StockGPT: A GenAI Model for Stock Prediction and Trading

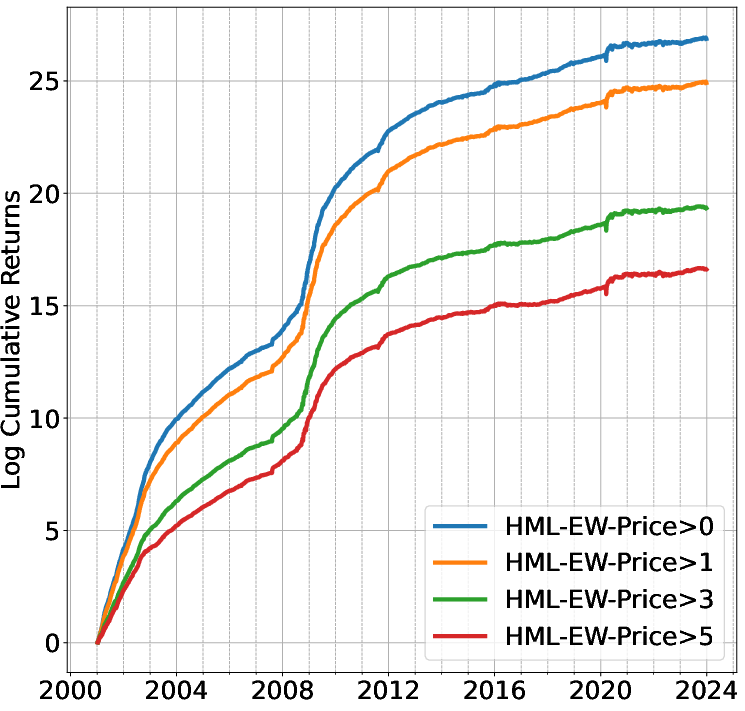

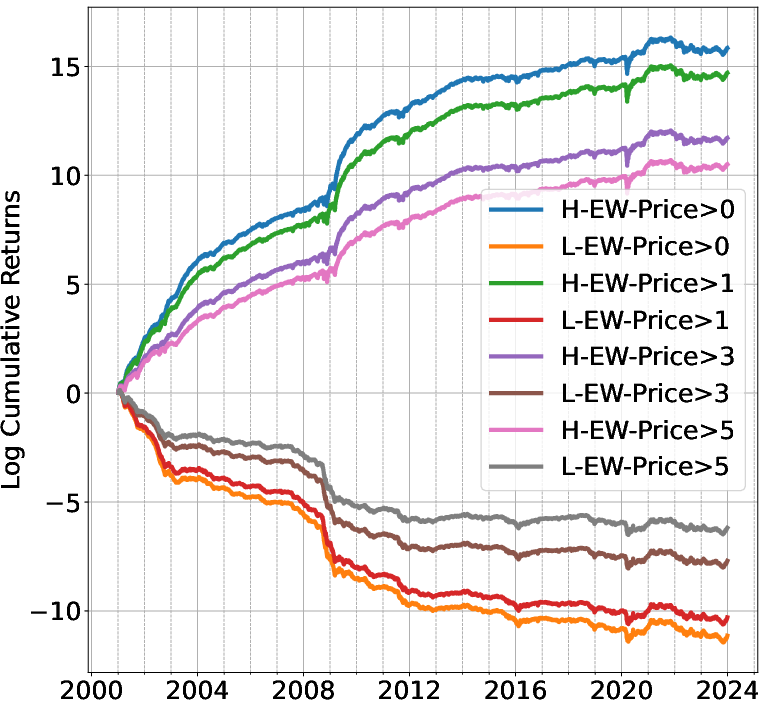

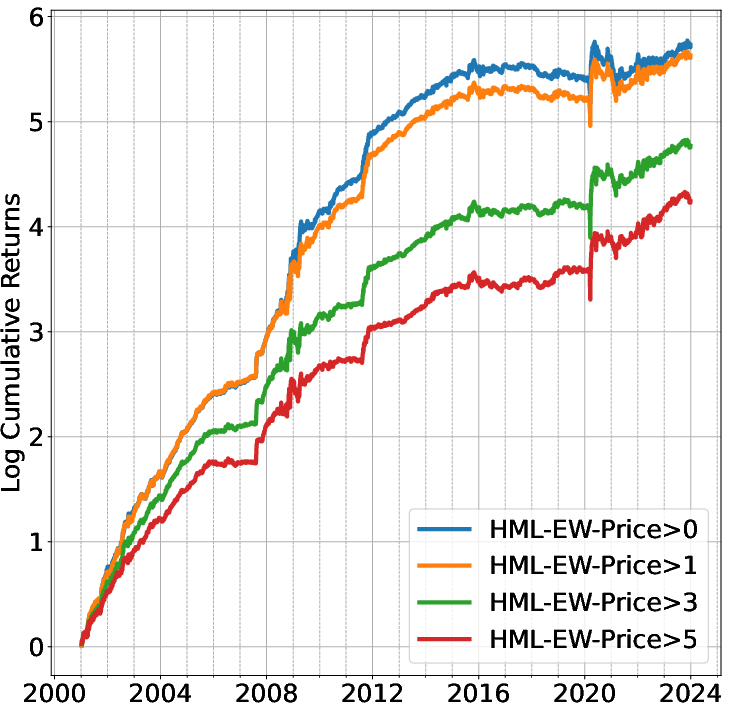

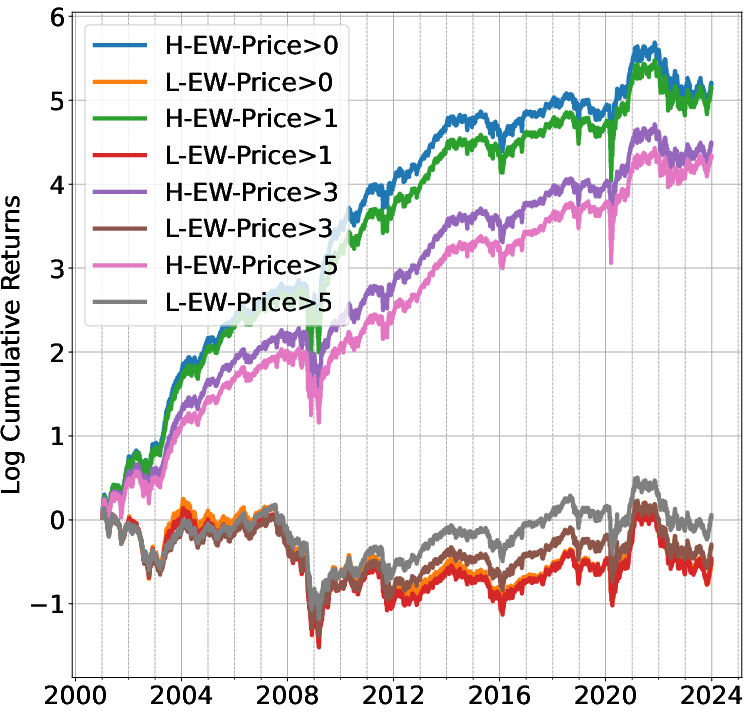

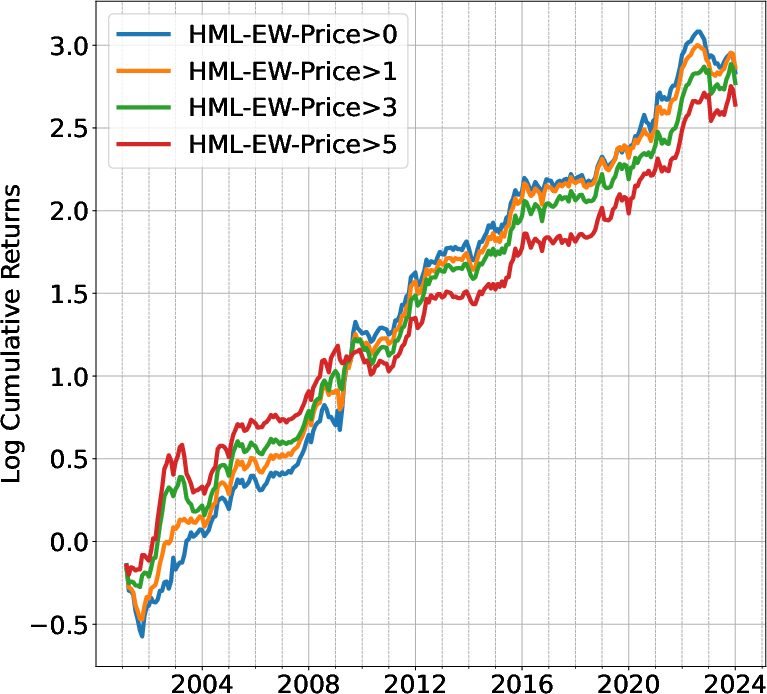

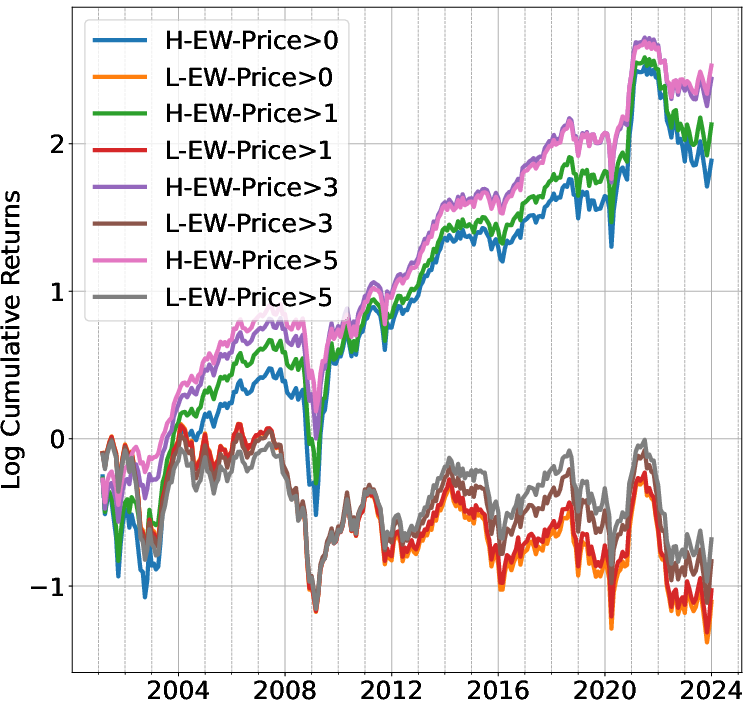

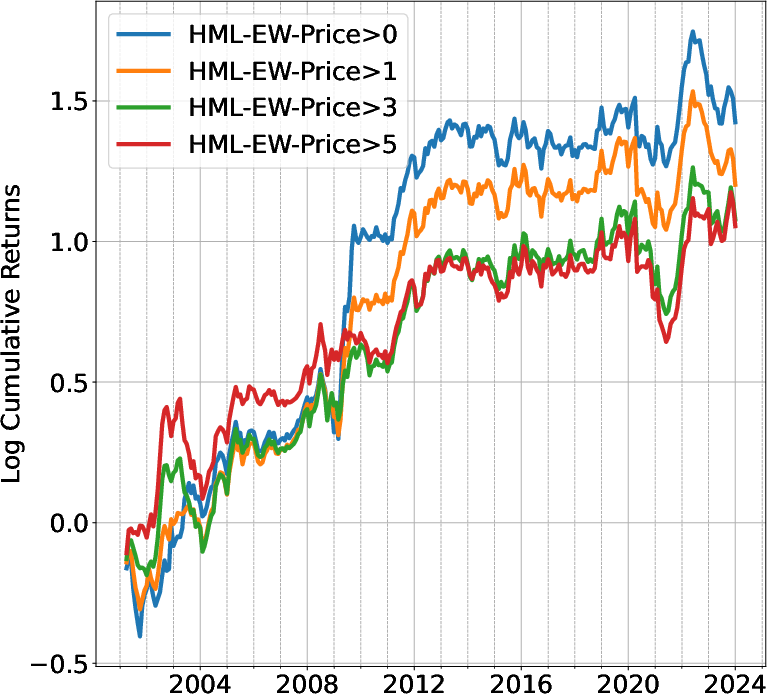

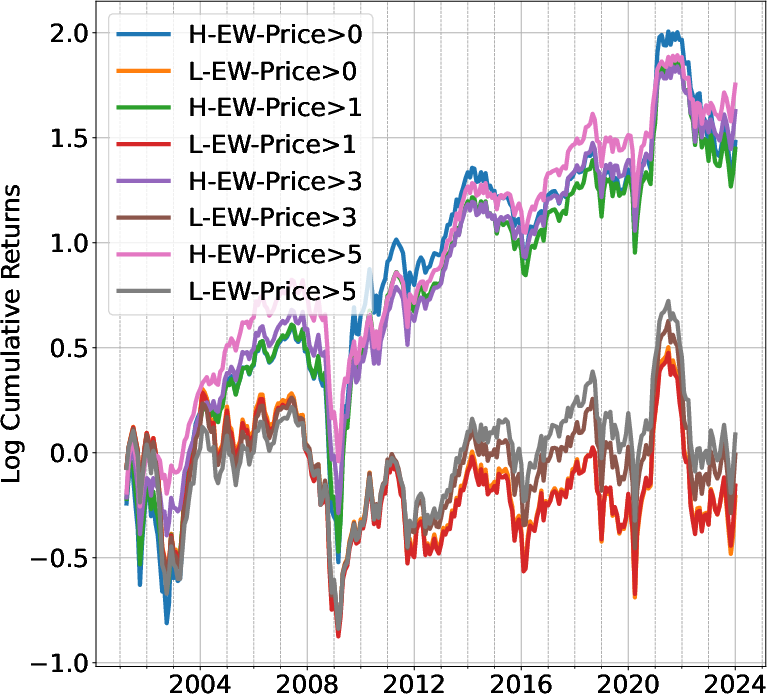

Abstract: This paper introduces StockGPT, an autoregressive ``number'' model trained and tested on 70 million daily U.S.\ stock returns over nearly 100 years. Treating each return series as a sequence of tokens, StockGPT automatically learns the hidden patterns predictive of future returns via its attention mechanism. On a held-out test sample from 2001 to 2023, daily and monthly rebalanced long-short portfolios formed from StockGPT predictions yield strong performance. The StockGPT-based portfolios span momentum and long-/short-term reversals, eliminating the need for manually crafted price-based strategies, and yield highly significant alphas against leading stock market factors, suggesting a novel AI pricing effect. This highlights the immense promise of generative AI in surpassing human in making complex financial investment decisions.

