- The paper presents a novel sigmoid-based parameterization that captures market smiles and skews while ensuring arbitrage-free conditions.

- It employs polynomials of sigmoid functions to fit empirical data and validate the model through numerical experiments compared to traditional models like SVI.

- The model reduces calibration parameters and enables construction of local volatility surfaces for practical option pricing applications.

Sigmoid-Based Functional Description of the Volatility Smile

Introduction

The paper "To sigmoid-based functional description of the volatility smile" (1407.0256) presents a novel approach to modeling the implied volatility surface using a sigmoid-based parameterization. The main aim is to construct an arbitrage-free implied volatility surface capable of accurately fitting market data characterized by volatility smiles and skews. This parameterization leverages polynomials of sigmoid functions alongside other terms to address prevailing deficiencies in existing models.

Theoretical Foundation and Model Structure

The proposed model introduces a static parameterization for the implied volatility surface, designed specifically to ensure flexibility and robustness in capturing market volatilities. Traditional approaches either rely on stochastic models per instrument or employ parametric fits that might only offer a snapshot of the market at a specific time.

Sigmoid Function Utilization

The paper utilizes the properties of sigmoid functions, notable for their bounded behavior and acceleration towards a climax over time, to model the implied volatility surface. Sigmoid functions, exemplified by the ordinary arctangent, hyperbolic tangent, and error function, allow the construction of implied volatility profiles that are continuous and smooth across both call and put wings.

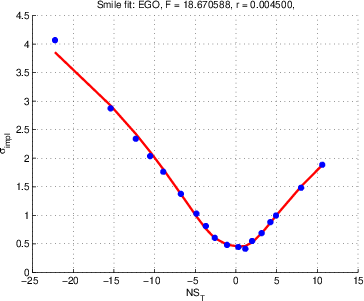

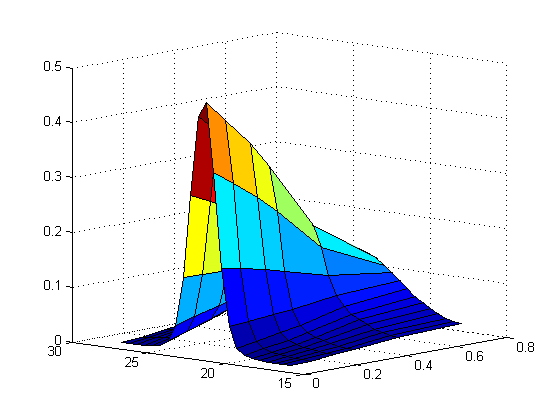

Figure 1: Fitting of the IV smile for EGO, T=10/15/2010.

Parameterization Details

The parameterization reads as a polynomial function in terms of normalized strike z and uses sigmoid forms to address behavior near extreme strikes and expirations. The model parameters include:

- C: Indicating the shift or skew of the smile.

- wC: Denotes the variance at the critical point.

- SC and S: Quantifying skew near the critical point and beyond.

- α and β: Control the steepness of put and call wings, respectively, ensuring correct asymptotic behavior.

- K: Governs kurtosis beyond the critical point.

Comparative Analysis and Numerical Validation

Extensive numerical experiments validate the robustness and adaptability of the proposed sigmoid-based model in fitting empirical market data against known models like SVI and quadratic fits.

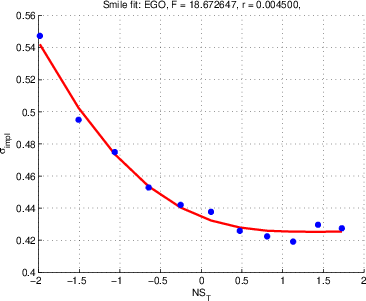

Figure 2: Sensitivity of w_C to the time change.

