income among non-participants (Figure 2 demonstrates tail fit), revealing tail indices in the range εi2 and easily rejecting thin-tailed nulls from the mid-1980s onward. Such findings challenge the common assumption of normality in panel binary response models and suggest latent shocks with potential macro or institutional drivers.

Figure 2: Pareto fit of husband's income among women not in the labor force (εi3), confirming the appropriateness of a heavy-tail model.

Practical and Theoretical Implications

The approach identifies and targets a source of model misspecification not easily ascertained using standard residual or link function-based specification tests. It operates as a powerful pre-estimation diagnostic, guiding whether standard logit/probit models are even econometrically defensible given observed conditional covariate behavior. Modelers are cautioned that, in fields where rare but large shocks are plausible (e.g., trade entry, innovation, labor supply), diagnostic application may frequently reject logistic or normal error hypotheses and accordingly recommend semiparametric, robust, or heavy-tailed specifications.

Methodologically, the test highlights the potential for EVT-based diagnostics in discrete choice and limited dependent variable contexts. Extensions to multinomial settings and data-driven optimal selection of εi4 are natural avenues for further research.

Conclusion

The paper provides a theoretically transparent, computationally minimal, and empirically robust solution to testing the thin-tail assumption in binary choice models. By leveraging observable conditional extremes, rather than unestimable latent errors or full likelihood modeling, researchers gain a calibrated, size-controlled diagnostic for extreme-value misspecification. The implications are both practical—guiding the preliminary assessment of model suitability—and theoretical, reinforcing the need for greater scrutiny of distributional assumptions in applied discrete choice econometrics.

Key empirical findings—statistically significant rejection of thin-tailed errors in canonical datasets—underscore the limitations of conventional probit/logit in the presence of observable heavy-tailed covariates. The path forward is clear: incorporate tail diagnostics as a standard complement to binary model specification analysis, particularly in domains characterized by potential rare extreme events.