Discrete-time asset price bubbles with short sales prohibitions under model uncertainty

Published 24 Dec 2025 in q-fin.MF | (2512.21115v1)

Abstract: In this study, we investigate asset price bubbles in a discrete-time, discrete-state market under model uncertainty and short sales prohibitions. Building on a new fundamental theorem of asset pricing and a superhedging duality in this setting, we introduce a notion of bubble based on a novel definition of the fundamental price, and analyze their types and characterization. We show that two distinct types of bubbles arise, depending on the maturity structure of the asset. For assets with bounded maturity and no dividend payments, the $G$-supermartingale property of prices provides a necessary and sufficient condition for the existence of bubbles. In contrast, when maturity is unbounded, the infi-supermartingale property yields a necessary condition, while the $G$-supermartingale property remains sufficient. Moreover, there is no bubble under a strengthened no dominance condition. As applications, we examine price bubbles for several standard contingent claims. We show that put-call parity generally fails for fundamental prices, whereas it holds for market prices under no dominance assumption. Furthermore, we establish bounds for the fundamental and market prices of American call options in terms of the corresponding European call prices, adjusted by the associated bubble components.

The paper establishes a novel FTAP under model uncertainty and short sales prohibitions using a G-supermartingale framework to characterize bubble dynamics.

It derives necessary and sufficient conditions for asset price bubbles and provides explicit superhedging duality results in a discrete-time setting.

The study analyzes valuation bounds for forward and option pricing, highlighting how market frictions disrupt classical relationships like put-call parity.

Discrete-Time Asset Price Bubbles under Short Sales and Model Uncertainty

Introduction and Context

The paper "Discrete-time asset price bubbles with short sales prohibitions under model uncertainty" (2512.21115) provides a comprehensive discrete-time, discrete-state analysis of asset price bubbles considering both model uncertainty (Knightian uncertainty) and explicit short-sales prohibitions. The work leverages a generalized (sublinear) expectation framework, extending classical risk-neutral valuation to robust and non-linear settings. The author investigates necessary and sufficient conditions for the presence of bubbles, characterizes their structural properties, and examines the implications for standard contingent claims, including forward contracts and American/European options.

Fundamental Theorem and Superhedging Duality

Central to the analysis is a novel version of the fundamental theorem of asset pricing (FTAP) under both model uncertainty and short sales prohibitions. In this market, the absence of arbitrage is proved to be equivalent to the requirement that the discounted asset wealth process is a G-supermartingale under a suitably defined family of risk-neutral measures. Explicitly, for the family Q of absolutely continuous measures, the FTAP states:

Wt≥Q∈QsupEQ[WT∣Ft], for all t≤T

where Wt represents the discounted portfolio/wealth process. This equivalence forms the backbone for deriving robust super-hedging results: the minimal super-hedging price of a claim is the supremum expectation across all Q∈Q.

Definition and Dynamics of Fundamental Prices and Bubbles

The fundamental value St∗ of an asset is rigorously constructed via the super-replication cost of its future cash flows, leading to:

St∗=Q∈QsupEQ[u=t∑τD^u+X^τI{τ<∞}Ft]

The asset price bubble is defined as the nonnegative difference βt=St−St∗. This conception is robust to both market incompleteness and model ambiguity. Several critical convergence properties and the G-martingale structure of the fundamental wealth process are established; notably, St∗→0 quasi-surely as t→∞, and the bubble process exhibits distinct martingale and supermartingale features depending on the asset’s maturity structure.