Term-by-term Calibration

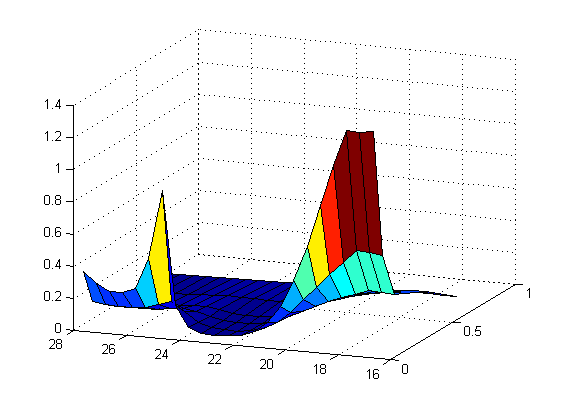

Term-by-term fitting showcases the model's ability to capture both market skews and smiles with a reduced number of parameters compared to traditional approaches. The fitting procedure utilizes the genetic algorithm to solve for the parameters, ensuring that all no-arbitrage constraints are satisfied on the entire computational grid.

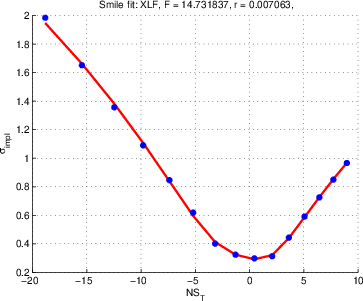

Figure 3: Term-by-term fitting of the IV surface constructed using the whole set of data in Tab.~\ref{TabOpt.

Implications and Future Directions

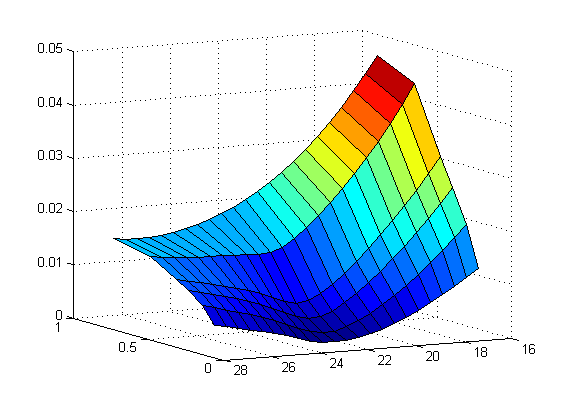

The proposed model paves the way for constructing local volatility and implied density surfaces, fundamental for pricing exotic and vanilla options using local stochastic volatility models. The approach holds promise for practical applications in trading environments, given its parameter robustness over sequential re-calibrations.

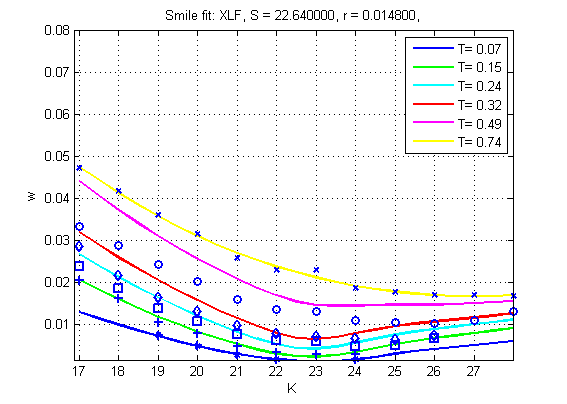

Figure 4: The local volatility surface produced from the IV surface.

Furthermore, its reliance on sigmoid functions suggests potential for adaptation toward dynamic modeling, capturing time evolutions of the volatility surface. Future research may explore integrating business clocks into the time-to-expiration parameter, possibly refining close-to-expiration behaviors.

Conclusion

The sigmoid-based functional description provides a comprehensive and reliable tool for modeling implied volatility surfaces in financial markets. Its capability to fit existing market data while maintaining arbitrage-free conditions positions it as a meaningful advancement in volatility modeling. The framework offers clear theoretical implications and practical utility, encouraging further exploration into its dynamic extensions and integration with broader quantitative finance models.