- The paper establishes that minimal trading frictions, either through time discretization or instantaneous costs, yield continuous-time equilibria with endogenous boundary block costs.

- It quantifies the convergence rate of discrete Nash equilibria, demonstrating that strategies converge at a 1/N rate and clarifying the universal regularization effect.

- The study shows that omitting instantaneous costs leads to persistent oscillations, emphasizing the critical role of regularization in ensuring well-posed trading models.

High-Frequency Nash Equilibria in Trading Games with Transient Price Impact

Introduction and Motivation

This paper studies the high-frequency limit of Nash equilibria in discrete-time n-player optimal execution games with transient price impact of Obizhaeva–Wang type and instantaneous quadratic trading costs. The canonical setting involves n≥2 agents aiming to liquidate inventories over a finite horizon [0,T], where each trade produces exponentially decaying impact on the asset price, combined with quadratic instantaneous cost penalties. Distinct from earlier two-player studies, this work generalizes results to arbitrary n, provides explicit convergence rates, and tracks the emergence of endogenous boundary block costs in the continuous-time limit. The principal contribution is the rigorous demonstration that both time discretization and small instantaneous trading frictions have a universal regularizing effect, giving rise to the specific boundary frictions required for well-posedness in continuous time.

Discrete-Time Nash Equilibrium: Model and Structure

The discrete-time model considers trading on an equidistant grid TN={0,T/N,2T/N,…,T}, with the price impact kernel G(t)=e−ρt, following the Obizhaeva–Wang framework. Each agent i selects an adapted strategy ξi satisfying deterministic liquidation, facing both the transient impact and quadratic instantaneous cost θ(ΔXt)2. The execution cost functional incorporates impact, instantaneous cost, and a symmetric tie-breaking rule for simultaneous trades.

A Nash equilibrium consists of a deterministic profile (ξ1∗,...,ξn∗) minimizing each player's expected cost against the opponents, and its explicit closed form can be constructed using two fundamental inventory processes v and w. The equilibrium inventories for agent i at time t decompose as

Xt(N),i=xˉVt(N)+(xi−xˉ)Wt(N),xˉ=n1j=1∑nxj ,

where Vt(N) and Wt(N) correspond to symmetric and zero-net-supply cases, respectively.

Continuous-Time Limit and Boundary Block Costs

In continuous time, the optimal execution game with solely transient impact generically admits no Nash equilibrium: Schied et al. (for n=2) and Campbell–Nutz (for general n) established that existence uniquely requires the addition of quadratic boundary block costs at t=0 and t=T, with coefficients ϑ0=(n−1)/2 and ϑT=1/2. The continuous-time Nash strategy for agent i is

$X_t^{*,i} = \mathbbm{g}(t) \bar{x} + \mathbbm{f}(t)(x_i - \bar{x})$

with explicit expressions for $\mathbbm{f}(t)$, $\mathbbm{g}(t)$, and a total cost that decomposes into impact and boundary block cost contributions. The values of ϑ0, ϑT are canonical: any deviation precludes equilibrium for generic inventories (except for the fully symmetric or net-zero initial configurations).

High-Frequency Limit: Rates and Identification of Block Frictions

The main results provide a detailed description of the limiting behavior of the discrete Nash equilibrium as N→∞, specifically:

- Convergence of Strategies: For any fixed θ>0, Xt(N),i→Xt∗,i pointwise on (0,T) with rate $1/N$. The limiting inventory processes universally coincide with the continuous-time limit, independently of the magnitude of θ as long as θ>0.

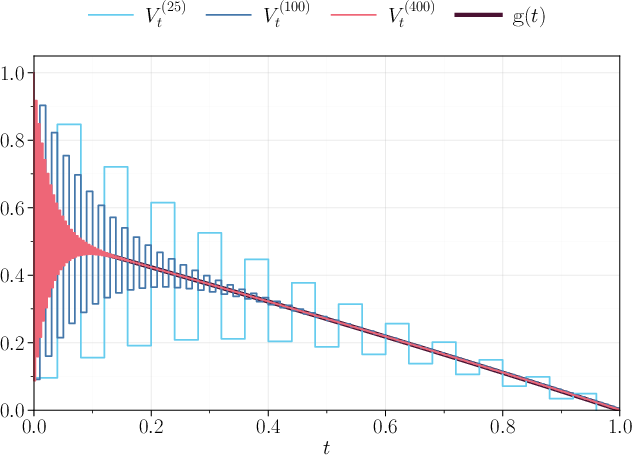

Figure 1: Convergence of Vt(N) as N increases, demonstrating the approach to $\mathbbm{g}(t)$ for n=10, θ=0.1, ρ=1.

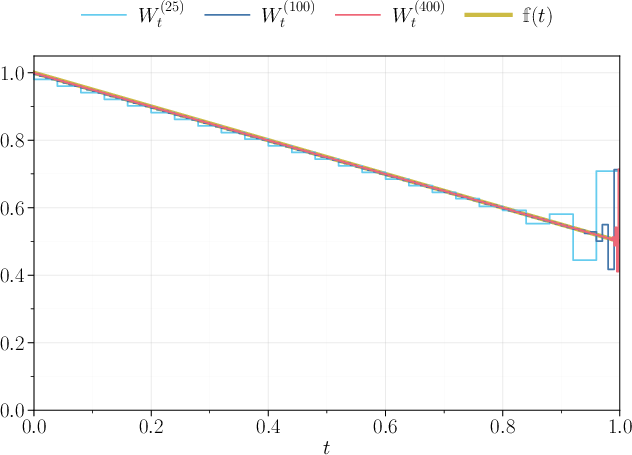

Figure 2: Convergence of Wt(N) as N increases, approaching $\mathbbm{f}(t)$, for the same parameters as Figure 1.

