- The paper demonstrates that a one-standard-deviation increase in closeness centrality boosts the odds of developing new EV competitive advantages by 52%.

- It employs a dual product space network from trade and firm-level data to quantify technological proximity, complexity, and diversification potential in the EV sector.

- Findings imply that regions with established machinery and electronics sectors can strategically leverage their strengths to enhance EV diversification and mitigate supply chain risks.

Product Space Analysis of Regional and Firm-Level Diversification in the Transition to Electric Vehicles

Introduction

The transformation of the automotive industry is determined by intertwined trends: electrification of powertrains, proliferation of software-defined vehicles, and the rise of circular economy principles. These shifts erode traditional sectoral boundaries, with increasing synergies between automotive manufacturing and electronics, battery technology, and software engineering. This paper systematically investigates the potential for regions and firms to develop competitive advantages in the emerging electric vehicle (EV) value chain by leveraging the product space methodology across both trade data and firm-level data, providing novel insights into path dependencies and structural constraints shaping the sector’s global evolution (2512.13178).

Methodological Framework

The study constructs and analyzes high-resolution product spaces from two distinct datasets: the BACI trade database (country-level exports, six-digit HS codes) and the Marklines supplier database (firm-level automotive component manufacturing). These data inform the construction of two product space networks: (1) an industry-level network quantifying co-export patterns across all traded products and (2) a firm-level network describing co-manufacturing of 900+ automotive components by 60,000+ firms. Industry-specific nodes in both networks are mapped by their technological specificity: exclusively ICE, exclusively EV, and common components.

Comparative advantage is measured using standardized revealed comparative advantage (sRCA) indices. Two measures of diversification potential are operationalized: the EV-Complexity Potential (EVCP), which incorporates proximity and product complexity, and closeness centrality, which quantifies a country’s access in the product space to EV-specific components. Logistic regression and centrality-based metrics are then used to predict the emergence of new comparative advantages.

