- The paper’s main contribution is the formulation of explicit local risk-minimization strategies for exponential additive processes in incomplete markets.

- It establishes explicit integrability and structural conditions ensuring the existence and square-integrability of the minimal martingale measure using Malliavin-Skorohod calculus.

- The work also provides numerically tractable representations via the Carr-Madan method, validated through experiments on the VGSSD model.

Local Risk-Minimization for Exponential Additive Processes

Introduction and Motivation

This paper develops the theory of local risk-minimization (LRM)—a quadratic hedging approach in incomplete markets—for models where the asset price follows an exponential additive process. Unlike Lévy processes, additive processes possess a time-dependent Lévy measure, introducing significant technical and conceptual challenges in formulating hedging strategies. Notably, the paper supplies explicit representations of LRM strategies under a comprehensive set of integrability and structural conditions, and reproduces these formulas in numerically tractable forms that leverage the Carr-Madan method for efficient computation.

The research expands the existing literature by systematically addressing the mathematical and numerical obstacles arising from non-stationary jump dynamics. It rigorously clarifies and corrects prior work on additive processes, proposing new sufficient conditions for key properties such as the existence and square-integrability of the minimal martingale measure (MMM), and adapting Malliavin-Skorohod calculus results to this setting.

Mathematical Formulation and Main Results

The risky asset price, St, is modeled as an exponential of an additive pure-jump process Lt, i.e., St=S0exp(Lt). The law of Lt is infinitely divisible with a generating triplet (0,νt,γt), but crucially the measure νt now depends on t. This time-inhomogeneity precludes the direct application of results valid for Lévy processes and compels new technical developments, particularly regarding integrability and martingale properties.

Structural and Integrability Conditions

The paper establishes a set of explicit conditions—denoted (A1)–(A6)—that ensure well-posedness of the model, integrability of the price process, and the existence and properties of the MMM. These assumptions are primarily cast as tractable constraints on the Lévy measure (for example, ∫0T∫∣x∣>1e4xν(ds,dx)<∞), encompassing the time-inhomogeneous nature of the jumps.

One key novelty is the derivation of sufficient conditions that guarantee both the structure condition (SC) and the square-integrability of the MMM Z=E(Mλ). These results require delicate handling of the time-varying jump measure and explicit estimates for quantities such as θt,x, the Girsanov kernel.

Explicit LRM Strategies

The LRM strategy for a square-integrable claim F reduces to the integrand ξt1,F in the Föllmer–Schweizer decomposition of F, which in this model is given (for a call F=(ST−K)+) by

ξt1,F=St−Σt1∫R0EP∗[Ψt,xF∣Ft−](ex−1)π(t,x)dx,

where Σt=∫(ex−1)2π(t,x)dx, and P∗ is the MMM. The operator Ψt,xF essentially evaluates the impact of adding a jump at time t of size x to the underlying path, and these calculations are situated within a Malliavin-Skorohod calculus framework appropriate for additive processes.

The mathematical validity of these formulas is rigorously established by verifying all required conditions (including a reverse Hölder inequality for Z) under the paper’s integrability assumptions.

Numerically Tractable Representations

To address computational concerns, the paper translates the previously obtained formulas into forms suitable for FFT-based algorithms, with specific attention to the Carr-Madan framework. The core is the efficient calculation of conditional expectations under the MMM, whose characteristic function is computed explicitly through an analysis of the Girsanov-transformed process and the time-inhomogeneous Lévy measure.

For instance, the price of a call option under P∗, conditional on current information, is written as

EP∗[(ST−K)+∣Ft−]=π1∫0∞K−iu−R+1(iu+R−1)(iu+R)ϕt,T∗(u−iR)St−iu+Rdu,

where ϕt,T∗ is the characteristic function of the log price increment LT−Lt under the MMM. The inner integral in the expression for ξt1,F is further reduced to differences of cumulant generating functions, making numerical implementation straightforward.