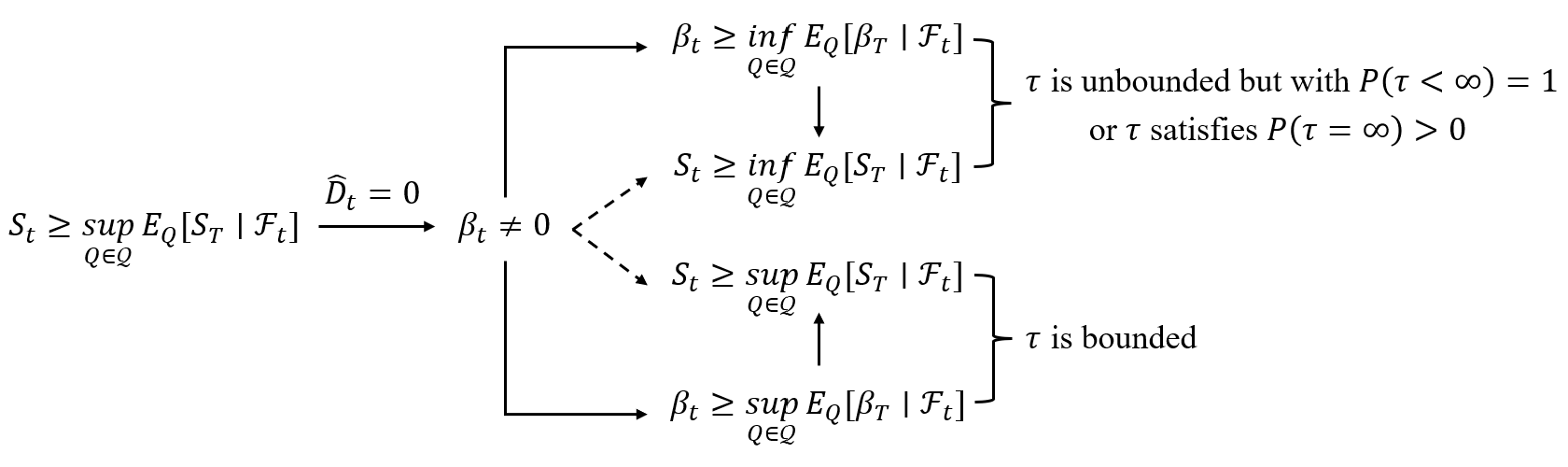

Bubble Types and Characterizations

The paper uncovers two distinct archetypes of price bubbles based on the maturity structure:

G-supermartingale bubbles: For assets with bounded maturity and no dividends, the necessary and sufficient condition for a bubble is that St is a G-supermartingale.

Infi-supermartingale bubbles: With unbounded maturity, the infi-supermartingale property of the market price is necessary, while the G-supermartingale property is sufficient for bubble existence.

Figure 1: The necessary and sufficient conditions for bubbles, distinguishing between G- and infi-supermartingale regimes according to maturity structure and uncertainty.

These characterizations are not just formal: they determine how bubbles may persist, collapse, or re-emerge, underpinning much of the discussion on contingent claims below. In particular, a no dominance condition under model uncertainty is shown to preclude the existence of bubbles altogether, even in the presence of short sales prohibitions.

Contingent Claims: Forward and Option Valuation

The analysis extends to standard contingent claims under the same market frictions and uncertainty. Notably, the constructed fundamental price for forward contracts and European options fails the classical put-call parity:

CtE∗(K)−PtE∗(K)≤Ft∗(K)

where CtE∗,PtE∗ are the fundamental prices for European call and put options, and Ft∗ the forward. This strict inequality arises both from model uncertainty and the presence of short-sales constraints, both of which disrupt the replication strategies needed for put-call parity.

When the no dominance condition is imposed, put-call parity is restored at the level of market prices, underscoring a structural difference between robust hedging cost (fundamental price) and friction-laden asset price.

The relationships among bubble magnitudes for contingent claims are made explicit:

δtS=δtF≤δtEC−δtEP

where δt⋅ denotes the bubble component for the asset, forward, European call, and European put, respectively.

American Option Pricing Bounds

A precise analysis of American call options under the established framework yields bounds relating the American option price to European option prices and bubble magnitudes:

CtE∗(K)≤CtA∗(K)≤CtE∗(K)+δtS

for the fundamental prices, and analogous inequalities for market prices involving bubble terms.

Thus, any premium from early exercise embedded in the American call cannot exceed the bubble size of the underlying asset or the bubble difference between American and European options.

Theoretical and Practical Implications

This framework establishes a comprehensive link between market friction (short sales prohibition), ambiguity aversion (Knightian uncertainty), and asset price bubbles in discrete time/state spaces. It demonstrates:

The robust FTAP and super-hedging duality in presence of realistic market frictions and uncertainty.

Explicit mechanisms by which bubbles can be diagnosed and classified solely from asset price dynamics and their martingale properties with respect to sublinear expectations.

The consistent finding that classical equalities (e.g., put-call parity) fail at the level of fundamental prices but are restored for market prices under no dominance.

Precise upper and lower bounds for American option premiums as a function of bubble components, offering practical guidance for model-based pricing under ambiguity and market constraints.

Future Directions and Conclusion

The theoretical advances here pave the way for practical implementations, such as bubble diagnosis in empirical market data under ambiguity-robust models, and for extensions to continuous time as well as infinite-horizon settings. The interplay between sublinear expectation theory and discrete, frictional markets is shown to yield rich, non-trivial phenomena—notably, the conditions for the emergence, disappearance, and detectability of price bubbles.

In summary, this work advances the mathematical finance literature by rigorously mapping the structure and pricing implications of asset bubbles in markets that reflect both model ambiguity and operational constraints, advancing both theory and the foundations for further empirical and algorithmic investigations.