- The paper demonstrates that atomic execution alone does not guarantee increased arbitrage profits, as it can result in net losses under typical price settings.

- The authors utilize a stochastic model with closed-form profit expressions to rigorously explore the conditions under which atomic execution is beneficial or detrimental.

- The findings imply that additional mechanisms like atomic bridging may be necessary for shared sequencer designs to effectively enhance MEV extraction and cross-rollup liquidity.

Atomic Execution and Arbitrage Profit Extraction in Shared Sequencers

This paper provides a formal analysis of cross-rollup arbitrage in the emerging context of shared sequencers, focusing on the practical question: Is atomic execution alone sufficient to increase arbitrage profitability and, therefore, MEV extraction in rollup-based decentralized finance? The authors present a stochastic model of cross-domain arbitrage between two CPMMs, derive closed-form profit expressions under atomic and non-atomic regimes, and analyze parameter regimes under which atomicity is beneficial or detrimental for arbitrageurs.

Context and Motivation

Decentralized finance on layer-2 rollups has experienced rapid growth, leading to new opportunities and challenges for MEV extraction, particularly arbitrage. Rollup sequencer designs are evolving from independent centralized entities to emerging proposals for shared sequencer networks, which promise enhanced composability across rollups and purportedly offer greater opportunities for cross-rollup MEV extraction via atomic execution and, potentially, atomic bridging.

Atomic execution allows searchers to bundle cross-domain arbitrage trades into a single transaction that is all-or-nothing, mitigating execution risk and currency risk associated with non-atomic arbitrage strategies. However, atomic bridging, which would eliminate the need for liquidity across multiple rollups, is a more complex property requiring additional trust and infrastructural changes.

This paper focuses on atomic execution alone—arguably the most immediate property shared sequencers can provide—and examines whether it suffices to improve arbitrageur incentives, and by extension, rollup/sequencer profitability.

The model assumes two CPMM pools for a token pair (X,Y) in rollups A and B, with respective pool states. An arbitrageur maintains independent liquidity on both rollups, and identifies a cross-rollup price discrepancy (PA>PB). The arbitrage strategy consists of two swaps:

- SB in rollup B: swap Y for X

- SA in rollup A: swap X for Y

The crucial modeling aspect is the introduction of independent random variables FSA, FSB to represent swap failures related to adverse state changes or inclusion risk, with failure probabilities fA and fB. The model omits transaction costs, focusing only on the impact of atomicity.

The profit function under each execution regime is:

- Non-atomic: If either swap succeeds, profit or loss is realized—even if one side fails.

- Atomic: Only if both swaps succeed does the profit accrue; otherwise, both revert.

Optimal trade sizes and profit expressions are derived analytically based on CPMM invariants, fees, trade sizes, and external price reference Pext, resulting in formulas for expected profit difference between regimes.

Parameter Analysis: When is Atomicity Beneficial?

The expected profit difference between atomic and non-atomic execution is:

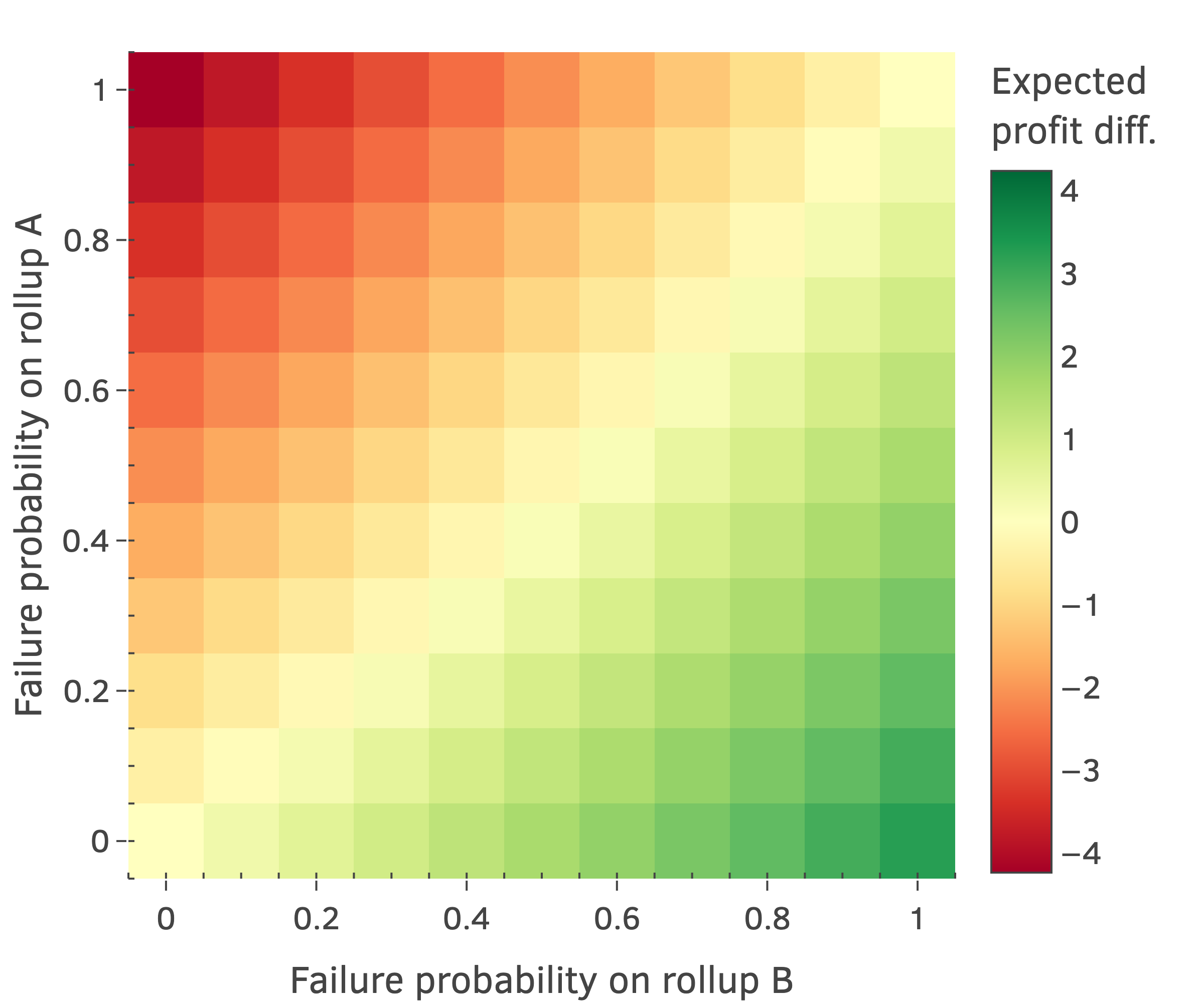

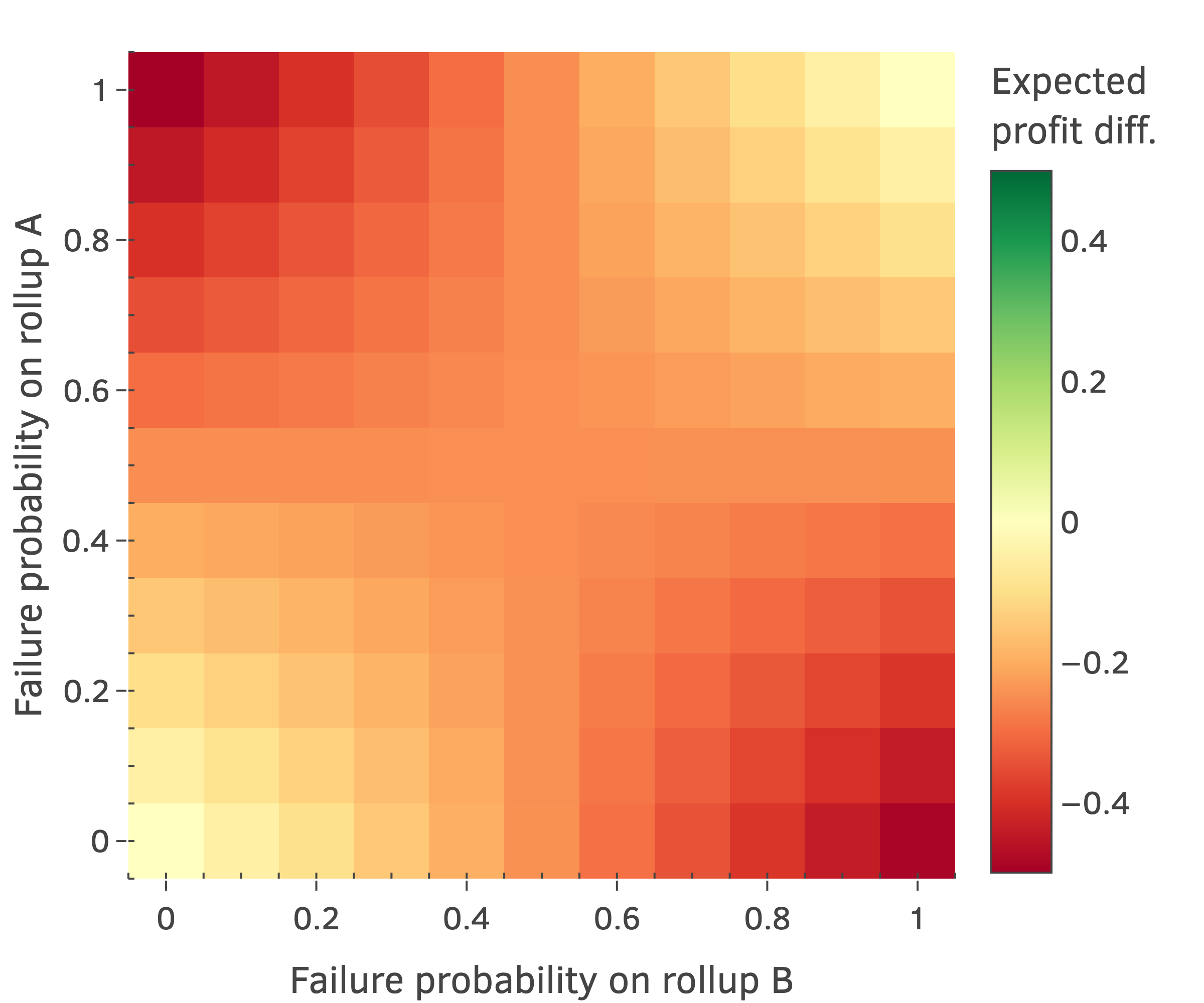

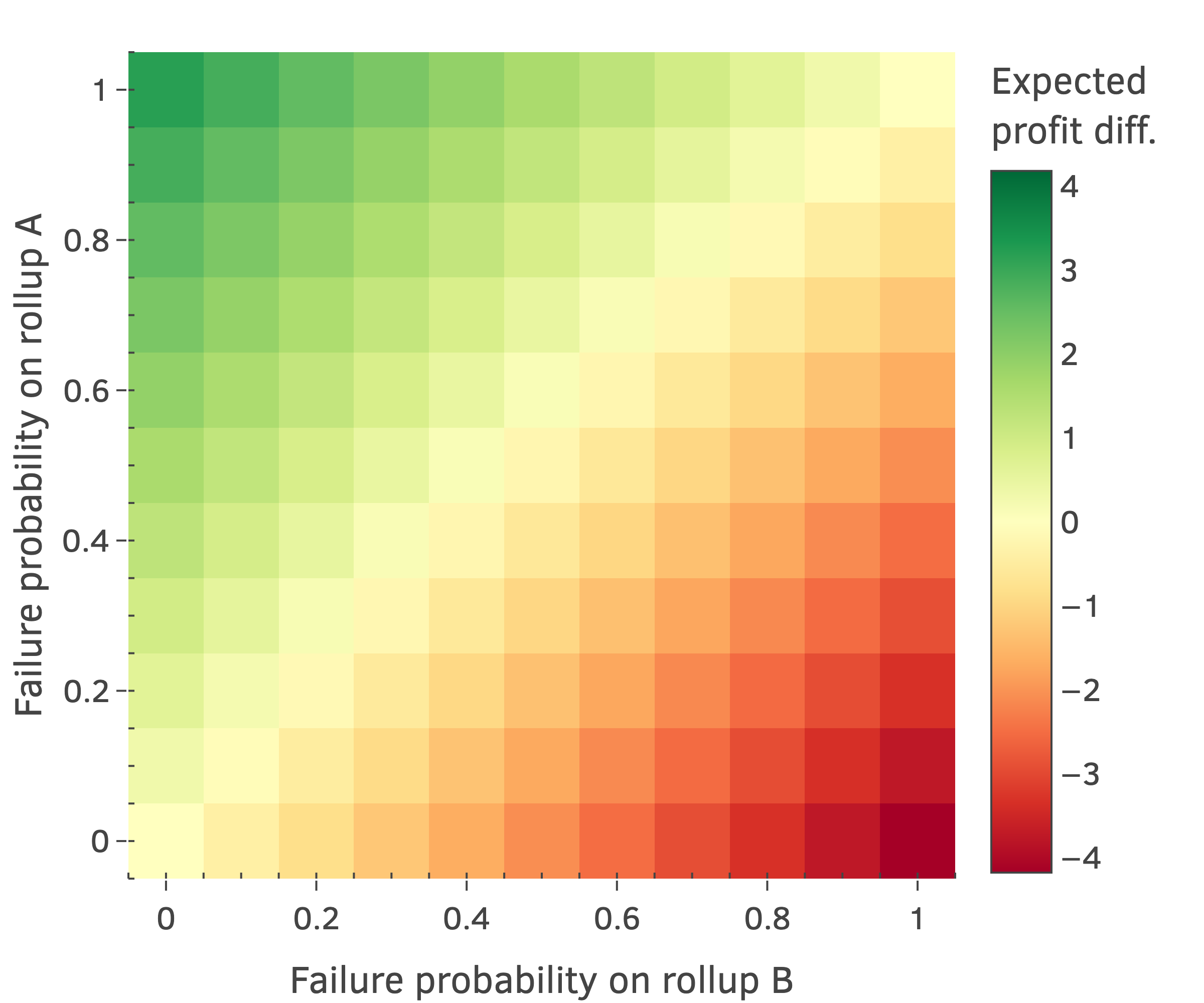

E[Profitdiff]=ΔxB[fA(PB∗−Pext)+fB(Pext−PA∗)+fAfB(PA∗−PB∗)]

where PA∗ and PB∗ are the effective prices paid in the optimal trades.

