- The paper investigates how predictive volume imbalance informs optimal quoting strategies by solving the market maker’s control problem with HJB equations.

- It demonstrates that risk sensitivity, volatility, and market order intensity significantly influence future price predictions and liquidity management.

- Numerical simulations validate the endogenous link between volume imbalance and price dynamics, guiding optimal tick size and regulatory decisions.

Understanding the Worst-Kept Secret of High-Frequency Trading

Introduction

The paper "Understanding the worst-kept secret of high-frequency trading" (2307.15599) explores the relationship between volume imbalance in a limit order book and future price movements. The authors propose a market-making model where a single market maker, aware of an efficient price, controls the volumes quoted at the best bid and ask prices. By solving this optimization problem, the paper demonstrates the endogenous connection between prices and volume imbalance and confirms that it is optimal to quote a predictive imbalance.

Market Dynamics and Control Problem

The market maker operates in a market characterized by a limit order book, where the mid-price evolves according to an efficient price model with uncertainty zones. The underlying efficient price influences the mid-price dynamics, and the market maker controls the quoted volumes. The study uses Hamilton-Jacobi-Bellman (HJB) equations with nonlocal boundary conditions to solve the market maker's control problem and prove the existence and uniqueness of solutions.

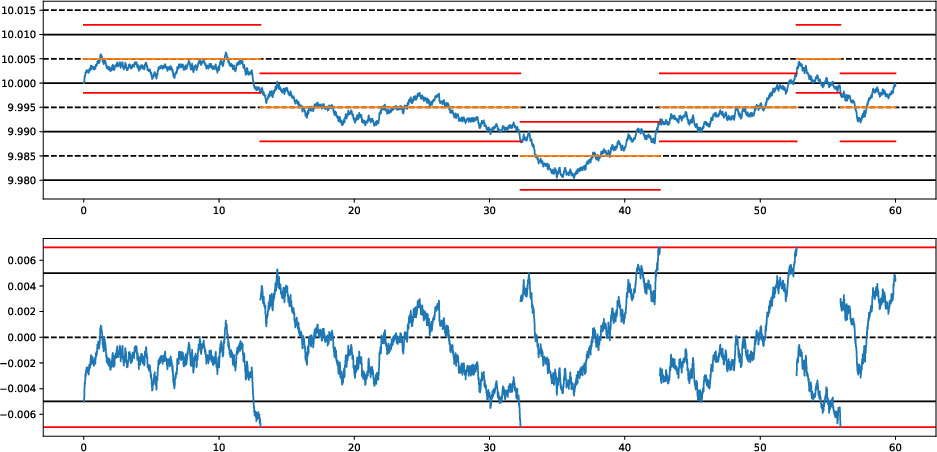

Figure 1: Above: A sample path of S (blue) and P (orange) displaying uncertainty zones in red. Below: Corresponding Y process illustrating the signed distance between the efficient price and the mid-price.

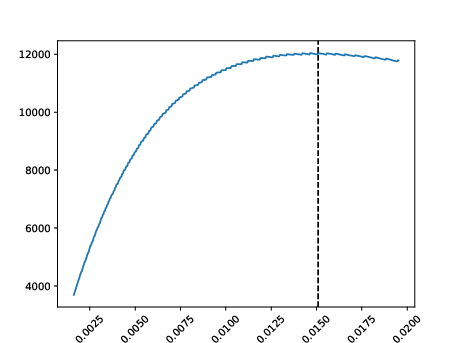

Numerical Results

Through numerical simulations, the paper reveals the predictive nature of volume imbalance concerning price movements. Several parameters, including risk sensitivity, volatility, and market order intensity, affect the market maker's optimal quoting strategy. The paper further discusses the platform's perspective in selecting an optimal tick size to maximize traded volumes, showcasing the impact of different market conditions on liquidity provision.

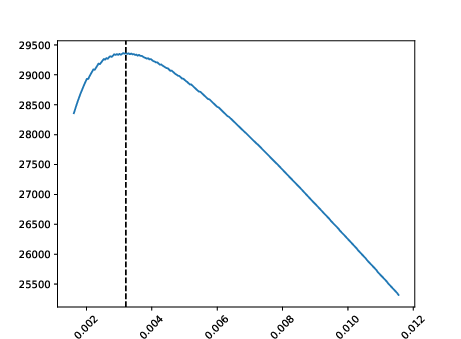

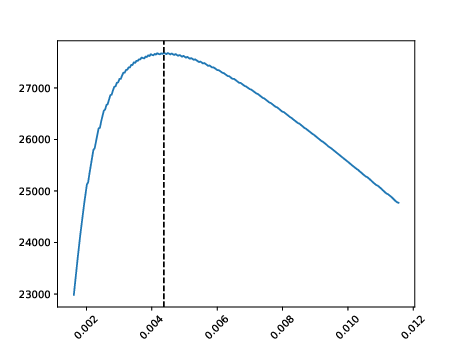

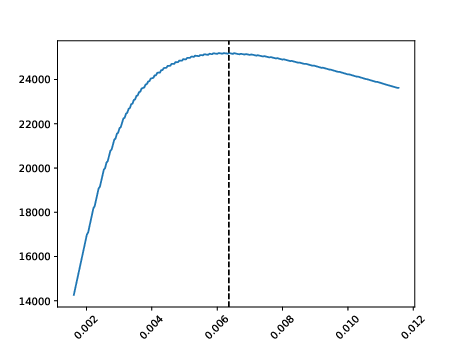

Figure 2: Platform's value function W as a function of tick size, highlighting the optimal tick size selection under various volatility settings.

Implications and Future Developments

The implications of this study are notable for financial regulation, particularly in determining optimal tick sizes for trading platforms. The paper contributes to the broader understanding of market microstructure by elucidating the endogenous mechanisms linking volume imbalance and price dynamics. Future research could extend this framework to multi-agent systems or explore more complex trading environments. Additionally, further investigation into the empirical validation of the proposed model could solidify its practical applications.

Conclusion

The exploration of high-frequency trading through the lens of market-making and volume imbalance provides valuable insights into price prediction and liquidity management. By combining stochastic control theory with comprehensive numerical simulations, the paper advances both theoretical understanding and practical strategies within the field of modern trading platforms.