- The paper introduces a novel approach for detecting and quantifying arbitrage between Ethereum’s centralized (CEX) and decentralized (DEX) exchanges through refined on-chain heuristics.

- The methodology employs price impact analysis to infer searcher revenues and optimize hedging horizons based on observable DEX trades.

- Results reveal market centralization, where three key searchers dominate, raising concerns about Ethereum’s decentralization and network security.

Measuring CEX-DEX Extracted Value and Searcher Profitability: The Darkest of the MEV Dark Forest

Introduction to CEX-DEX Arbitrage

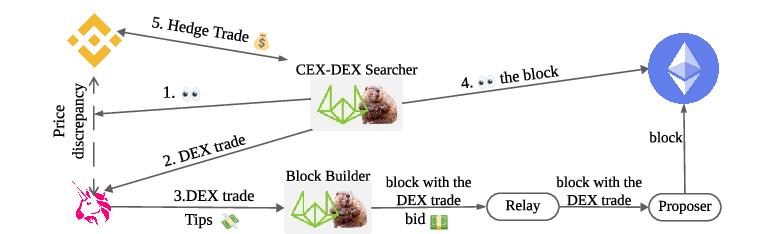

The paper undertakes a rigorous empirical analysis of arbitrage between centralized exchanges (CEX) and decentralized exchanges (DEX) on Ethereum. This trading strategy exploits temporary price discrepancies arising due to structural frictions between high-liquidity, fast-execution CEX platforms and decentralized, slower-settlement DEX venues. These discrepancies offer profitable opportunities for specialized entities known as searchers, who navigate high entry barriers and infrastructure demands to extract significant MEV.

Figure 1: An example of a CEX-DEX arbitrage operation.

Detection and Data Collection Methodology

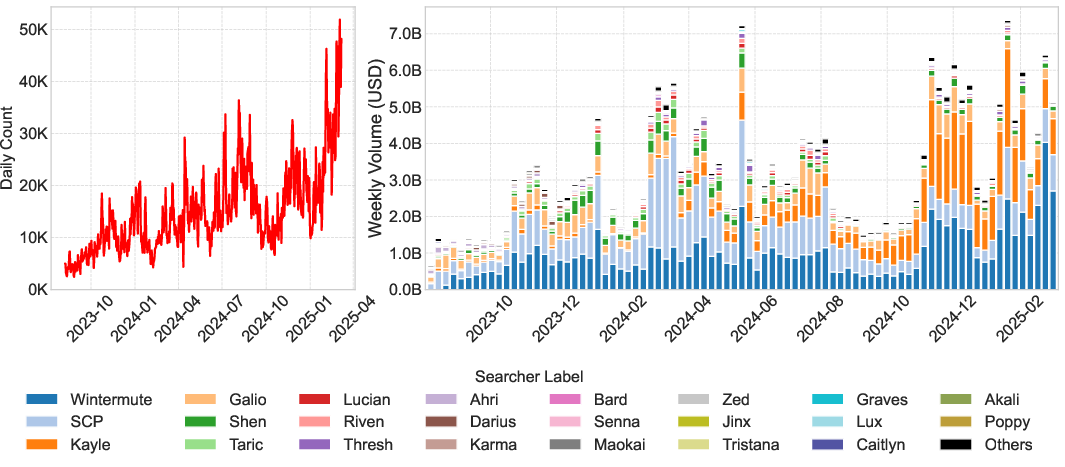

To identify CEX-DEX arbitrage transactions on-chain, the authors refine existing heuristics and expand their coverage. This involves leveraging properties of transactions and behavioral patterns of MEV searchers to infer legitimate CEX-DEX activity. Their dataset spans transactions from August 2023 to March 2025, revealing three major searchers—Wintermute, SCP, and Kayle—dominating the market.

Figure 2: Daily count and weekly volume of detected CEX-DEX trades between August 2023 and March 2025.

Revenue Estimation for Arbitrage Transactions

The study presents a framework for estimating searcher revenues when only the DEX side of arbitrage is observable. By analyzing price impacts in CEX markets, gross returns are calculated over short time intervals to infer optimal hedging horizons for searchers. This method accommodates for variability in searchers' observations and execution times due to differing infrastructure and information asymmetries.

