- The paper introduces MILP and QUBO formulations that address collateral optimization challenges in financial transactions.

- It employs quantum and quantum-inspired methods, using NISQ devices and digital annealers, to solve complex combinatorial problems.

- Numerical experiments explore penalty tuning strategies, highlighting future avenues for enhancing quantum algorithm performance.

Approaching Collateral Optimization for NISQ and Quantum-Inspired Computing

Introduction

The paper "Approaching Collateral Optimization for NISQ and Quantum-Inspired Computing" (2305.16395) addresses the collateral optimization problem (\CO) in financial transactions. Collateral optimization involves allocating financial assets to meet obligations while minimizing costs and efficiently utilizing resources. This process is crucial for mitigating credit risk by ensuring that the value of the collateral offsets the risk of default in lending and derivatives transactions.

The authors approach the \CO~problem by presenting a Mixed Integer Linear Programming (MILP) formulation and a Quadratic Unconstrained Binary Optimization (QUBO) formulation tailored for quantum and hybrid computing solutions. By leveraging near-term quantum technologies, Noisy Intermediate-Scale Quantum (NISQ) devices, and quantum-inspired methods, the paper explores alternate strategies for solving \CO, a challenging combinatorial optimization problem.

Collateral Optimization Problem Overview

In the financial domain, collateral serves as a security against loan defaults, requiring precise and optimal allocation strategies for minimizing costs associated with funding and asset quality. The \CO~problem involves a financial institution managing an asset pool that must be distributed among counterparties to cover exposure requirements while considering constraints like asset limits, risk tiers, and administrative costs.

The problem can be mathematically expressed using MILP, where the objective is to minimize the cost of posting collateral subject to several constraints:

- Quantity constraints ensuring no excessive allocation of a single asset.

- Exposure constraints to meet each account's risk requirements.

- Diversification limits to prevent over-reliance on a single asset type.

Quantum and Quantum-Inspired Approaches

Given the complexity and large scale of \CO~instances, traditional MILP solvers face exponential worst-case complexity. The authors propose QUBO formulations as a promising alternative for harnessing NISQ quantum devices and quantum-inspired hardware. The QUBO formulation is particularly appealing due to its compatibility with various quantum and classical heuristic solvers.

The QUBO formulation of \CO~involves:

- Binarization of decision variables to accommodate quantum and classical solver constraints.

- Recasting linear and inequality constraints using penalty terms and slack variables to fit the QUBO framework.

- Utilizing weighting schemes to balance objective function minimization and constraint satisfaction.

Numerical Experiments

The paper demonstrates the efficacy of the proposed approaches through small-scale simulations using emulators for D-Wave's simulated annealing and Fujitsu’s Digital Annealer. For both balanced and unbalanced penalty approaches, various tuning strategies for Lagrange multipliers were explored to achieve acceptable allocations within the defined constraints.

