Published 11 Jul 2025 in q-fin.PM and cs.LG | (2507.20468v1)

Abstract: The rapid growth of crypto markets has opened new opportunities for investors, but at the same time exposed them to high volatility. To address the challenge of managing dynamic portfolios in such an environment, this paper presents a practical application of a multi-agent system designed to autonomously construct and evaluate crypto-asset allocations. Using data on daily frequencies of the ten most capitalized cryptocurrencies from 2020 to 2025, we compare two automated investment strategies. These are a static equal weighting strategy and a rolling-window optimization strategy, both implemented to maximize the evaluation metrics of the Modern Portfolio Theory (MPT), such as Expected Return, Sharpe and Sortino ratios, while minimizing volatility. Each step of the process is handled by dedicated agents, integrated through a collaborative architecture in Crew AI. The results show that the dynamic optimization strategy achieves significantly better performance in terms of risk-adjusted returns, both in-sample and out-of-sample. This highlights the benefits of adaptive techniques in portfolio management, particularly in volatile markets such as cryptocurrency markets. The following methodology proposed also demonstrates how multi-agent systems can provide scalable, auditable, and flexible solutions in financial automation.

The paper introduces a MAS for crypto portfolio construction that contrasts static equal-weighting with dynamic rolling-window optimization strategies.

It employs Crew AI with eight specialized agents to adjust allocations based on evolving market data, thereby enhancing returns and reducing volatility.

Empirical results demonstrate that the dynamic strategy (Crew B) significantly improves the Sharpe ratio (up to 1.00) and outperforms the static approach in volatile markets.

Agentic AI for Crypto Portfolio Construction

This paper introduces a multi-agent system (MAS) designed for the automated construction and evaluation of crypto-asset portfolios. It compares a static equal weighting strategy against a rolling-window optimization strategy, both aimed at maximizing Modern Portfolio Theory (MPT) metrics such as Expected Return, Sharpe ratio, and Sortino ratio, while minimizing volatility. The system leverages the Crew AI platform, and the empirical analysis is conducted using daily data from 2020 to 2025 on the ten largest cryptocurrencies by market capitalization.

Data and MAS Setup

The study utilizes daily closing prices for the ten largest cryptocurrencies from August 20, 2020, to March 13, 2025. The cryptocurrencies include Bitcoin (BTC), Ethereum (ETH), Binance Coin (BNB), Solana (SOL), Ripple (XRP), Cardano (ADA), Dogecoin (DOGE), Avalanche (AVAX), Polkadot (DOT), and Shiba Inu (SHIB). These assets were selected based on their market relevance and liquidity.