- “Chronos: Learning the Language of Time Series” In arXiv preprint arXiv:2403.07815, 2024

- “The social impact of generative ai: An analysis on ChatGPT” In Proceedings of the 2023 ACM Conference on Information Technology for Social Good, 2023, pp. 363–373

- “Language models are few-shot learners” In Advances in neural information processing systems 33, 2020, pp. 1877–1901

- Werner FM De Bondt and Richard Thaler “Does the stock market overreact?” In Journal of Finance 40.3 Wiley Online Library, 1985, pp. 793–805

- “BERT: Pre-training of deep bidirectional transformers for language understanding” In arXiv preprint arXiv:1810.04805, 2018

- Eugene F Fama “Efficient capital markets” In Journal of finance 25.2, 1970, pp. 383–417

- Eugene F Fama and Kenneth R French “A five-factor asset pricing model” In Journal of financial economics 116.1 Elsevier, 2015, pp. 1–22

- Eugene F Fama and James D MacBeth “Risk, return, and equilibrium: Empirical tests” In Journal of political economy 81.3 The University of Chicago Press, 1973, pp. 607–636

- Shihao Gu, Bryan Kelly and Dacheng Xiu “Empirical asset pricing via machine learning” In The Review of Financial Studies 33.5 Oxford University Press, 2020, pp. 2223–2273

