Thermal Macroeconomics: An axiomatic theory of aggregate economic phenomena

Abstract: An axiomatic approach to macroeconomics based on the mathematical structure of thermodynamics is presented. It deduces relations between aggregate properties of an economy, concerning quantities and flows of goods and money, prices and the value of money, without any recourse to microeconomic foundations about the preferences and actions of individual economic agents. The approach has three important payoffs. 1) it provides a new and solid foundation for aspects of standard macroeconomic theory such as the existence of market prices, the value of money, the meaning of inflation, the symmetry and negative-definiteness of the macro-Slutsky matrix, and the Le Chatelier-Samuelson principle, without relying on implausibly strong rationality assumptions over individual microeconomic agents. 2) the approach generates new results, including implications for money flow and trade when two or more economies are put in contact, in terms of new concepts such as economic entropy, economic temperature, goods' values and money capacity. Some of these are related to standard economic concepts (eg marginal utility of money, market prices). Yet our approach derives them at a purely macroeconomic level and gives them a meaning independent of usual restrictions. Others of the concepts, such as economic entropy and temperature, have no direct counterparts in standard economics, but they have important economic interpretations and implications, as aggregate utility and the inverse marginal aggregate utility of money, respectively. 3) this analysis promises to open up new frontiers in macroeconomics by building a bridge to ideas from non-equilibrium thermodynamics. More broadly, we hope that the economic analogue of entropy (governing the possible transitions between states of economic systems) may prove to be as fruitful for the social sciences as entropy has been in the natural sciences.

Paper Prompts

Sign up for free to create and run prompts on this paper using GPT-5.

Top Community Prompts

Knowledge Gaps

Knowledge gaps, limitations, and open questions

Below is a consolidated list of specific gaps and unresolved questions that emerge from the paper and suggest concrete directions for future research.

- Empirical measurement: How can economic entropy and temperature be operationalized and consistently measured in real economies from observable data (prices, quantities, monetary aggregates), including confidence intervals and robustness to data revisions?

- Thermometer design: What concrete protocols, instruments, and data inputs are required to implement the proposed “economic thermometer” for temperature, and how can measurement error and market frictions be accounted for?

- Validation of the second law: Do real-world money flows between economies (countries, regions, sectors) statistically align with predicted entropy-increasing directions and temperature equalization? Design tests using cross-border payments, remittances, and capital flow datasets.

- Timescales to equilibrium: What determines the speed of temperature equalization and entropy change in financially joined economies, and how do transaction costs, capital controls, and network topology slow or prevent equilibration?

- Scope of A0 (unique statistical equilibrium): What micro-level behavioral and market interaction conditions guarantee uniqueness (ergodicity/mixing), and how robust is A0 to herding, coordination failures, or institutional constraints?

- Multiple equilibria and decomposability: How should the framework be extended to systems with persistent segmentation (barriers, islands, submarkets) and multiple stable equilibria; what additional state labels or order structure are needed?

- Path dependence of financial joins: Under what necessary and sufficient conditions is the equilibrium of a financial join independent of how the join is implemented (sequence, channels, frictions), and how large are deviations when independence fails?

- Non-equilibrium TM: How should non-equilibrium thermodynamics concepts (entropy production, flux–force relations) be translated to economics to model cycles, crises, and persistent disequilibria; what are the right macro “currents” and “forces”?

- Production and consumption: How can the axioms and state variables be generalized beyond pure exchange to include production, depreciation, consumption, capital accumulation, inventories, and time-to-build constraints?

- Finance and credit: How to incorporate endogenous money creation, bank balance sheets, credit constraints, leverage, default, and interest rates while maintaining a coherent notion of “conservation of money” and accessible states?

- Multi-currency systems: How to extend the theory to multiple monies with exchange rates, currency substitution, arbitrage, and capital controls; what replaces a single money coordinate and how is “temperature” defined across currencies?

- Pure vs commodity money: How do results change when money has intrinsic utility or storage cost; what are testable implications of the “pure money” construct and how to detect it empirically?

- Goods heterogeneity and indivisibilities: How to relax assumptions of divisibility and indistinguishability to include discrete goods, quality differences, perishability, and non-durables; how does this affect entropy existence and concavity?

- Extensivity and non-extensive systems: Many economies exhibit increasing returns, network effects, and “lumpiness.” What is the appropriate generalization of entropy and temperature in non-extensive settings, and which axioms must be modified?

- Accessibility with realistic constraints: The external trader is assumed to have unlimited goods and money and zero transaction costs. How to model accessibility when the trader is finite, faces constraints, and markets have frictions and legal barriers?

- Concavity/differentiability of entropy: Precisely characterize the conditions under which economic entropy is concave, differentiable, and additive; identify cases where concavity fails (e.g., strong complementarities, externalities) and the implications for stability.