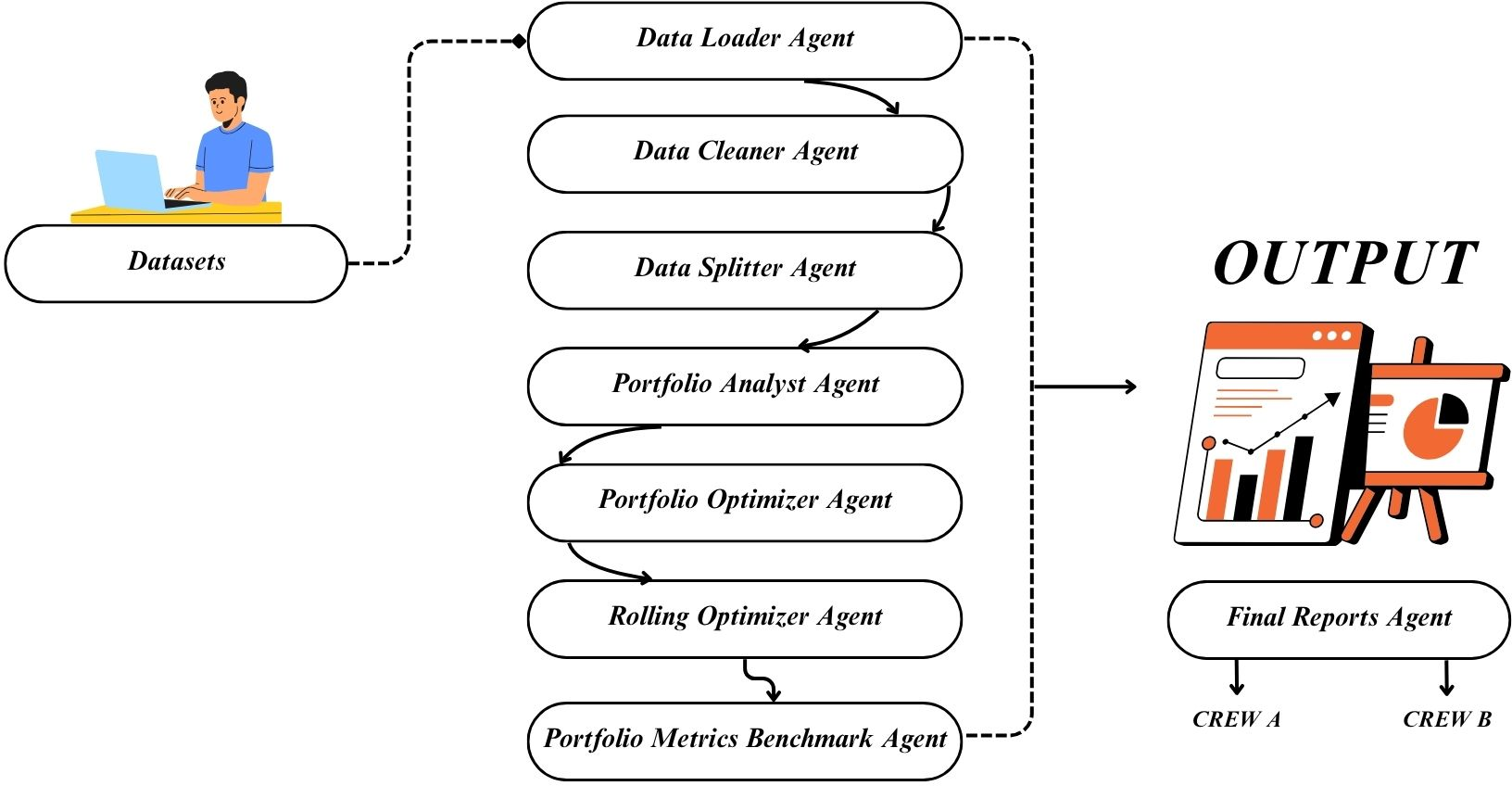

The MAS framework is built using Crew AI, where specialized agents interact to manage the investment pipeline. Each agent is programmed with a specific objective and communicates through structured prompts. The agents utilize tools such as data_loader_tool, data_cleaner_tool, data_splitter_tool, portfolio_metrics_tool, portfolio_optimizer_tool, rolling_portfolio_optimizer_tool, portfolio_metrics_with_benchmark_tool, and file_checker_tool. Eight collaborative agents are organized into two crews with identical structures but different optimization strategies.

Figure 1: The final structure of the Multi-Agent System implemented with Crew AI, illustrating the collaborative interactions between different agents.

Crew A performs a static portfolio analysis, initiating with equal weights and applying a single mean-variance optimization on the training set. Crew B employs a rolling optimization, recomputing weights every 30 days to adapt to changing market conditions. The MAS design emphasizes modularity, replicability, and transparency.