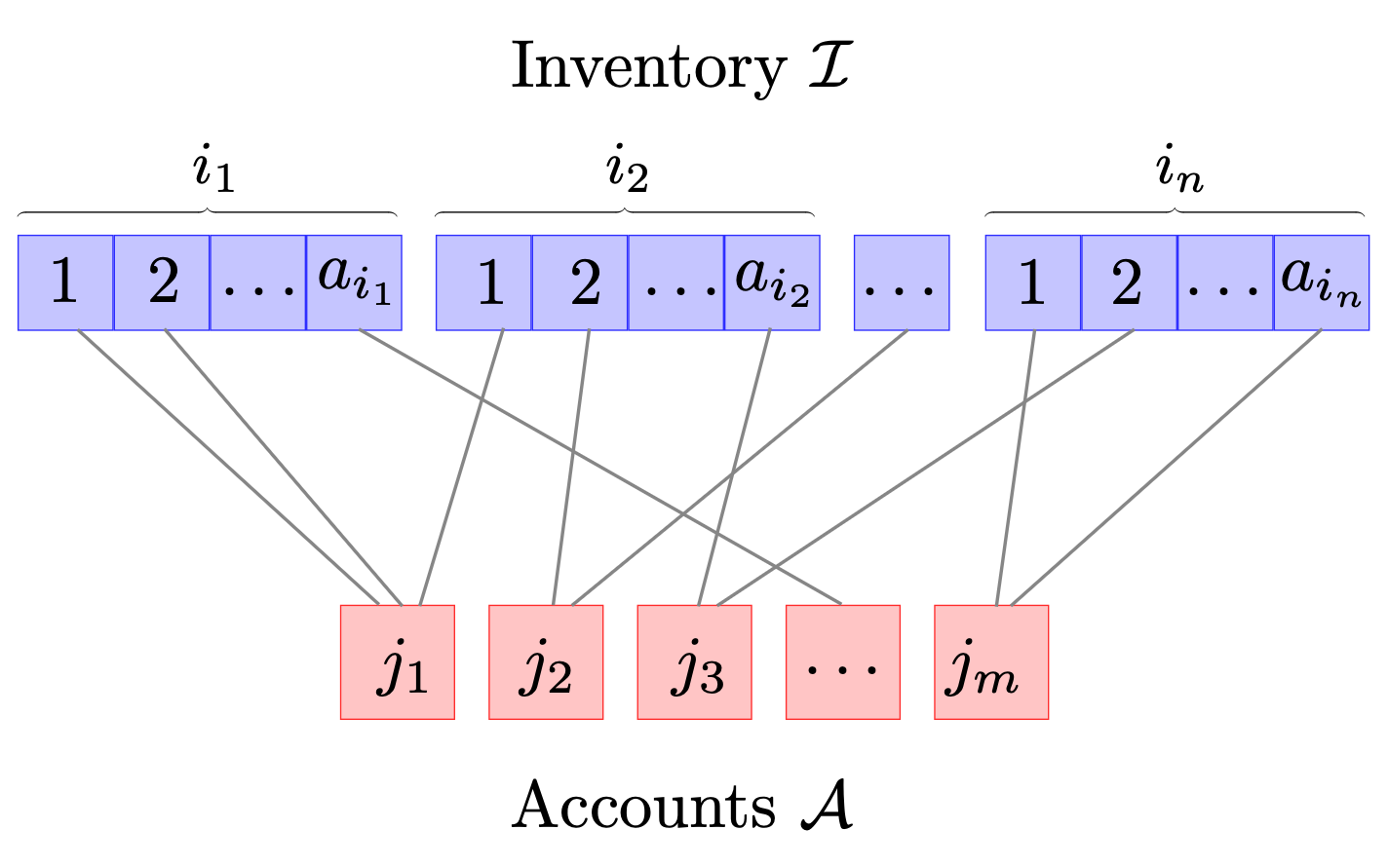

Figure 1: Schematic representation of the collateral optimization problem. The figure above can be seen as a bipartite graph where one has to make optimal allocation of non-unique and weighted pairings.

However, the quantum-inspired solutions did not find the global minimum for the simulated problem instance, indicating room for improvement in formulation accuracy and solver strategies.

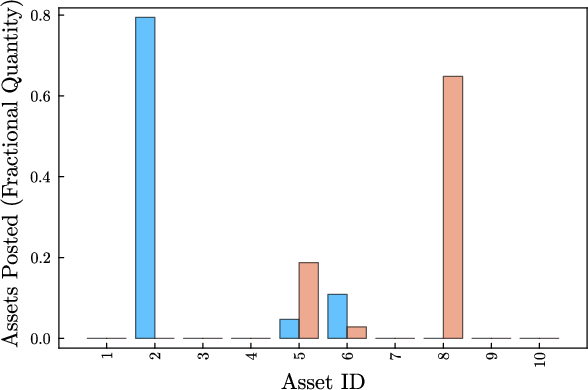

Figure 2: The optimal allocations of assets among accounts with short term (red) and long term (blue) requirements, determined through solving the \CO~ instance as a continuous LP with HiGHS. Assets IDs of 1-4 are low-tier, 5-6 are mid-tier and the final 7-10 are the high-tier assets.

Implications and Future Directions

The exploration of QUBO-based approaches for \CO~sets the stage for potential applications in larger instances enabled by advancements in hybrid and quantum computing. While current hybrid solutions do not surpass classical MILP solvers for small instances, the framework establishes a foundation for automating collateral management processes when quantum hardware capabilities mature.

The study suggests an impetus for further research into:

- Improving tuning methodologies for penalty weights in QUBO formulations.

- Designing novel quantum algorithms and annealing schedules tailored to specific financial optimization problems.

- Benchmarking against established optimization strategies within more extensive and complex problem spaces.

Conclusion

This work underscores the viability and necessity of alternative computational models like NISQ and quantum-inspired computing to address large-scale combinatorial challenges in financial applications. Despite the limitations faced in the current simulations, the research contributes significantly to the nascent domain of quantum finance, promising improved strategies for complex financial operations in anticipation of more robust quantum computing advancements.