Searcher Profitability and Market Integration

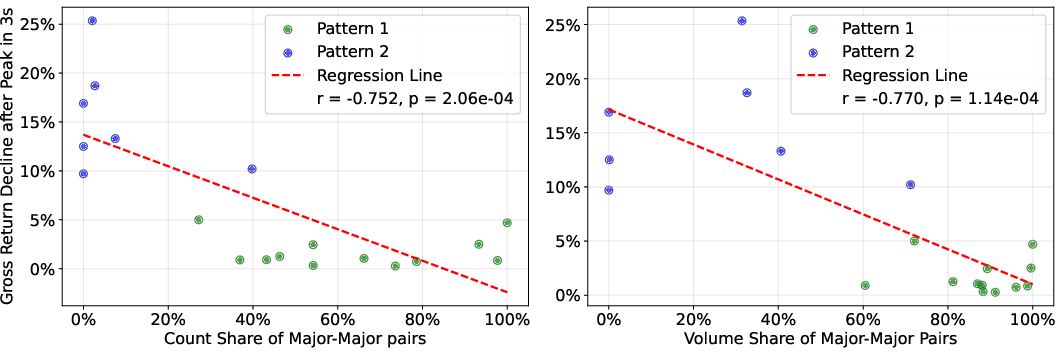

The formal analysis reveals distinct patterns in searcher profitability linked to their integration with block builders. Searchers with exclusive partnerships with builders typically share more revenue, maintaining lower margins than neutral searchers who distribute their order flow across multiple builders.

Figure 3: Correlation between the decline in median gross returns within 3 seconds after peak and the proportion of trade count (left panel) and trade volume (right panel) involving Major-Major token pairs for each searcher. Each scatter represents one searcher, with color indicating their pattern.

Centralization and Its Implications

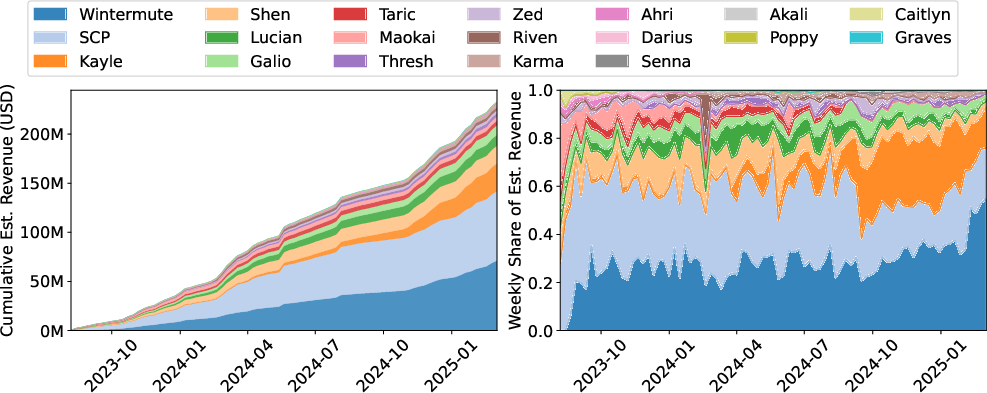

The paper highlights significant market centralization, with three leading searchers responsible for 73% of total extracted value. This centralization poses critical challenges for Ethereum's decentralization and security, as vertically integrated entities dominate both searcher and builder markets. The study provides a nuanced view of market dynamics and the implications of searcher-builder exclusivity on Ethereum's ecosystem.

Figure 4: Cumulative CEX-DEX arbitrage revenue (left panel) and daily share of revenue (right panel) by 19 labeled searchers. A total of 233.8M USD is extracted from 7,203,560 CEX-DEX arbitrages by these 19 searchers between August 8, 2023 and March 8, 2025.

Conclusion

The comprehensive analysis of CEX-DEX arbitrage transactions elucidates complex interactions within the MEV supply chain. By refining detection methodologies and exploring profitability dynamics, the work sheds light on critical aspects of MEV centralization that may inform future decentralization efforts and protocol-level changes to mitigate inherent vulnerabilities and promote a more decentralized Ethereum ecosystem.