- The paper introduces Trading GNN that integrates simulated method of moments with GNN techniques to improve asset price estimation in trading networks.

- The methodology leverages message-passing, Nash-bargaining principles, and iterative contraction mappings to achieve convergence and high prediction accuracy.

- Empirical evaluations demonstrate that TGNN outperforms traditional OLS models across various network structures, offering enhanced insights into market dynamics and regulatory effects.

Trading Graph Neural Network

The paper introduces the Trading Graph Neural Network (TGNN), a novel algorithm designed to estimate the impact of asset, dealer, and relationship features on asset prices within trading networks. TGNN strategically integrates the simulated method of moments (SMM) with emerging Graph Neural Network (GNN) technologies, surpassing conventional methods in prediction accuracy and offering adaptable applications across diverse network structures. This essay explores the core aspects of TGNN, elucidating its model, estimation procedures, and empirical evaluations while highlighting its superiority over traditional approaches.

Model and Structure

TGNN is rooted in a parsimonious model representing trading networks as graph structures, where nodes signify dealers and edges represent trading relationships. The model calculates each dealer's value as the difference between its maximum resale price and holding cost, determining potential transaction prices using Nash-bargaining principles. The algorithm ensures the existence and uniqueness of bounded equilibrium solutions through iterative contraction mappings, which are central to simulating and estimating trading dynamics.

Figure 1: The Structure of Dense Random Networks

Estimation With Trading Graph Neural Network

TGNN employs a parameterization strategy to estimate customer values, holding costs, and bargaining power, informed by asset, dealer, and relationship features. The estimation process involves initializing random parameters, computing predicted prices, and minimizing the mean squared error loss between predicted and observed prices using backpropagation until convergence. By leveraging the message-passing framework inherent in GNNs, TGNN facilitates iterative updates to dealer values, achieving an efficient estimation procedure with confidence intervals determined via the bootstrap method.

The algorithm adapts the message-passing principles of GNNs for economic interpretations, structurally embedding economic models into its computations. Unlike generic GNNs, TGNN provides economically grounded interpretations of its parameters, enriching its applicability to financial networks.

TGNN's efficacy is rigorously tested across diverse synthetic network scenarios, including dense random networks, sparse networks, and core-periphery structures, simulating over-the-counter (OTC) markets with varying interdealer relationships. TGNN consistently excels in recovering parameter estimates with high accuracy, outperforming traditional Ordinary Least Squares (OLS) regressions.

