- The paper presents an improved Cuckoo Search algorithm that efficiently calibrates the Heston model for American options by minimizing the sum of squared errors.

- It adapts parameters using a dynamic discovery probability and Lévy flight-inspired random walks to overcome non-convex optimization challenges.

- Experimental validation on synthetic data confirms robust convergence and computational efficiency, highlighting practical applications in derivative pricing.

Robust Calibration of the Heston Model Using an Improved Cuckoo Search Algorithm

Introduction

The pricing of derivative options, particularly American options, poses intricate challenges within financial markets. Traditional models, such as the Black-Scholes model, have limitations, particularly with the assumption of constant volatility which misrepresents real market conditions, such as the volatility smile. Consequently, stochastic volatility models like the Heston model are employed to better align with observed market behavior, as they incorporate time-variant volatility processes. Nonetheless, the calibration of these models for American options is notably complex because it entails estimating multiple parameters without a closed-form solution for American put options.

Problem Overview

Calibrating the Heston model necessitates solving a non-convex optimization problem characterized by multiple local minima. The objective is to minimize the discrepancy between model-predicted prices and observed market prices, represented by the sum of squared errors:

mini=1∑N(Pimodel−Piobs)2

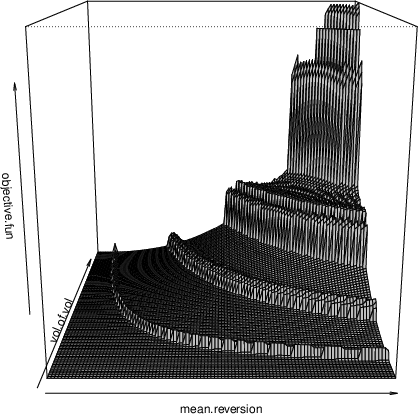

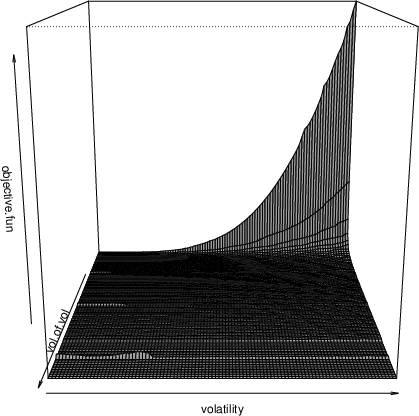

The complexity is compounded by the necessity to concurrently estimate five critical parameters (κ, θ, σ, V0, and ρ) under varying market conditions without the guidance of gradient-based techniques due to the non-convexity. The search space's intricate topography is illustrated in figures delineating parameter variations affecting volatility behavior.

Figure 1: Search space when varying volatility of volatility and rate of mean reversion.

Figure 2: Search space when varying volatility and volatility of volatility.

Cuckoo Search Methodology

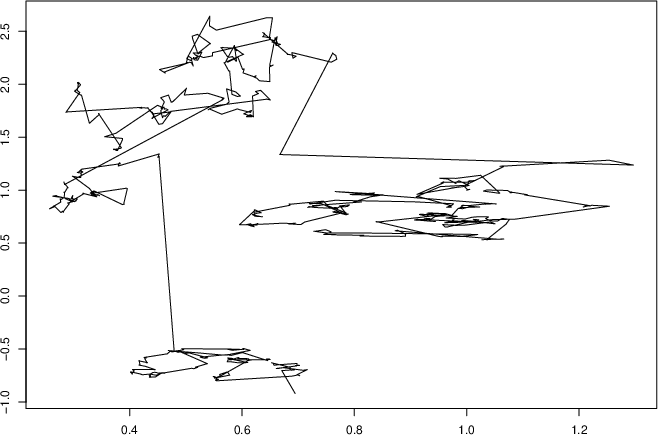

The Cuckoo Search Algorithm, inspired by the brood parasitism of cuckoos, serves as a robust heuristic method for optimization tasks with challenging landscapes. The algorithm operates through laying eggs in nests representing potential solutions, selectively retaining those with optimal fitness, and probabilistically replacing suboptimal nests. This approach exhibits adaptivity through Lévy flight-inspired random walks, enhancing exploration capabilities and precluding entrapment in local minima.