- Emergence of Block Frictions: The initial and terminal block costs of the continuous-time model (ϑ0=2n−1, ϑT=21) are shown to arise as weak limits of the cumulative instantaneous costs accrued in shrinking neighborhoods of the endpoints. The limiting procedure is robust: the result does not depend on the particular choice of θ>0. In the high-frequency limit, the only nonvanishing contribution to instantaneous cost comes from oscillations near the endpoints, whose mass converges to the prescribed block cost.

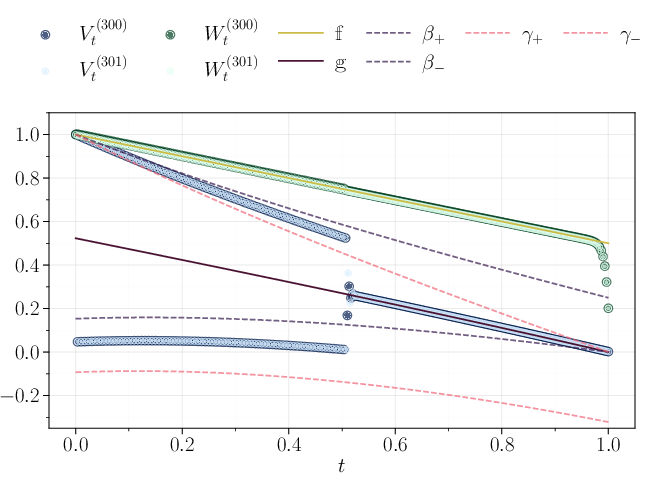

- Impact of Removing Instantaneous Costs: When θ=0, the discrete-time Nash equilibrium oscillates persistently as N→∞. There is no continuous-time equilibrium, mirroring the non-existence results for the unregularized model. Subsequence analysis shows inventories cycling between explicit cluster points, with the partition into even/odd grid sizes controlling the limit.

Figure 3: Oscillatory patterns in discrete inventories under block costs charged only on [T/2,T]; cluster points from the oscillation theorems are indicated.

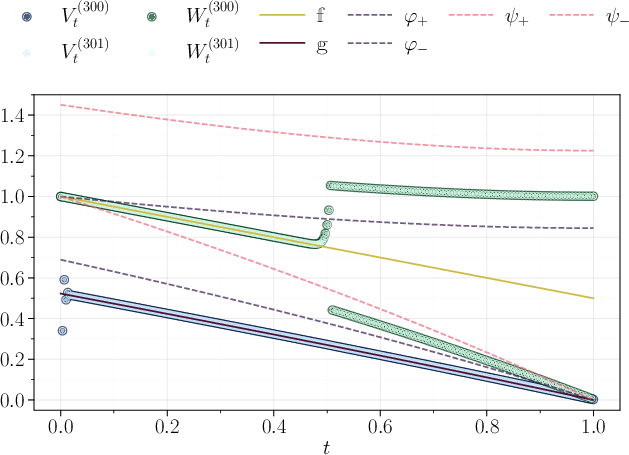

- Boundary Sensitivity: Charging instantaneous cost only on part of the interval (e.g., [0,T/2] or [T/2,T]) allows for convergence to equilibrium only for inventories in symmetric/zero-sum configurations, respectively, matching the existence results for the continuous-time model with only one correct boundary block cost.

Figure 4: Analogous oscillatory behavior when instantaneous cost is charged only on [0,T/2], isolating convergence in the symmetric case.

Numerical and Analytical Consequences

The analysis gives strong, explicit convergence rates for the microscopic-to-macroscopic limit in n-player Nash equilibria, clarifies the exact mechanism by which boundary frictions become endogenous, and displays the universal nature of regularization via either fine time-discretization or explicit instantaneous cost. The precise oscillatory form for θ=0 further sharpens the connection between discrete grid friction and mathematical ill-posedness of pure Obizhaeva–Wang games.

Implications and Theoretical Significance

The findings have several important implications:

- Canonical Regularization: Any positive trading friction (instantaneous cost or positive discretization step) universally selects the same continuous-time model with endogenous block costs, regardless of how small the regularization is.

- Universality: Various trading frictions (small instantaneous penalty, time discretization, or time-inhomogeneous local friction) play interchangeable roles in the existence theory for strategic execution games with transient impact.

- Block Costs Are Endogenous: The required block cost penalties in continuous models should be viewed as emerging features of the market microstructure (tick size, latency, or other "hidden" trading costs).

- Robust Well-posedness: The methods provide a framework for addressing well-posedness and equilibrium computation even in more complex models with signals, non-exponential decay, or other generalizations.

Conclusion

This paper offers a definitive high-frequency analysis of multi-agent optimal execution games with transient price impact. It rigorously establishes the universal appearance of critical block frictions in continuous-time Nash equilibria, derived from both time discretization and vanishing instantaneous costs, and quantifies the resulting Nash strategies and cost convergence. The results provide a comprehensive bridge between microstructure modeling and continuous-time equilibrium theory, with direct relevance for both theoretical mathematical finance and algorithmic market design.

Reference: "High-Frequency Analysis of a Trading Game with Transient Price Impact" (2512.11765)