- The paper presents TradingAgents, a multi-agent LLM system that replicates real trading firms by assigning specialized roles like analysts, researchers, and traders.

- It employs structured communications and agent debates to enhance decision-making and outperform conventional strategies such as Buy-and-Hold, MACD, and SMA.

- Simulations on stocks like Apple demonstrated a minimum cumulative return of 23.21% with improved Sharpe Ratio and robust risk management.

TradingAgents: Multi-Agent LLM Financial Trading Framework

The paper presents the TradingAgents framework as an innovative multi-agent system leveraging LLMs for stock trading, inspired by the collaborative dynamics of real-world trading firms. This framework, incorporating specialized roles such as analysts, researchers, traders, and a risk management team, seeks to replicate the intricate decision-making processes of professional trading environments.

Framework Structure and Agent Roles

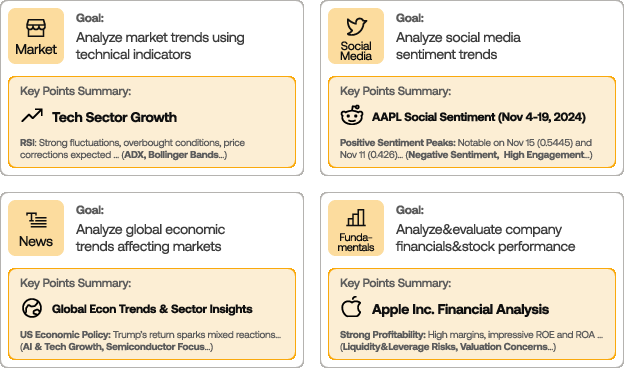

TradingAgents features seven distinct agent roles to emulate the functionalities within a trading firm:

The analyst team's insights anchor the decision-making process by feeding into the Researcher Team, which evaluates the implications through structured evaluations of market data (Figure 1).

Implementation and Communication Protocol

TradingAgents optimizes information flow via structured documents for clear communication between agents, replacing extensive natural language dialogues prone to degradation. This ensures precise decision-making, essential for managing complex trading objectives.

Agents are tasked with specific goals, using a blend of quantitative analysis and qualitative judgment. LLMs handle distinct tasks, choosing between quick-thinking models for basic tasks and deep-thinking models for complex reasoning. This division resembles real-world roles within trading firms, promoting accuracy and efficiency in execution.

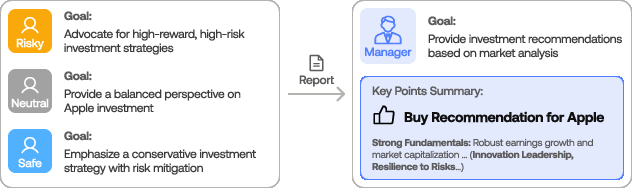

Figure 2: TradingAgents Risk Management Team and Fund Manager Approval Workflow

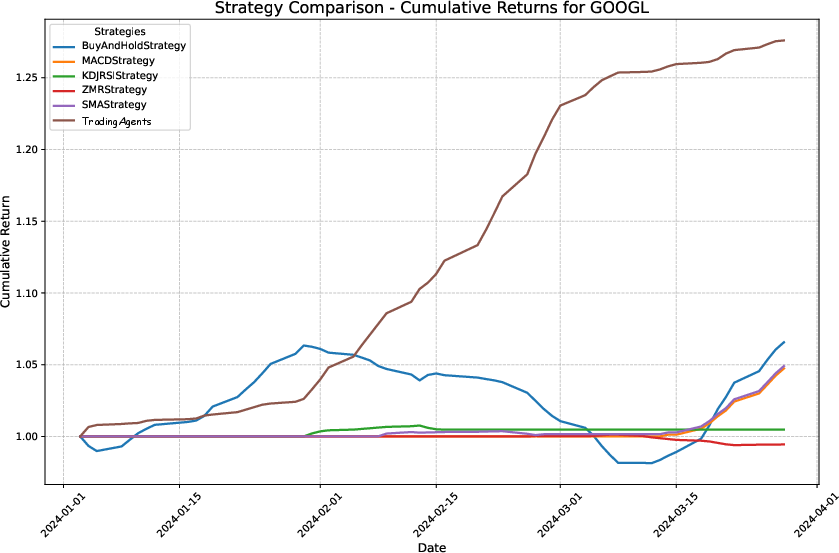

Evaluated through simulations on stocks like Apple, Nvidia, Microsoft, and others, TradingAgents significantly outperforms baseline strategies such as Buy-and-Hold, MACD, and SMA. Key metrics include Cumulative Return (CR), Sharpe Ratio (SR), and Maximum Drawdown (MDD).

TradingAgents achieved a minimum CR of 23.21% across assets, highlighting its ability to capitalize on market opportunities while maintaining manageable risks. The use of structured debate and risk evaluation ensures robust performance under changing market conditions, achieving at least 23.21% CR and a notable Sharpe Ratio improvement (Figure 3).

Figure 3: Cumulative Returns on $AAPL using TradingAgents

Future Developments and Implications

The framework's implications extend beyond trading to any decision-making scenarios replicating dynamic real-world interactions. Future iterations aim for enhanced real-time data integration and expanded agent roles. Possible enhancements include utilizing hybrid communication methods balancing structure with the flexibility of natural language to further refine the decision-making process.

TradingAgents showcases LLMs' potential to transform financial trading, offering insights into the future direction of AI-driven decision systems in high-stakes environments. It suggests a growing role for interdisciplinary AI applications in financial markets, reinforcing the critical impact of collaborative AI strategic models.

Conclusion

TradingAgents presents a comprehensive approach to deploying multi-agent LLM systems in financial trading, replicating the organizational structure of a trading firm. Its agents' structured communication and role specialization underpin its success in simulated environments, outperforming traditional strategies in managing returns and risks effectively. As it becomes more adept at integrating real-time complexity, TradingAgents sets a benchmark for AI frameworks in finance, promising enhanced performance and accountability in decision-making systems.