- The paper introduces a novel mathematical framework that formalizes how market models actively shape price dynamics through feedback loops.

- It embeds performative dynamics into market making by integrating inventory strategies and dynamic reservation prices into the stochastic price evolution.

- Simulation results demonstrate that the performative strategies yield higher expected returns and lower inventory risks compared to traditional models.

This essay discusses the research presented in "Performative Market Making" (2508.04344), which introduces a novel mathematical framework that formalizes the concept of performativity in financial markets. The research particularly focuses on how the embedded feedback mechanisms of financial models like market making influence market prices and behaviors, ultimately creating opportunities for systematic trading strategies.

The paper begins by defining performativity in the context of financial markets as the empirical phenomenon where financial models do not merely reflect market activities but actively shape them through feedback loops. Traditionally, these models have operated under the assumption of a distinct separation between market descriptions and model behaviors. The performative framework proposed in this research challenges this separation by integrating model-driven dynamics directly into the stochastic processes that govern price evolution.

The dynamic is modeled as:

ds(t)=(r(t)−ϵs(t))dt+σdW(t)

where r(t) represents the dynamic reference process or the reservation price reflecting the financial model's bias. ϵ controls the intensity of the adjustment, encapsulating the degree of performativity present in the system.

This model creates a closed feedback loop where prices gradually adjust toward the reference value r(t), capturing how market models render themselves prophetic by influencing the very prices they compute.

Application to Market Making

The framework is instantiated in the context of the market making problem, traditionally explored by models like that of Avellaneda and Stoikov (A{additional_guidance}S). The inventory strategy—where the market maker's quotes aim to balance inventory and risk—is embedded within the pricing process itself.

The price dynamics driven by performativity are expressed as:

s(T)=e−ξ(T−t)s(t)−γσ2q⋅Δξ+σ∫tTe−ξ(T−u)dW(u),

where Δξ is a critical term quantifying the performative inventory impact. This formulation explicitly shows how inventory influences price, especially how it introduces deterministic drifts that violate standard martingale properties.

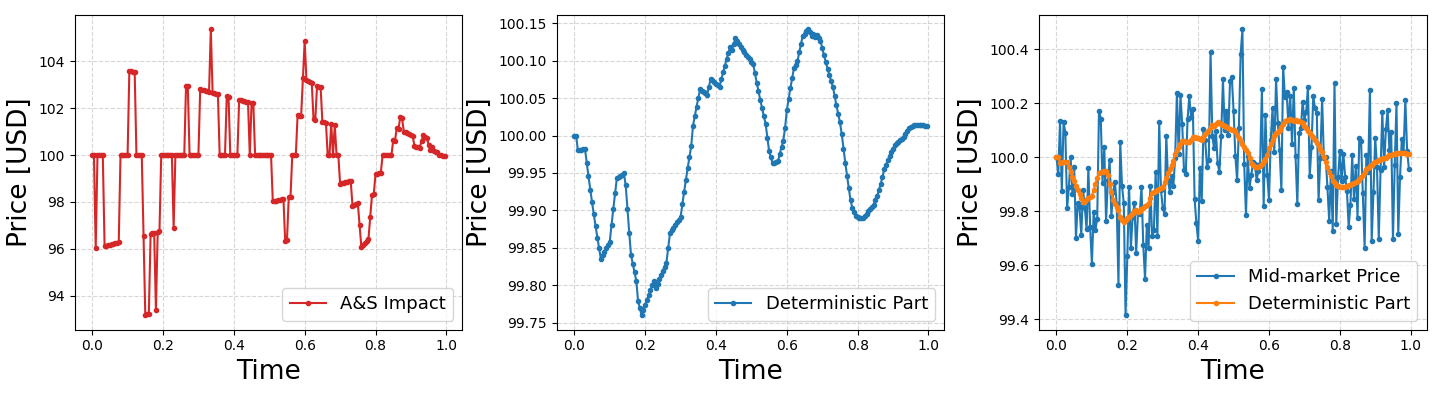

Figure 1: Step-by-step price formation. The three panels show the inventory term adjustment of A{additional_guidance}S (left), the deterministic part of the process, and the final mid-price after the addition of random noise.