Key insights:

- The expected profit difference depends on the relative position of Pext to PA∗ and PB∗, the trade sizes, and the respective failure probabilities.

- If Pext is between PA∗ and PB∗, atomicity always makes the arbitrageur strictly worse off—regardless of failure probabilities.

- If failure probabilities are equal (fA=fB), atomicity is always strictly detrimental; i.e., separating swaps probabilistically dominates the atomic approach.

Figure 1: PB∗<PA∗<Pext; Region where the atomic regime is net beneficial or detrimental depending on failure probabilities.

The paper provides analytic and visual exploration of the parameter space, showing that:

- The value of atomicity is highly contextual; positive net expected profit for the atomic regime arises only in pathological settings (e.g., highly asymmetric failure probabilities and specific relative price positions).

- In "middle-price" scenarios, which are likely for pools near reference venues, atomicity is universally detrimental for arbitrageurs.

Implications for Shared Sequencer Adoption and MEV Redistribution

The strongest result is that atomic execution alone is insufficient to guarantee increased arbitrage profitability in cross-rollup settings. This directly challenges the assumption that adding atomicity via shared sequencing will necessarily drive higher MEV extraction and sequencer revenue.

Moreover, in parameter regimes approximating real cross-rollup deployments—such as symmetric or low failure probabilities and external prices between pool effective prices—arbitrageurs are strictly disincentivized to switch to atomic execution. The practical consequence is that developers and rollup operators cannot assume that deploying shared sequencer infrastructure with atomic execution will automatically attract sophisticated arbitrage activity or increase MEV flows.

This also suggests that in the absence of atomic bridging (which remains technically challenging), the rollout of shared sequencers is unlikely to meaningfully alter MEV extraction patterns or cross-domain liquidity dynamics in the short term. These findings are consistent with recent observations that the realized revenue from shared sequencers in cross-rollup arbitrage is not universally higher, and may depend on nuanced incentives, ordering policies, and competition dynamics.

Theoretical and Practical Consequences for Rollup Architecture

The analysis exposes a subtle but critical point in blockchain protocol and DeFi mechanism design: removing execution risk (via atomic execution) is not unconditionally beneficial for arbitrageurs—in some cases, this may paradoxically reduce profits or even lead to net losses.

This has several theoretical ramifications:

- It highlights the non-trivial interaction between risk structure, liquidity provision, and value realization in cross-domain MEV.

- It motivates empirical work to measure the prevalence of parameter regimes where atomicity is net negative, to inform architecture and incentive choices in rollup and sequencer design.

- It suggests that future optimization in cross-rollup MEV extraction will likely require atomic bridging or more sophisticated liquidity management, beyond execution atomicity alone.

On the practical deployment side, protocol designers should be aware that shared sequencer proposals providing only atomic execution may not catalyze the anticipated arbitrage flows or liquidity harmonization across rollups. Careful empirical validation, possibly via simulation or historic transaction data analysis, is required before making infrastructure commitments.

Limitations and Potential Extensions

While the model is robust in its conclusions, some simplifications are noted:

- No accounting for transaction costs or real-world gas fees.

- The liquidity model assumes tokens are held directly, whereas sophisticated searchers often hold stablecoins and actively rebalance.

- The model does not capture competitive latency dynamics, strategic order routing, or asymmetric information.

Future work may address these limitations through:

- Empirical analysis of historic cross-rollup arbitrage and failure rates.

- Extension to the atomic bridging setting to assess the incremental value of that property.

- Integration with auction-based sequencing models to analyze order flow competition and value capture in the MEV supply chain.

Conclusion

This paper rigorously demonstrates that the economic value of atomic execution for cross-rollup arbitrage is highly sensitive to pool parameters, external price references, and failure probabilities. Atomic execution is not a sufficient incentive for arbitrageur participation or increased MEV extraction in shared sequencer architectures. Protocol designers seeking to optimize cross-rollup MEV need to address bridging, latency, and liquidity structures in addition to execution atomism. The paper's results challenge intuitive notions about risk-reduction in arbitrage and will inform both the theoretical modeling of MEV and the practical migration of DeFi ecosystems across rollup architectures.