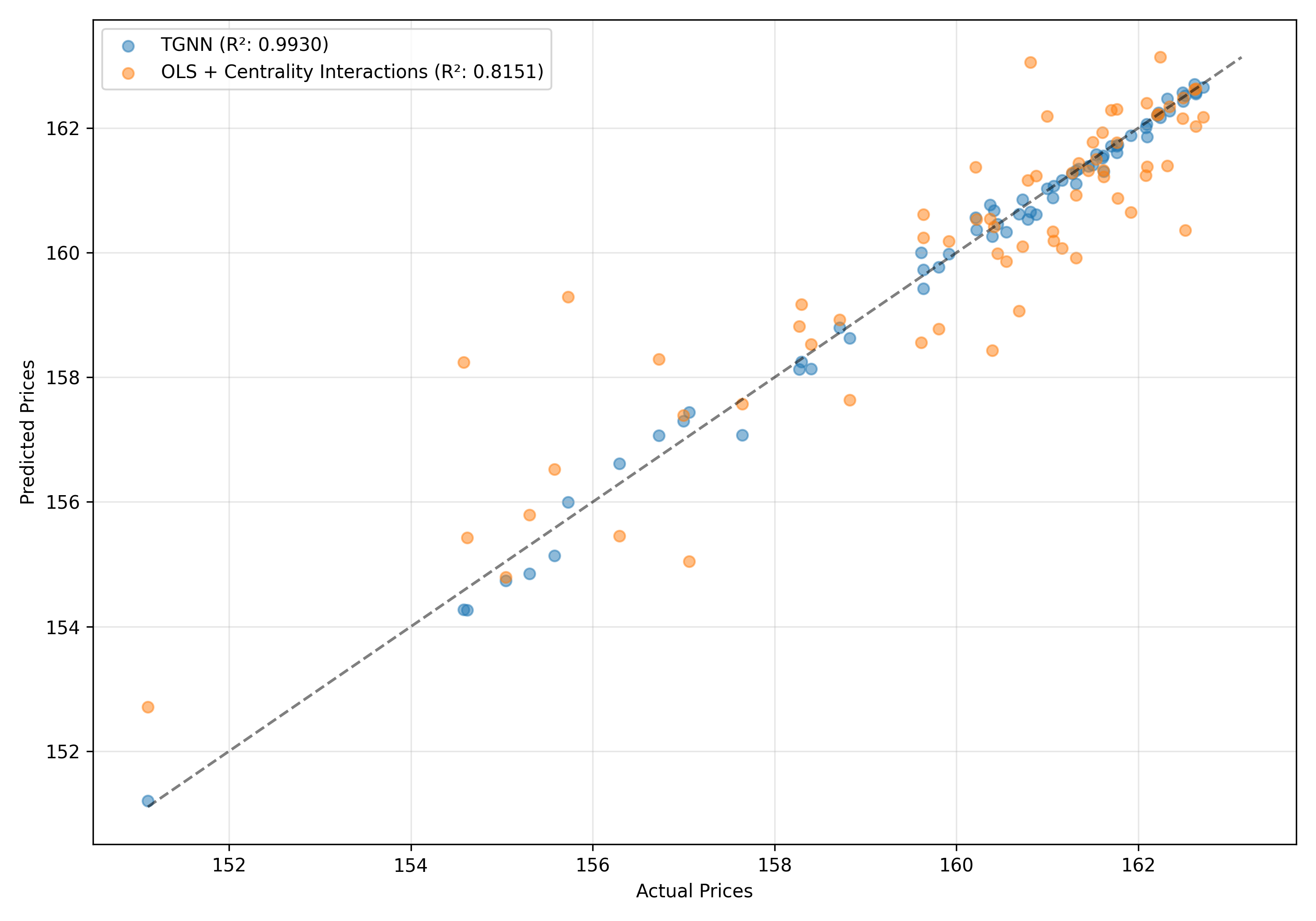

In dense networks, TGNN exhibits extraordinarily high R2 values, significantly reduced Mean Absolute Error (MAE), and Mean Squared Error (MSE), surpassing even the most sophisticated OLS models that incorporate centrality measures and interaction terms.

Figure 2: Prediction Comparison: OLS with Centrality Interactions vs. TGNN in Dense Random Networks

Applications and Implications

TGNN stands as a robust tool for structural estimation in decentralized and OTC markets, offering insights into price formation, market power, and systemic risk while retaining interpretability in its parameter estimates. Its capabilities extend to decentralized digital markets such as cryptocurrency and peer-to-peer lending, positioning TGNN as an invaluable asset for regulatory and efficiency analyses.

The algorithm facilitates counterfactual analysis by simulating market conditions under varied structural changes, such as alterations in dealer inventories or regulatory shifts, thereby informing policy and strategic market interventions.

Conclusion

The Trading Graph Neural Network presents a transformative approach to analyzing trading networks, integrating machine learning advancements with robust economic modeling to facilitate nuanced understanding and estimation of asset prices within complex network structures. Its adaptability across diverse market structures and its high estimation accuracy position TGNN as a preeminent tool in financial econometrics. Through its empirical validation and broad applicability, TGNN not only advances structural estimation methodologies but also aligns theoretical and empirical studies within the finance sector, offering practical insights into market dynamics and potential regulatory impacts.