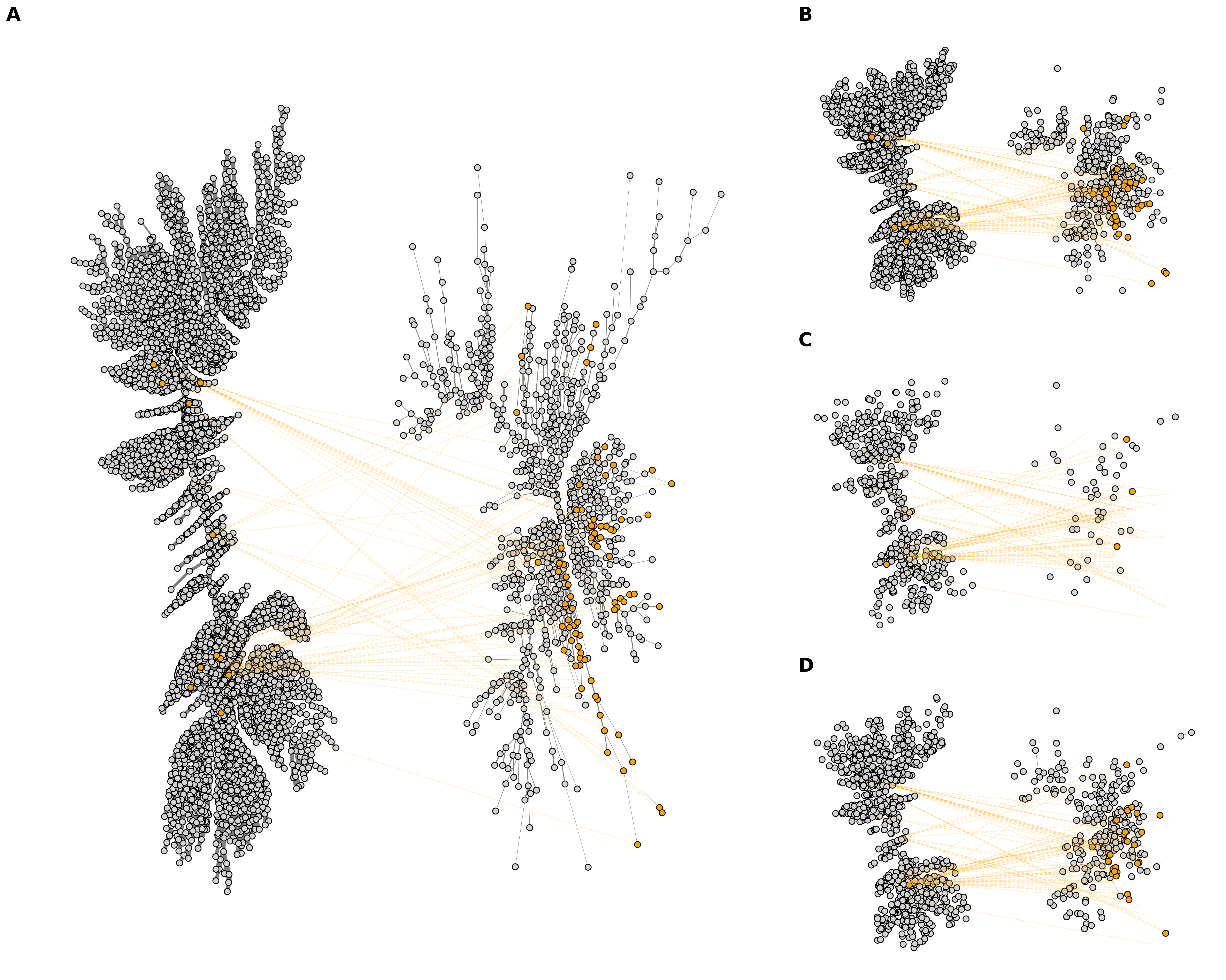

Figure 1: Product spaces constructed from industry- (left) and firm-level (right) data, showing EV-specific nodes (orange) and the relative density and network structure for China, New Zealand, and Hungary.

Path Dependency and Predictors of Diversification

The product space framework validates long-standing principles of relatedness: regions are more likely to develop new export strengths in products proximate to their existing capabilities. Empirical validation via regression demonstrates that closeness centrality is a stronger predictor of future diversification than proximity or complexity measures alone, particularly within the EV sector. A one-standard-deviation increase in country-level closeness to EV products increases the odds of developing new comparative advantages in EV by 52%.

Notably, core product-space sectors—machinery, electrical equipment, and vehicles—consistently exhibit high closeness scores, implying spillover potential. The network structure reveals that diversification pathways are not uniformly accessible; they depend on existing strengths, and centrality is contingent on both sectoral location and regional specialization.

Analysis of export dynamics over time reveals step-change increases in Chinese EV-specific exports—surpassing the EU—and a “hockey stick” in Chinese sRCA for EV products. EU countries, by contrast, demonstrate stagnation or decline in EV-specific sRCA, with comparative disadvantage emerging across a range of EV components.

(Figure 2)

Figure 2: Trends in export value and comparative advantage for EV-specific, unspecific, and ICE-specific HS products across major automotive regions, highlighting heterogeneity and shifts in competitiveness.

At the firm level, advanced manufacturing hubs (Korea, China, US, Canada) and diversified economies exhibit the highest EVCP and closeness centrality to EV technologies. Mapping diversification opportunities reveals that for the EU, new comparative advantage in vehicles, aluminum products, and rubber yields 5x, 4.6x, and 3.7x more incremental EV strengths, respectively, compared to the average EV-relevant sector. In China, with its greater baseline diversification, vehicles yield only a 1.6x increase, underscoring diminishing returns and the role of initial conditions.

(Figure 3)

Figure 3: Closeness gains to EV-specific products by sector and country, showing where comparative advantages translate into strong EV diversification potential.

Supply Chain Risk and Derisking

Import concentration, measured via Herfindahl-Hirschman Index (HHI), is juxtaposed with diversification pathways. In most EU markets, products with higher import concentration (e.g., permanent magnets, batteries) are not proximate to existing comparative advantages, introducing a trade-off between derisking ambitions and feasible growth trajectories within the product space.

(Figure 4)

Figure 4: Correlation of import concentration (HHI) with product space closeness for EV-specific components across EU regions, illuminating structural supply chain vulnerabilities and diversification potential.

Implications and Future Directions

The findings have direct implications for industrial policy, supply chain strategy, and the theoretical modeling of capability formation. Policy interventions will need to account for the differential path dependencies and network centralities revealed—regions lacking centrality to EV components must close capability gaps through targeted investments or risk being marginalized from future automotive growth.

The methodological integration of firm-level and trade data provides resolution to limitations of prior complexity analyses, where sectoral aggregation often occluded cross-industry transformation pathways. Nonetheless, export-based capability proxies remain imperfect, especially in globally fragmented value chains with substantial foreign direct investment and multinational production.

The analysis supports a nuanced diagnosis: regions with well-developed machinery and electronics sectors stand at the nexus of automotive electrification, while established automotive hubs may lose relative advantage without strategic adaptation. New manufacturing centers (Vietnam, Malaysia, Eastern Europe) emerge as potential beneficiaries, reflecting the product space’s predictive power for capability-driven sectoral transition.

Conclusion

This paper advances product-space methodology in modeling the diversification potential of economies and firms during the transition to electric vehicles. Closeness centrality, as a network metric, is demonstrated to be a robust and sectorally discriminative predictor of future competitive advantage in EV technologies. The approach integrates macro- and micro-level data, yields actionable policy insights, and highlights structural challenges in supply chain derisking. Future research should develop dynamic product space models that incorporate policy shocks and endogenous technological innovation, to further elucidate the mechanisms underlying industrial transformation across interconnected global value chains.