The research develops a performative market making strategy that uses the market's inherent performative dynamics to extract arbitrage opportunities. By specifying a reservation price and spread informed by the performative characteristics in equations like:

rperf∗=e−ξ(T−t)s−γσ2(q⋅Δξ+qperf2ξ1−e−2ξ(T−t))

The performative model shows superior profit and loss (P{additional_content}L) profiles across various risk scenarios when compared to non-performative models.

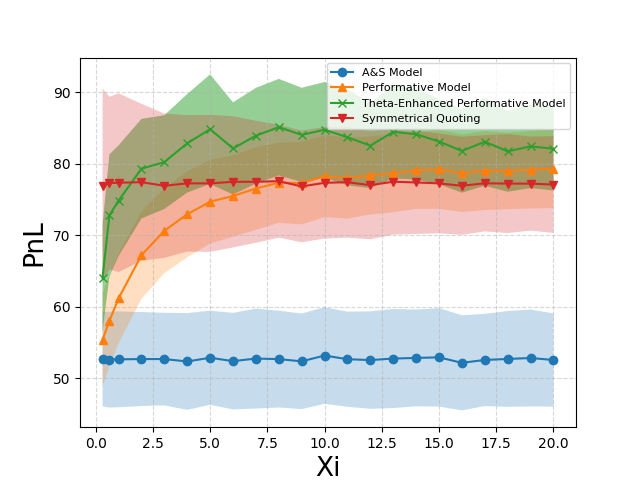

Figure 2: The PnL of all strategies across xi (Xi) values for different gamma values. Performative strategies consistently outperform the A{additional_guidance}S strategy.

Simulation and Results

Simulations confirmed the efficacy of the performative strategies in generating higher expected returns and lower inventory risk. A theta-enhanced variant further optimized the performative strategy by adjusting parameters to maximize utility. Results highlight how incorporating performative elements can systematically improve trading strategies.

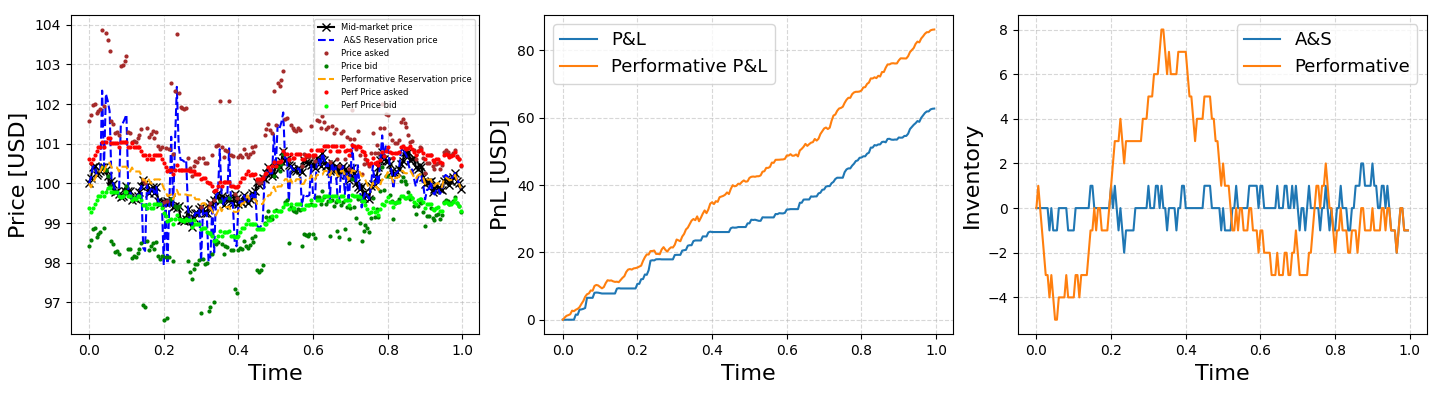

Figure 3: A simulation demonstrating the efficacy of performative strategies over traditional approaches in arbitraging price dynamics.

Conclusion

The paper successfully formalizes the notion of performativity within financial markets, offering a quantitative framework that rigorously models how market strategies don't just respond to market conditions, but help form them. The methods outlined provide a strategic edge in market-making tasks by exploiting the endogenous risks and directional biases that performative strategies necessarily imply. Future exploration in AI and RL settings, where model-based policies are performative themselves, could extend these insights, potentially revolutionizing automated trading systems and high-frequency trading dynamics.