- The paper demonstrates a novel HJB framework that integrates transient market impact with inventory risk management in spot FX market making.

- It derives closed-form optimal quotes and execution speeds, illustrating how transient decay rates adjust quoting strategies.

- Numerical simulations show that transient impact models outperform traditional permanent impact assumptions during large inventory shocks.

Market Making and Transient Impact in Spot FX

Introduction and Context

This paper addresses optimal market making in over-the-counter (OTC) spot foreign exchange (FX) trading under the empirically supported assumption of transient market impact, departing from the canonical Almgren-Chriss framework that assumes only instantaneous and permanent price impact. The study incorporates a resilient impact state into the dealer's risk-control problem, reflecting the fact that real-world execution impact decays over time, with client flows and hedging decisions altering both inventory and price dynamics. The analysis draws upon Hamilton-Jacobi-Bellman (HJB) stochastic control and offers theoretical and numerical insights into the interplay between market-maker inventory, impact persistence, hedging strategies, and optimal quoting.

Transient Impact Characterization

The author formally demonstrates that OTC FX market making induces a form of transient price impact, akin to propagator-type models. Relying on the Avellaneda-Stoikov framework with laddered trade sizes and symmetric Poisson arrivals, the baseline HJB system is extended to accommodate quadratic expansions of the value function and a mean-field relaxation of inventory after shocks. The closed-form derivation for optimal quotes reveals that price jumps upon a client trade, followed by exponential relaxation—a transient signature. The system's risk relaxation rate, ω, closely tracks empirical timescales for FX desk risk mitigation, and the dealer's quote skew directly induces temporary pricing pressure.

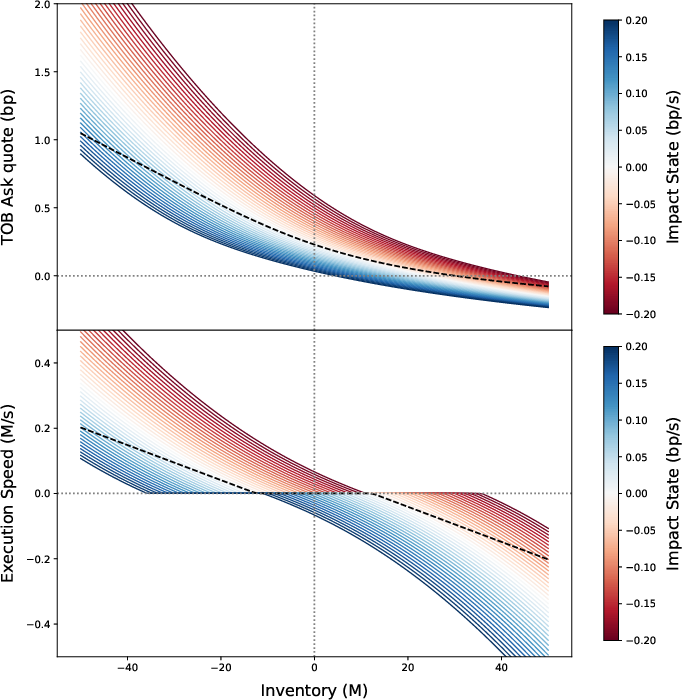

Figure 1: Optimal top of book (TOB) ask quote δ∗1,a and execution speed v∗ as inventory q and impact state x vary, with the dashed curve showing the x=0 approximation.

Hedging and Resilient Impact Model

Building on the above, the paper extends the optimization formulation by incorporating continuous hedging in the interbank market, with quadratic and linear transaction costs and exponentially decaying market impact. The mid-price evolution consists of an exogenous Brownian increment and a controlled transient component xt, which itself evolves according to the impact of dealer executions and decays at a rate β.

The HJB equation is generalized to a value function V(t,q,x) and systematically analyzed with quadratic approximations for risk aversion and impact state cross-terms. Notably, the interplay between the market-maker's inventory q and the impact state x modulates both optimal quoting (via δ∗) and execution speed v∗, dynamically adjusting the internalization zone based on transient impact feedbacks.

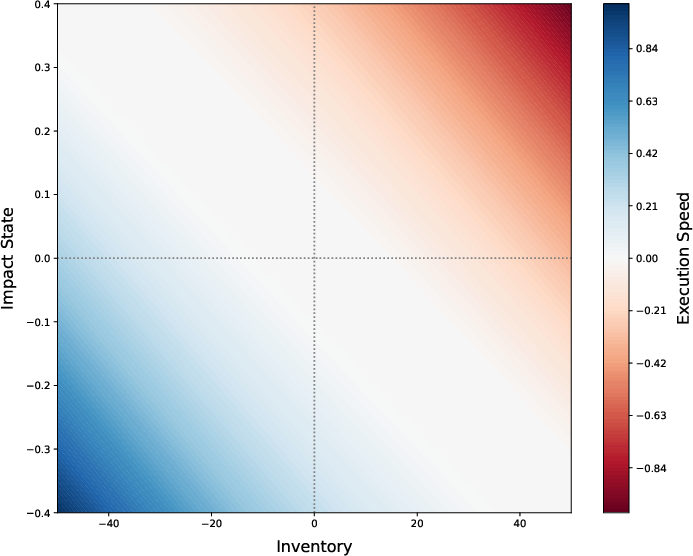

Figure 2: Two-dimensional dependence of optimal execution speed v∗ on inventory q and impact state x, with critical boundaries of the pure internalization region.