Exploratory Data Analysis

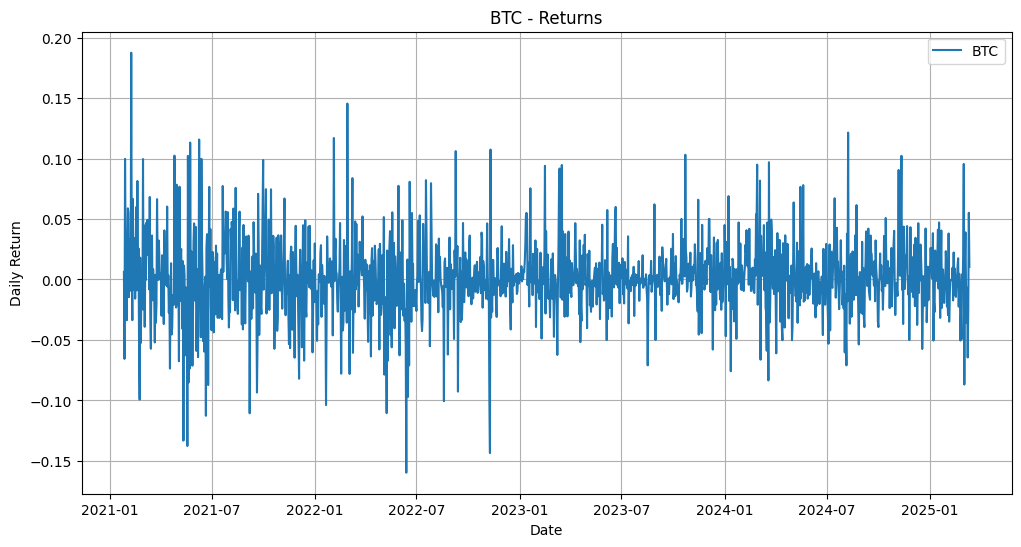

Exploratory data analysis reveals the volatility structure, return distributions, and potential correlations across assets. Bitcoin's (BTC) price trend from 2020–2025 exhibits a strong boom-bust cycle, peaking in November 2021, followed by a correction. The log returns of BTC display volatility clustering, with alternating periods of high and low variance. This analysis suggests the necessity of a dynamic portfolio allocation framework due to significant fluctuations in asset-specific volatility and return behavior.

Figure 2: A visual representation of Bitcoin's close prices from 2020 to 2025, showcasing market volatility.

Portfolio Construction

The paper describes two portfolio management strategies: Crew A (static portfolio analysis) and Crew B (dynamic rolling optimization). Both rely on the same dataset and agent framework but differ in timing, rebalancing logic, and adaptivity.

Crew A: Static Portfolio Analysis

Crew A applies a traditional investment strategy, evaluating an equally weighted portfolio across all ten cryptocurrencies in the training set. It then applies a mean-variance optimization to maximize the Sharpe ratio while minimizing volatility, with constraints of no short-selling and full investment. This strategy does not allow for portfolio rebalancing during the investment horizon. The Sharpe ratio is computed as:

Sharpe=σME[RM]−Rf

where E[RM] is the annualized expected return of the market, and σM represents its annualized standard deviation. The volatility is calculated as:

σM=std(RM)×252

Crew B: Dynamic Rolling Optimization

Crew B incorporates dynamic rebalancing, performing a rolling-window optimization every 30 days to recompute the optimal portfolio weights. This approach reflects adaptive asset management, where allocations are revised based on observed changes in returns, volatility, and correlations. The rolling framework is particularly suited to the crypto environment, where regime shifts and sudden volatility spikes are frequent.

Empirical Results

The empirical results compare in-sample and out-of-sample performance using standard financial metrics. Key metrics include Annualized Expected Return, Annualized Volatility, Sharpe Ratio, Sortino Ratio, and Maximum Drawdown.

In-Sample Performance

Crew A's static optimized portfolio improves over the equal-weighted portfolio, while Crew B significantly enhances the Sharpe ratio while maintaining acceptable volatility. Crew B achieves a Sharpe ratio of 1.00, with reduced volatility (10.2\% against 12.4\%) and improved expected return (9.9\% vs 7.5%).

Out-of-Sample Performance

In the out-of-sample test, Crew A's Sharpe ratio drops to 0.36, whereas Crew B maintains a strong 0.72, demonstrating better generalization. Maximum drawdown is slightly higher for Crew B, reflecting increased exposure to high-return, high-risk assets at certain times.

Comparative Analysis

Crew B consistently outperforms Crew A in the risk-return space, with higher returns and lower volatility. Dynamic rebalancing enables the system to respond to market shifts by allocating weights to outperforming assets and reducing exposure to deteriorating ones. This supports the hypothesis that adaptive strategies perform better in volatile environments like the cryptocurrency market.

Discussion

The findings confirm the importance of adaptivity in crypto-asset allocation. Crew B's rolling framework enhances the in-sample Sharpe ratio from 0.60 to 1.00 and maintains a robust 0.72 out-of-sample, cutting annualized volatility and limiting maximum drawdown. The MAS architecture provides modularity, auditability, and scalability.

The study identifies limitations such as the universe size, transaction costs, window length, and risk metrics. Future research could incorporate stable-coins, regime-switching models, and explainable AI layers to enhance adaptability and investor trust.

Conclusions

The study introduces a MAS for crypto portfolio construction and evaluation. Crew B's dynamic strategy consistently outperforms the static one, validating the benefits of time-varying allocation when regime shifts occur. The MAS architecture proves effective in modularizing and automating the entire pipeline, ensuring transparency, traceability, and replicability. Combining adaptive optimization with modular agent design offers a promising approach for managing crypto portfolios in complex and volatile environments.

“Emergent Mind helps me see which AI papers have caught fire online.”

Philip

Creator, AI Explained on YouTube

Sign up for free to explore the frontiers of research

Discover trending papers, chat with arXiv, and track the latest research shaping the future of science and technology.Discover trending papers, chat with arXiv, and more.