Figure 3: L{évy flight in 2 dimensions with 1000 steps.

Implementation Details

The Heston model’s calibration utilizes an R package implementing an enhanced Cuckoo Search algorithm. Modifications include a dynamic discovery probability (pa), adjusted using a linear decrement strategy to balance exploration with exploitation, optimizing the search trajectory over iteration cycles. Initial parameters and nesting configurations are tailored to ensure computational efficiency and convergence stability across varied financial datasets.

Experimental Validation

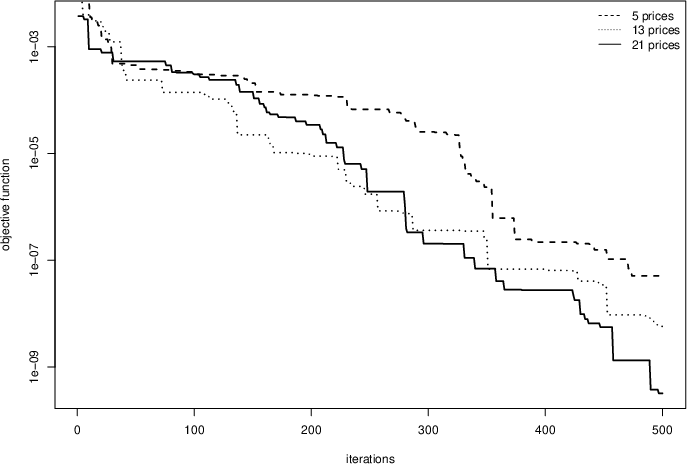

The algorithm’s performance was validated using synthetically generated options data, varying both asset spot and strike prices with consistent maturity periods. Evaluations confirmed robust convergence within the bounds of plausible market parameter sets. The stability of the search strategy is demonstrated across different nest configurations, underscoring computational efficiency without compromising calibration accuracy.

Figure 4: Convergence comparison for different nest sizes.

Figure 5: Convergence comparison for different number of prices.

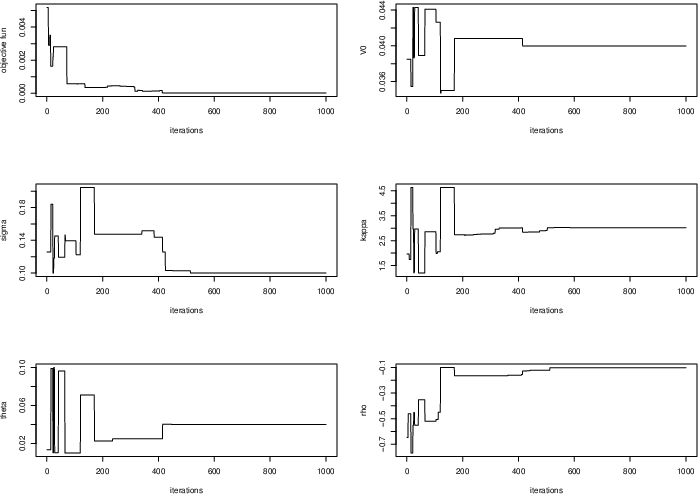

Figure 6: Convergence of objective function and parameters.

Conclusion

Through leveraging the enhanced Cuckoo Search Algorithm, the paper achieves efficient and robust calibration of the Heston option pricing model tailored for American options—overcoming previous limitations. The results facilitate potential extensions into real-world financial datasets, implying substantial practical implications for derivative pricing and risk management strategies in finance. Future work could explore adaptive variants of the algorithm to dynamically respond to evolving market conditions and non-static interest rates.