- Uniqueness/normalization of entropy: To what extent is the entropy function unique (up to affine transformations) under the economic axioms, and how should normalization be chosen for empirical comparability across economies?

- Prices and “values”: The paper proposes macro “values” of goods and links to prices and reversible trade. What are necessary and sufficient conditions for market prices to coincide with these values, and how large can deviations be under frictions or market power?

- Cross-derivative relations: Can the predicted symmetry/negative-definiteness (macro Slutsky-like properties) and “flexibilities” be estimated from data, and do they hold across sectors and time? Develop econometric identification strategies.

- Money capacity: How can “money capacity” be defined, measured, and linked to observable aggregates (e.g., money velocity, liquidity ratios)? What determines it structurally, and how do policy levers affect it?

- Reversible trade in practice: With transaction costs and taxes, how close can real trades approach reversibility? Derive bounds on entropy changes under typical frictions and provide empirical tests.

- DSGE and TM integration: What is the mapping between TM’s entropy/temperature and DSGE primitives (preferences, technologies, shocks)? Can TM provide constraints that improve DSGE identification or calibration?

- Welfare interpretation: If entropy is “aggregate utility,” what is its relationship to welfare under heterogeneity and inequality? When (if ever) does entropy increase coincide with Pareto improvements or social welfare gains?

- Inequality and distribution: How do agent-level distributions (wealth, income, preferences) shape macro entropy and temperature; what are the distributional consequences of entropy-increasing transitions?

- Crises and large deviations: How do entropy and temperature behave near abrupt transitions (sudden stops, liquidity crises)? Can TM provide early-warning indicators or bounds on crisis probabilities?

- Calibration and simulations: Beyond the cited simulations, what broader classes of micro models (heterogeneous agents, networked trading, behavioral rules) reproduce TM predictions, and where do they fail?

- Identification from limited data: With incomplete information on quantities and microstates, what minimal datasets are sufficient to identify entropy gradients and temperature differences?

- Policy design: How can fiscal/monetary policies (taxes, subsidies, QE, capital controls) be framed as entropy/temperature interventions, and what constraints does the “second law” impose on feasible policy transitions?

- Exchange rates and inflation: The paper proposes a currency value independent of baskets. How does this relate to CPI-based inflation and purchasing power parity, and can inconsistencies be quantified and exploited for prediction?

- Network structure of contacts: How do money and goods-flow network structures affect equilibria, entropy production, and propagation of shocks; what are the analogues of transport coefficients in networked economies?

- Cyclic money flows: The transitivity of financial equilibrium rules out net cycles in equilibrium. Yet carry trades and global imbalances suggest persistent cycles. Under what conditions does the axiom fail, and how should TM be adapted?

- Robustness to changing technology and preferences: The theory assumes stationary statistical equilibria. How can slow structural change (technology adoption, preference drift) be incorporated as quasi-static processes with trackable entropy?

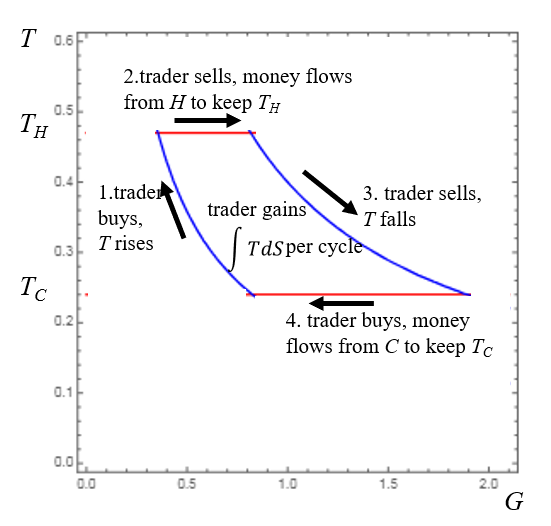

- Testing the Carnot-like cycle: What empirical settings would allow observation or implementation of a Carnot-analogue trading strategy; what are the expected returns net of frictions, and how to isolate temperature-ratio effects from price differentials?

- State-space completeness: What additional state variables (institutions, legal constraints, collateral quality) may be required to ensure that the macro state fully captures constraints on accessibility?

- Micro-to-macro mapping beyond Cobb–Douglas: How do different micro utility forms (CES with low/high elasticity, Leontief, habit formation) aggregate into macro entropy; derive general aggregation theorems and counterexamples.

- Relation to arbitrage conditions: How does no-arbitrage in asset markets interact with temperature equalization and entropy constraints; can TM generate new asset pricing restrictions testable in financial data?

- Treatment of services and intangibles: How should non-storable services and intangible capital be included in the state variables and accessibility framework, and what is their impact on measured temperature?

Collections

Sign up for free to add this paper to one or more collections.