- The paper introduces NJ-ODE, a framework that integrates jump mechanisms with neural ODEs to yield L2-optimal continuous-time predictions.

- It employs a novel jump neural network for hidden state updates, providing theoretical convergence and reduced complexity.

- Empirical results on financial and real-world datasets confirm NJ-ODE's superior accuracy in modeling irregular stochastic processes.

Neural Jump Ordinary Differential Equations: Consistent Continuous-Time Prediction and Filtering

The paper "Neural Jump Ordinary Differential Equations: Consistent Continuous-Time Prediction and Filtering" introduces the Neural Jump Ordinary Differential Equation (NJ-ODE) framework. This framework extends neural ODEs by incorporating jump mechanisms to model the conditional expectation of stochastic processes with irregular observations. The paper demonstrates the NJ-ODE's theoretical convergence and shows its superior empirical performance compared to existing models like GRU-ODE-Bayes and ODE-RNN.

Model Overview

NJ-ODE combines the strengths of RNNs and neural ODEs to continuously model stochastic processes while accommodating jumps at observation times. Unlike ODE-RNNs, which rely on RNN cells to update hidden states, NJ-ODE employs a simpler approach using a neural network jump mechanism. This choice reduces complexity and allows for theoretical convergence guarantees, emphasizing that NJ-ODE outputs converge to the L2-optimal prediction or conditional expectation.

Implementation Details

Architecture

NJ-ODE consists of several components:

- Neural ODE: Captures continuous latent dynamics between observations.

- Jump Mechanism: Updates hidden states at observation times without relying on prior hidden states, using a standalone neural network.

- Output Mapping: Translates the hidden states to predictions via an output neural network.

1

2

3

4

5

6

7

8

9

|

def NJ_ODE(x, timesteps, model_params):

h_t = initialize_hidden_state(x[0])

predictions = []

for i in range(1, len(timesteps)):

h_t = ODESolve(h_t, timesteps[i-1], timesteps[i], model_params)

if timesteps[i] in observation_times:

h_t = jumpNN(x[timesteps[i]], model_params)

predictions.append(outputNN(h_t, model_params))

return predictions |

Training

Training involves minimizing a novel loss function that balances fitting observed values and maintaining continuity between observations. The convergence guarantees provided by the NJ-ODE's framework are largely due to the precise mathematical formulations and loss function design.

Experimental Results

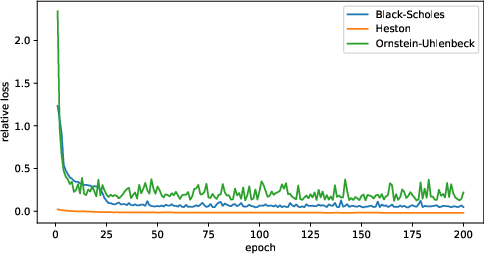

NJ-ODE was tested on synthetic datasets (Black-Scholes, Ornstein-Uhlenbeck, and Heston models) and real-world datasets (such as climate data and physiological recordings). The empirical results show that NJ-ODE consistently outperforms GRU-ODE-Bayes, especially in more complex scenarios like the Heston model.

Figure 1: Predicted and true conditional expectation on a test sample of the Heston dataset.

The NJ-ODE's superior performance is largely attributed to its robust handling of irregular time-series data and its ability to model complex non-linearities present in stochastic processes.

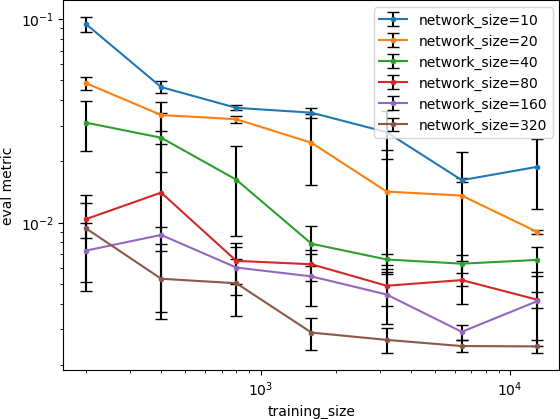

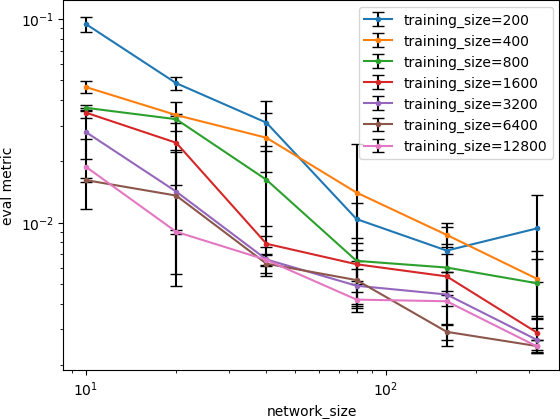

Figure 2: Black-Scholes dataset. Mean ± standard deviation (black bars) of the evaluation metric for varying training samples N1 and network size M.

Implications and Future Work

NJ-ODE offers a robust framework for modeling stochastic processes in finance, healthcare, and climate science. By eschewing the need for continuous information between observations, NJ-ODE makes online updates feasible, which is crucial for real-time applications. Future research could extend NJ-ODEs to capture dependencies across multiple stochastic processes or enhance scalability for large datasets.

Conclusion

The NJ-ODE model represents a significant advancement in continuous-time prediction for irregularly sampled stochastic processes. Its theoretical rigor and empirical success suggest potential for widespread application across fields that rely on time-series data. The integration of jumps into the neural ODE framework addresses a critical gap in continuous-time modeling, facilitating both theoretical developments and practical implementations.