The closed-form and numerically exact solutions evidence that when impact resilience (i.e., the value of β) competes with client-flow-driven risk relaxation (ω), B0=β/(β+ω) quantifies the correction to the dealer's quoting and execution policies. When impact decays slowly (β≪ω), the system approaches the permanent impact regime; when impact decays quickly, Almgren-Chriss becomes a valid approximation.

Numerical Results and Regimes

Using a detailed parameterization for realistic spot FX market conditions, including a size ladder for trade notional, empirical intensity functions, and volatility inputs, the study numerically solves the HJB and simulates post-shock dynamics. The solutions reveal a significant and state-dependent deviation in the optimal controls compared to the permanent impact case, especially regarding the boundaries and magnitude of the internalization region.

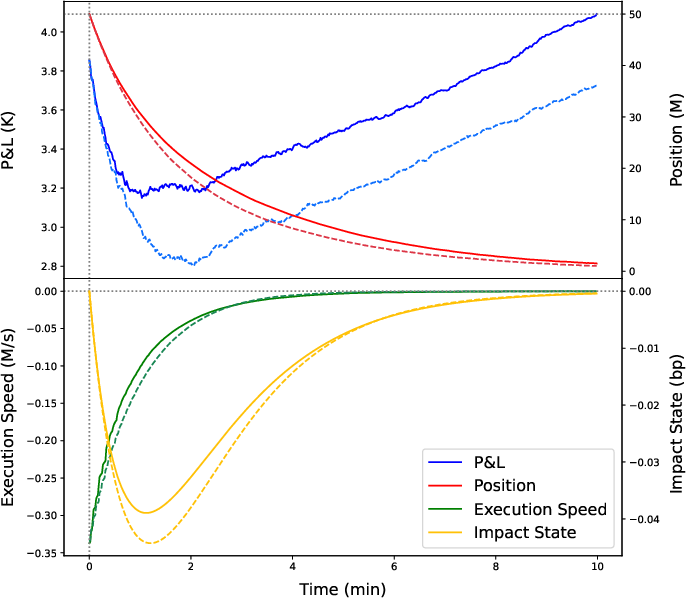

Monte Carlo simulations (Figure 3) show the full dynamical response of P&L, inventory, execution speed, and impact state post-shock. Transient impact models yield superior P&L trajectories compared to misspecified permanent impact controls during large inventory shocks, driven by better adaptation to evolving impact states.

Figure 3: P&L, inventory, execution speed, and impact state evolution after a q0=50M shock, with 10,000 Monte Carlo trajectories and comparison to the Almgren-Chriss impact solution.

However, in the practical regime where large trades are infrequent, the qualitative difference between transient and permanent impact models is diminished, justifying the continued utility of Almgren-Chriss approximations for day-to-day quoting. The need for transient impact calibration primarily arises in risk scenarios involving large, infrequent flows, where impact feedback is largest and persistent.

Practical and Theoretical Implications

The findings underscore the importance of including transient impact in market-making and execution algorithms for dealers handling significant inventory shocks. While the Almgren-Chriss permanent impact assumption suffices for passive risk control under routine client flow, optimality under realistic transient impact models drives substantial P&L improvements in stressed inventory regimes. This highlights the imperative for desks to calibrate impact decay rates and integrate inventory- and impact-aware policies for large trades.

On the theoretical side, the results extend HJB-based market-making models by coupling inventory and decaying price impact, bridging internalization (skewing) and externalization (hedging) strategies under a unified control paradigm. The modeling framework supports hybrid and adaptive market making, with potential for future integration with agent-based microstructure models and reinforcement learning approaches for model uncertainty or non-Markovian impact.

Conclusion

This paper offers a precise analytical and numerical study of market making in OTC FX with transient impact, generalizing classical models to account for empirically observed resilience in market impact. The rigorous analysis demonstrates when and how transient effects alter optimal decision boundaries and execution policies, providing actionable insights for both theoretical development and market-practitioner implementation. The approach paves the way for more nuanced risk and impact modeling, especially in institutional trading segments where large, infrequent trades play a critical role in desk performance.