- Yufeng Han, Ke Yang and Guofu Zhou “A new anomaly: The cross-sectional profitability of technical analysis” In Journal of Financial and Quantitative Analysis 48.5 Cambridge University Press, 2013, pp. 1433–1461

- “An augmented q-factor model with expected growth” In Review of Finance 25.1 Oxford University Press, 2021, pp. 1–41

- Narasimhan Jegadeesh “Evidence of predictable behavior of security returns” In Journal of Finance 45.3 Wiley Online Library, 1990, pp. 881–898

- “Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency” In Journal of Finance 48.1, 1993, pp. 65–91

- Jingwen Jiang, Bryan Kelly and Dacheng Xiu “(Re-) Imag (in) ing Price Trends” In The Journal of Finance 78.6 Wiley Online Library, 2023, pp. 3193–3249

- Jingwen Jiang, Bryan T Kelly and Dacheng Xiu “Expected returns and large language models” In Available at SSRN, 2022

- “Financial machine learning” In Foundations and Trends® in Finance 13.3-4 Now Publishers, Inc., 2023, pp. 205–363

- “Sentiment Trading with Large Language Models” In Finance Research Letters, 2024

- “Can ChatGPT forecast stock price movements? Return predictability and large language models” In arXiv preprint arXiv:2304.07619, 2023

- “Artificial intelligence in developing countries: The impact of generative artificial intelligence (AI) technologies for development” In Information Development SAGE Publications Sage UK: London, England, 2023

- Whitney K Newey and Kenneth D West “Hypothesis testing with efficient method of moments estimation” In International Economic Review JSTOR, 1987, pp. 777–787

- Henrik Skaug Sætra “Generative AI: Here to stay, but for good?” In Technology in Society 75 Elsevier, 2023, pp. 102372

- “Attention is all you need” In Advances in neural information processing systems 30, 2017

- “ClinicalGPT: large language models finetuned with diverse medical data and comprehensive evaluation” In arXiv preprint arXiv:2306.09968, 2023

- “BloombergGPT: A large language model for finance” In arXiv preprint arXiv:2303.17564, 2023

- Yi Yang, Mark Christopher Siy UY and Allen Huang “FinBERT: A Pretrained Language Model for Financial Communications”, 2020 arXiv:2006.08097

- “OPT: Open pre-trained transformer language models” In arXiv preprint arXiv:2205.01068, 2022

Paper Prompts

Sign up for free to create and run prompts on this paper using GPT-5.

Top Community Prompts

Collections

Sign up for free to add this paper to one or more collections.