- The paper's main finding is that ChatGPT-3.5 outperforms DeepSeek and traditional methods in predicting stock market returns using good news ratios.

- The methodology employs predictive regression models on WSJ news data from 1996 to 2022, highlighting ChatGPT’s robust contextual analysis for economic forecasting.

- Implications suggest that ChatGPT’s extraction of macroeconomic signals can guide investor strategies by identifying market underreaction to positive news.

Predicting Financial Trends with ChatGPT and DeepSeek

Introduction

The paper "ChatGPT and DeepSeek: Can They Predict the Stock Market and Macroeconomy?" examines the role of LLMs like ChatGPT and DeepSeek in predicting financial outcomes. By extracting information from the Wall Street Journal, the study evaluates the predictive power of these models regarding stock market trends and macroeconomic indicators.

Methodology

The analysis hinges on using LLMs to dissect financial news headlines and alerts, identifying predictive patterns for stock market returns. The primary focus is on two models: ChatGPT-3.5, which exhibits robust English-language capabilities, and DeepSeek, known for its diverse linguistic training, including a strong focus on Chinese.

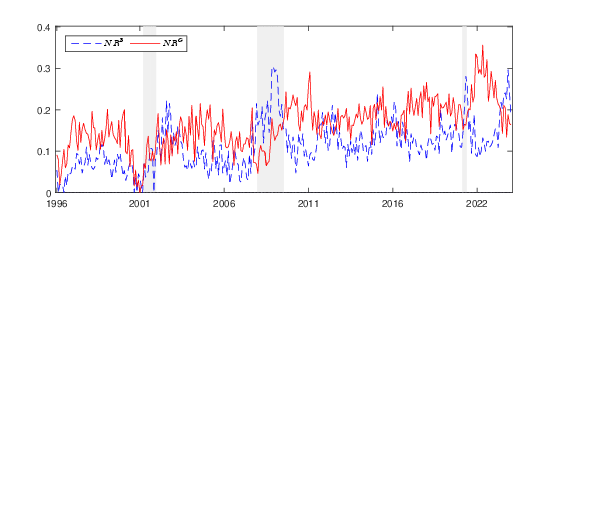

- Data Collection: News data is sourced from the Wall Street Journal, spanning from 1996 to 2022. Headlines and alerts are analyzed using prompts designed to categorize news as indicating potential upward or downward stock movements.

- Model Comparison: The paper compares the effectiveness of ChatGPT and DeepSeek against other LLMs and traditional textual analysis methods (like word lists).

- Predictive Techniques: Employing predictive regression models, the research assesses whether news ratios (proportion of good or bad news per month) are significant predictors of stock market returns or macroeconomic conditions.

Key Findings

Predictive Power of ChatGPT

- Immediate Assimilation: Both good and bad news identified by DeepSeek show rapid incorporation into market prices, indicating a lack of predictive prowess for future returns.

- Sentiment Analysis: DeepSeek's effective capture of investor sentiment reflects its capability to mimic market behavior but lacks depth in predicting long-term economic fundamentals.

Comparison with Traditional Methods

Implications

The differential predictive capabilities of ChatGPT raise important considerations:

- Investor Underreaction: Markets respond to good news identified by ChatGPT more slowly—a phenomenon possibly attributable to investor inattention or ambiguity aversion, aligning with existing behavioral finance theories.

- Market Conditions Insight: ChatGPT's ability to extract and process macroeconomic indicators suggests its utility as a tool for assessing cyclical economic changes and guiding investment strategies.

Conclusion

The exploration confirms ChatGPT-3.5's superior ability in identifying and predicting trends in stock markets and macroeconomic conditions. While DeepSeek competes in sentiment analysis, ChatGPT’s nuanced understanding of economic texts makes it a formidable asset in financial forecasting. Future work could extend this analysis to other financial sectors, enhancing our understanding of LLMs in varied economic contexts.

The study underscores the potential of AI-driven LLMs in revolutionizing market predictability, offering valuable insights for investors and economists striving for refined predictive accuracy in a complex economic landscape.