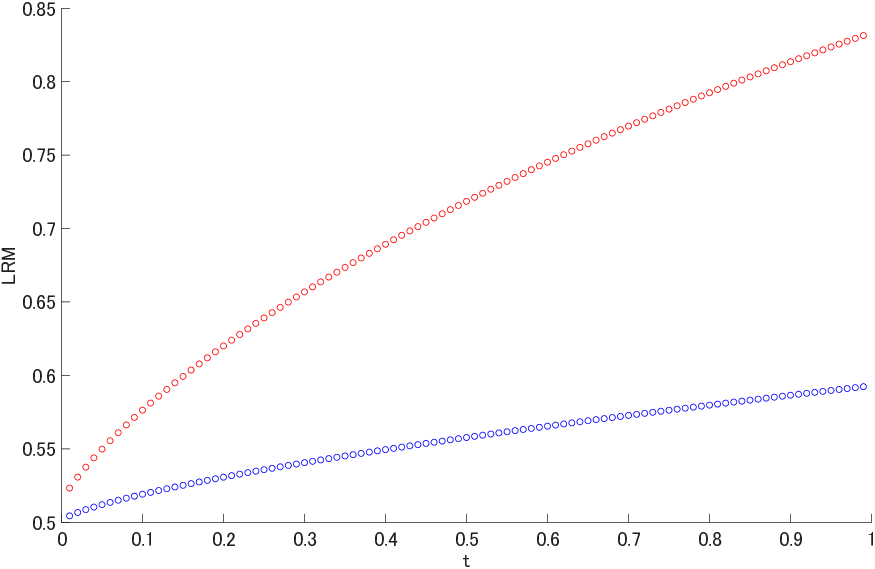

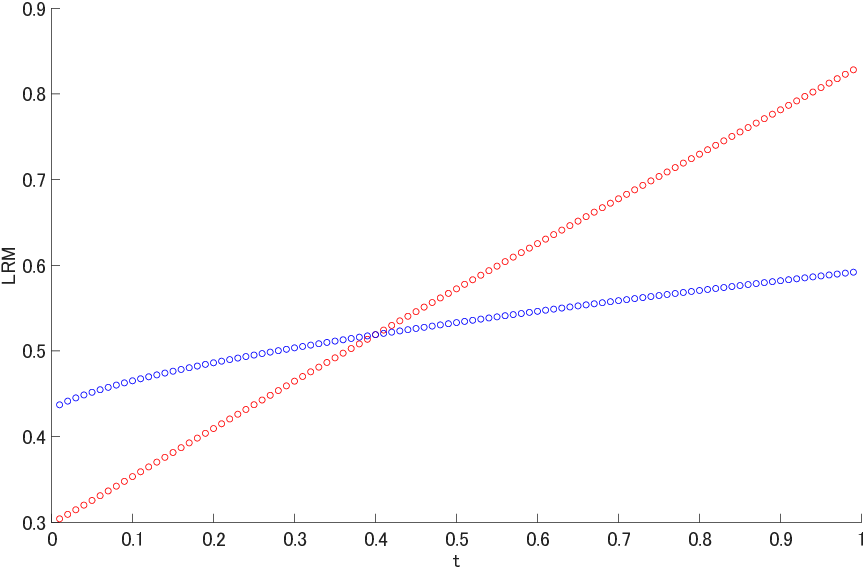

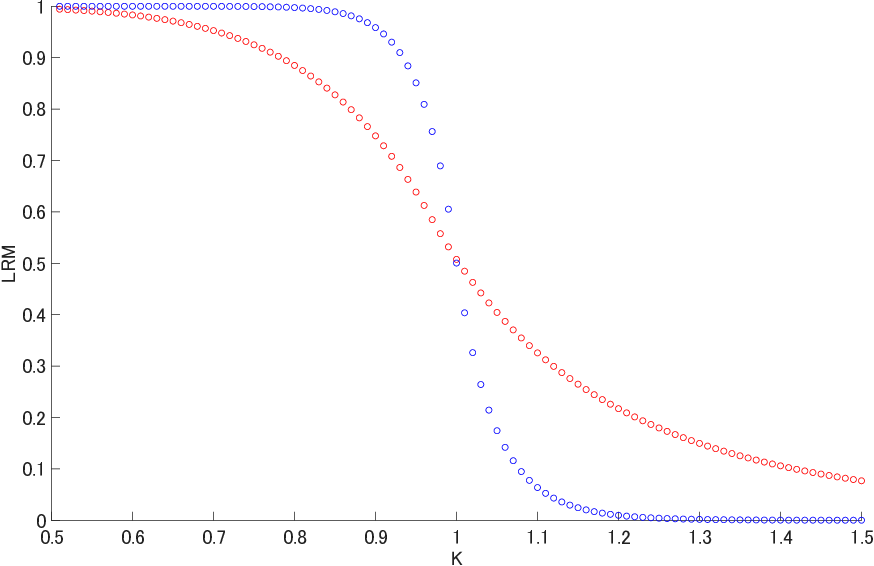

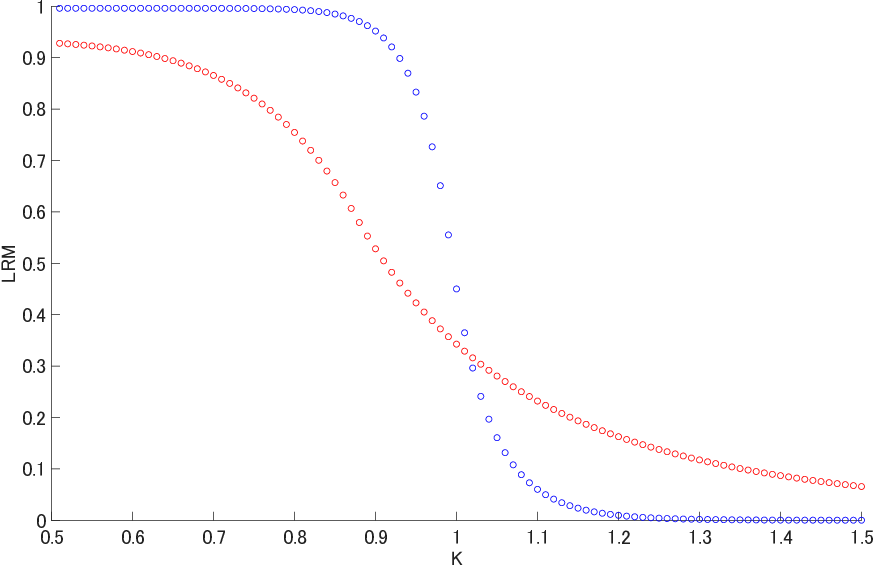

Numerical Experiments: The VGSSD Model

As a primary example of the theory, the paper investigates the Variance-Gamma Scaled Self-Decomposable (VGSSD) process, generalizing the classical variance gamma process to the additive (non-stationary) case. Explicit forms for the Lévy density and drift are derived, and formula simplifications for qt(z) and lt(z) are provided, notably enabling fast computation.

Numerical experiments validate the practical applicability and stability of the closed-form LRM strategies. Two main scenarios are considered: varying the hedging time (thus varying time-to-maturity for at-the-money options), and varying the option strike (thus traversing from deep-in-the-money to out-of-the-money). The results demonstrate that the magnitude and sensitivity of optimal hedge positions are modulated both by the time-inhomogeneous jump structure and the choice of the parameter M in the VGSSD process.

Figure 1: (A1, A2) LRM strategy values for ATM calls as a function of time-to-maturity. (B1, B2) LRM strategy values for varying strikes at fixed maturity, comparing M=4 and M=16 for two model variants.

Theoretical and Practical Implications

The technical contribution is twofold: a precise formulation of LRM hedging in time-inhomogeneous jump environments, and a rigorous verification of all conditions required for the existence and computation of MMM and LRM strategies in this generality. The provided integrability criteria, cast in terms of the Lévy measure, are directly checkable for specific models—a significant advantage for both theoretical and applied work.

In practice, the numerical tractability of the resulting formulas—especially with respect to non-stationary processes—facilitates improved hedging risk control in incomplete markets featuring non-constant jump risk, such as time-varying event intensities or non-stationary stochastic volatility models.

Future Directions

This research opens pathways for further investigation of hedging and pricing under more general additive processes, including those with stochastic volatility or multifactor dynamics. Extensions to path-dependent options, portfolio optimization problems under time-varying jump risk, and further numerical benchmarking across real market data constitute immediate directions. The framework can potentially inform robust risk management in financial systems characterized by non-stationary and abrupt structural breaks.

Conclusion

The paper systematically generalizes LRM theory to exponential additive processes with non-stationary jump dynamics, offering explicit formulas for hedging strategies and demonstrating numerical feasibility via the VGSSD example. This work not only clarifies prior ambiguities in the literature but also equips researchers and practitioners with both the theoretical and computational means to address quadratic hedging in a wide array of practical settings.