- The paper presents a novel Python tool that integrates linear programming for optimal cash management.

- It details both single-objective cost minimization and multiobjective cost-risk models to manage cash flows efficiently.

- The study demonstrates practical applications and sensitivity analyses that support real-world cash management decisions.

PyCaMa: Python for Cash Management

The paper "PyCaMa: Python for cash management" introduces a software tool designed to optimize cash management policies across multiple bank accounts using Python and linear programming techniques. PyCaMa is intended to assist cash managers in making informed decisions by evaluating costs and risks associated with various cash management strategies.

The challenge in cash management lies in balancing cash held versus invested across multiple accounts, ensuring liquidity for obligations while minimizing costs and risks. The paper articulates this complexity by framing it in multi-objective terms: reducing transaction and holding costs, as well as mitigating policy risks.

PyCaMa fills a practical gap in automated decision support tools for cash management. Despite advancements in theory, workable software that practitioners can deploy in real-world scenarios was lacking. PyCaMa leverages Python's accessibility paired with the computational power of the Gurobi solver to implement linear programming solutions. Bank accounts and transactions are modeled via an incidence matrix that forms the basis of optimization problems to determine optimal policies.

Linear Programming Models

Single Objective: Cost Minimization

The single-objective model focuses on minimizing transaction and holding costs over a defined planning horizon:

mint=1∑τ(Γ(xt)+vT⋅b^t)

subject to the continuity constraints and non-negativity of transactions. This approach assumes known cash flow forecasts and utilizes them to predict account balances while minimizing associated costs.

Multiobjective Optimization: Cost and Risk

Expanding to a multiobjective framework, the model introduces Conditional Cost-at-Risk (CCaR) to account for cost variability beyond a specified reference:

min[Cmaxw1t=1∑nc(xt)+Rmaxw2t=1∑nδt+]

Here, w1 and w2 are weights expressing cost-risk preferences. The inclusion of CCaR aligns the solution in assessing the trade-offs between efficiency and exposure to unfavorable cash flow outcomes.

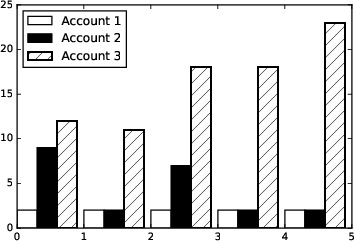

Figure 1: Optimal balances for the cost minimization example.

Software Functionality and Architecture

The PyCaMa package centers around the multibank class, which incorporates instances of cash management systems defined by account and transaction lists, costs, and constraints. Cash managers can input initial balances and cash flow projections to derive cost-efficient transactions.

The software's core functions provide users with the capability to model specific scenarios and explore optimal cash management policies. PyCaMa identifies solutions via linear programming; if a feasible solution exists, it returns the optimal policy and balance schedule over the planning horizon.

Example Application

In the paper, an illustrative example demonstrates PyCaMa's practical application. A model is constructed with three accounts and specific transaction costs. Managers can simulate a five-day outlook using cash flow forecasts and adjust parameters to derive and compare policies contingent on cost versus cost-risk strategies.

Implications for Research and Practice

PyCaMa serves as both a decision-support tool and an academic research facilitator. By addressing multidimensional cash systems, it allows practitioners to validate theoretical concepts against tangible data. Its adaptability makes it conducive to testing different forecasting methods, risk measures, and optimization approaches.

Furthermore, PyCaMa permits sensitivity analyses; adjusting cost structures or flow assumptions to observe resultant impacts offers valuable insights. This robustness ensures PyCaMa's utility in empirical studies and practical decision frameworks, closing the gap between theoretical advancements and operational implementations.

Conclusions

The development of PyCaMa marks a significant contribution to cash management by bridging the complexity of multiobjective optimization with accessible computational techniques. While the existing implementation is robust, future expansions might include more sophisticated forecasting capabilities and risk measures, enhancing its applicability in diverse financial settings. PyCaMa stands as a promising resource for cash managers striving for optimal balance management and researchers exploring financial decision-making algorithms.